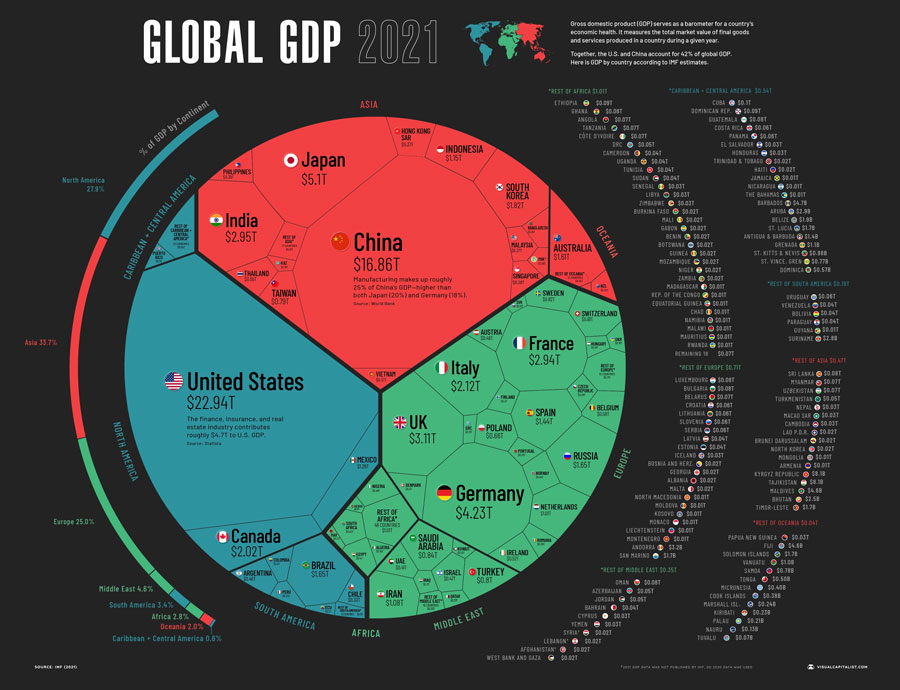

To visualise the distribution of the Global GDP (Gross Domestic Product), this graph by Visual Capitalist helps us greatly. As we can see, only US and China together account for 42% of the Global GDP. This data point tells us about the unequal distribution of countries’ richness worldwide.

It also points out the most powerful global economic players in the world. Looking at the American continent alone, we discover great differences. North America, for example, accounts for 27,9% of global GDP, while South America accounts just for 3.4%, and the Caribbean and Central America for only 0.6%.

Image Source: Visual Capitalist

Image Source: Visual Capitalist

The term Digital Economy was coined in the mid-90s by the Canadian finance expert Don Tapscott in a book of the same name, as the internet began to transform how businesses and consumers interact. This term refers to the impact on the global economy of all digital activities, from e-commerce to digital banking or online education.

The World Bank estimates that the digital economy contributes 15% ($14.5 trillion) to the global GDP in 2021 and is predicted to keep growing, reaching 20,8 trillion in 2025. This percentage shows the importance of this industry on a global scale in a 100 trillion global GDP market.

In general, the global economy post-covid era has benefited greatly from the Digital Economy, as it helped the economy grow and boosted digital life. This study on the Impact of the Digital Economy on Economic Growth shows how countries along the “Belt and Road” have generally benefited from the digital economy:

“there exists an obvious regional imbalance […] Specifically, East Asia, Southeast Asia (especially for Singapore), and Central and Eastern Europe have relatively high levels of digital economy, while most countries in West Asia (except for Israel), Central Asia, and South Asia are still lagging behind. (2) The digital economy has a significantly positive effect on the economic growth in countries along the “Belt and Road.” It can stimulate economic growth by promoting industrial structure upgrading, the total employment and restructuring of employment. (3) COVID-19 has generally boosted the demand for digital industries in countries along the “Belt and Road,” and its impact on digital industries from the demand side is much larger than that from the supply side. Specifically, the digital industries in Armenia, Israel, Latvia and Estonia have shown great growth potential during the epidemic. However, COVID-19 has also brought negative impacts to the digital industries in Ukraine, Egypt, Turkey and the Philippines”.

The digital economy needs good internet infrastructure to work, but isolated digital marks are not enough to decide if a country is more developed digitally than others. That’s why the Dutch VPN company Surfshark created the Index of Digital Quality of Life (DQL). After analysing 117 countries discovered that 7 of the top 10 countries are in Europe. The other three are Israel, the first one; Japan, the 8th; and South Korea, the 10th.

This index looks at 5 indicators to determine the rankings of the countries:

- Internet affordability.

- Internet quality.

- Electronic infrastructure.

- Electronic security.

- Electronic government.

Image Source: Surfshark

Image Source: Surfshark

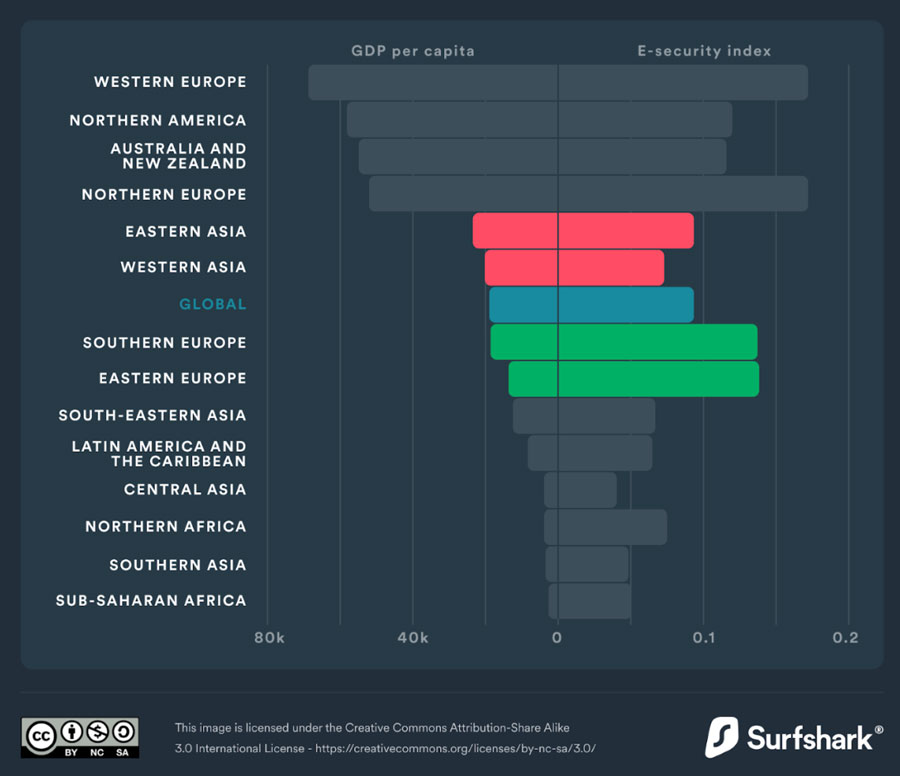

The size of a country’s GDP doesn’t always equate to a high level of Digital Quality of Life. This is evident in the graph below, which illustrates significant disparities between the GDP of various regions and their digital security.

Image Source: Surfshark

Image Source: Surfshark

The Digital Economy was growing at 6,8% rate every year before the Covid-19 pandemic, much faster than the 1.7% growth of the overall economy. It’s believed that Covid-19 has accelerated digital transformation by almost four years.

For the Trade and Development Board of the United Nations, this pandemic has raised, as never before, the question of sustainability and equal access to the digital economy:

“Moving forward, digitalization can be an important element in supporting economic recovery and contributing to long-term inclusive and sustainable development […] the decades prior to the pandemic were characterized by increasingly unsustainable trends”.

The pandemic is seen as an opportunity that has highlighted the weak spots of the digital economy and will help us build a better digital life in the future:

“Recovery from the pandemic can help reshape the global economy in order to accelerate achievement of the Sustainable Development Goals. The pandemic has posed an enormous challenge to development aspirations. It is a stark reminder of shared vulnerabilities and demonstrates the need for real change. Nonetheless, it can also be an inflexion point to alter course and build more resilience into the future”.

It’s not a surprise that most companies that saw significant growth during the pandemic and in the post-covid era are directly related to the Digital Economy, such as Apple, Microsoft, Alphabet, Tesla, Amazon or Nvidia. Other sectors like consultancies, pharma, diagnostics and retailers have also benefited, while oil and gas companies were among the worst affected by it.

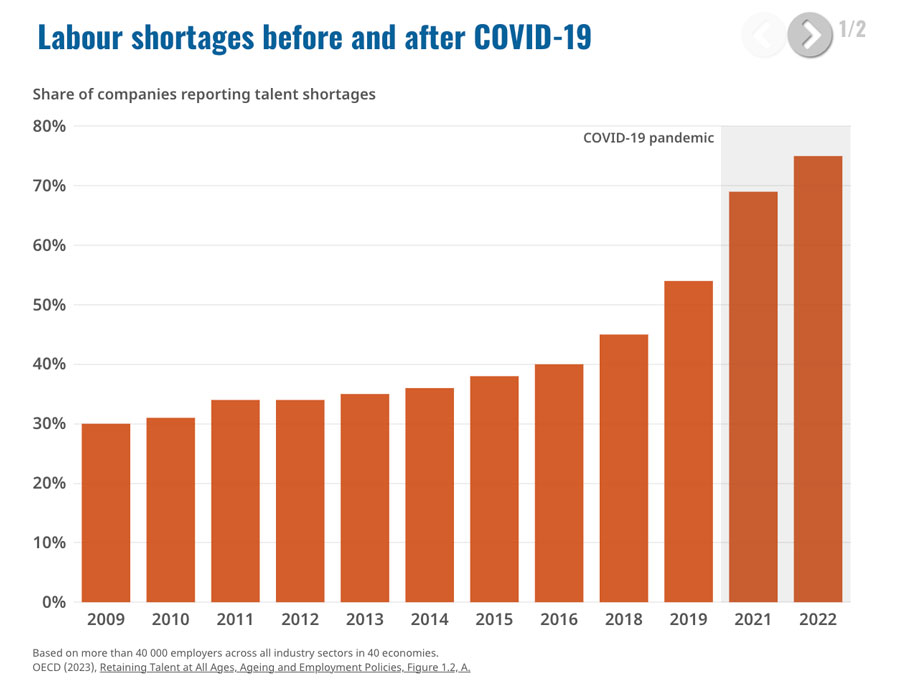

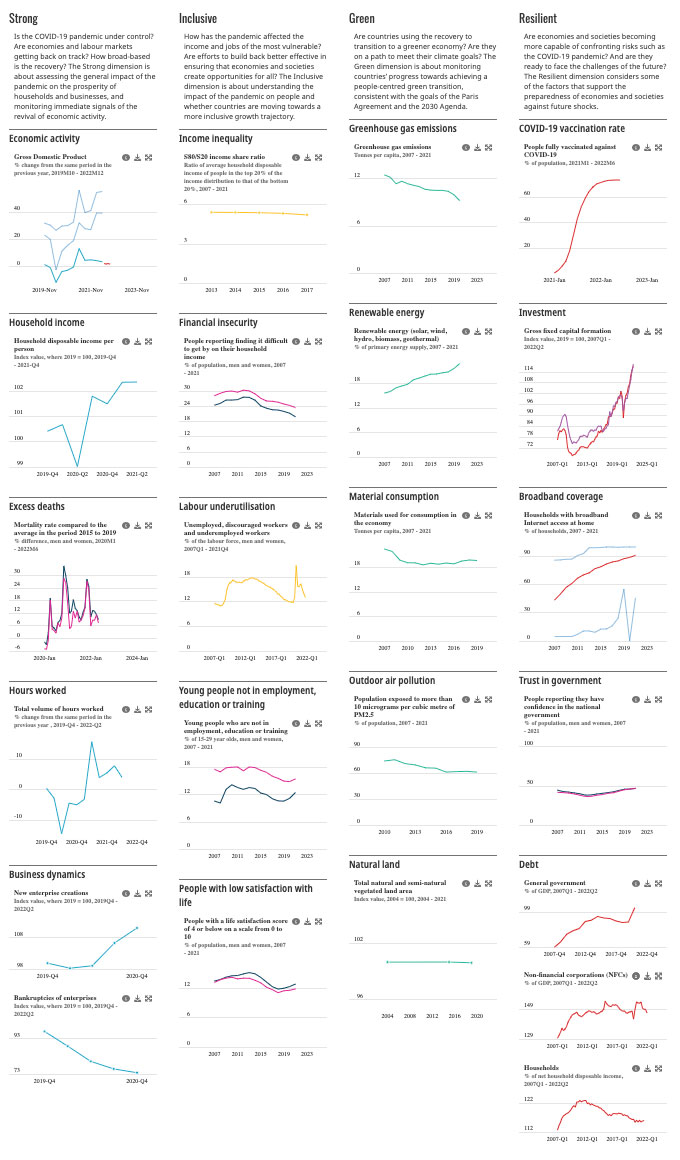

The OECD (Organisation for Economic Co-operation and Development) points out how Covid-19 is an opportunity to make a “greener, more inclusive and more resilient tomorrow”. The digital and green transformations are bringing about rapid changes in the world of work, which significantly impacts workers and employers alike. On the one hand, new technologies are creating opportunities for greater efficiency, productivity, and innovation. But on the other hand, they are leading to job displacement and insecurity for many workers.

This graph illustrates how labour shortages have increased after Covid-19:

Image source: OECD

Image source: OECD

The OECD has started the “Covid-19 Recovery Dashboard” to help revive the economy after the impact of the pandemic:

“As countries begin to emerge from the most acute phase of the COVID-19 pandemic, policymakers and citizens need tools to monitor efforts to revive economic activity and fulfil the shared commitment of OECD Member countries to build back better. This means addressing structural inequalities, accelerating the green transition, and strengthening resilience in the face of future challenges. A quality recovery would help set the world on course for mid- and long-term agendas and facilitate progress towards the SDGs”.

They offer 20 indicators to help address and monitor the progress of recovery:

Image Source: OECD

Image Source: OECD

The economy is experiencing several factors that are slowing it down, including tightening financial conditions due to higher-than-expected inflation, especially in major European economies and the United States.

According to IMF, The global economy is expected to slow down in 2023 due to the fight against inflation and Russia’s war in Ukraine, which has also contributed significantly to damage and slowed down the economy worldwide but is expected to rebound next year. However, this outlook is less negative than predicted by the OECD in the previous forecasts and could mark a turning point for growth and declining inflation.

Despite these challenges, there were some positive developments, such as better-than-expected adaptation to the energy crisis in Europe, strong labour markets, robust household consumption and business investment, and the reopening of China. In addition, global financial conditions have also improved due to the decreasing inflation pressures.

As a result, the growth forecasts for 2022 and 2023 have been slightly increased, with global growth expected to slow to 2.9 per cent in 2023 before rebounding to 3.1 per cent in 2024. The tension between US and China increased, and their relationship deteriorated due to their “trade war”, though trade between them hit new records in 2022.

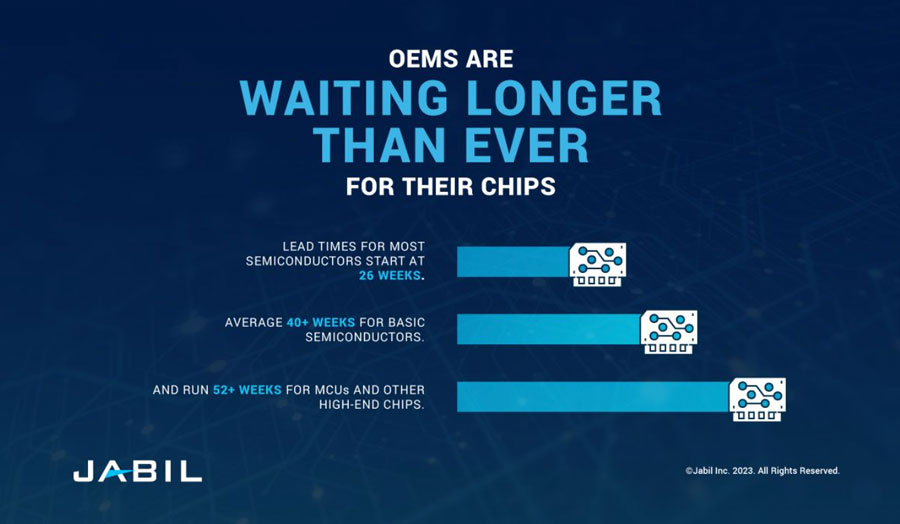

The chip shortage has impacted large consumer electronic products such as smartphones, computers, graphic cards, game consoles and car production. This shortage has been caused by several factors, including high demand for electronic devices since Covid-19, lockdowns and restrictions in the Asian companies in charge of production, transport slowdowns and 5G overlapping technologies.

This slowed down the delivery of consumer products and increased consumer price. TSMC, the largest semiconductors supplier in the world, with 28% of production capacity, has been increasing chip prices between 10% and 20% in the past two years and will raise them by 3% – 6% in 2023. The forecast is that the chip shortage will end in 2024.

The car industry, one of the most impacted by this chip shortage, has increased, on average, the price of a new car by 16% in two years (2020-2022). This is because the average car needs around 100 chips on board, and “many vehicles require thousands of semiconductors to control safety features, electrical and powertrain systems, infotainment, connectivity, and more”.

Image Source: Jabil

Image Source: Jabil

Europe and the US have signed the “Chips Act” to help the semiconductors industry be more resilient in future supply chain disruptions.

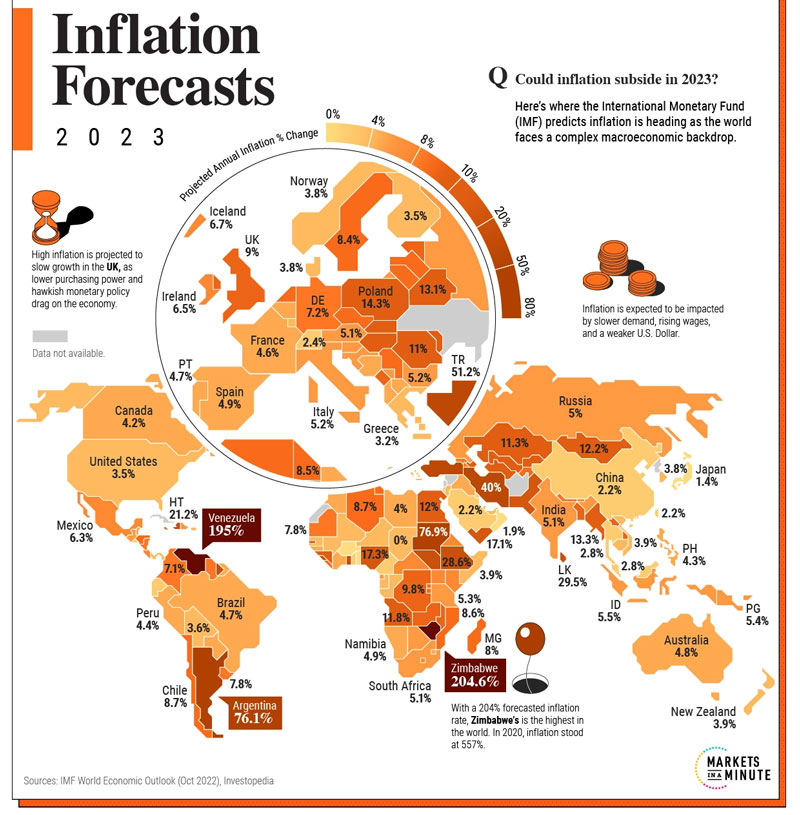

2022 has been a year of continuous global inflation, and it is forecasted that in 2023 it will continue but slow down some points. According to the IMF, global inflation is projected to have reached its highest point in late 2022 but is expected to remain elevated in several regions throughout 2023. However, IMF predicts that the worldwide inflation rate will decrease to 6.6% in 2023 and 4.3% in 2024, following an 8.8% rate in 2022.

Image Source: Advisor – Visual Capitalist

Image Source: Advisor – Visual Capitalist

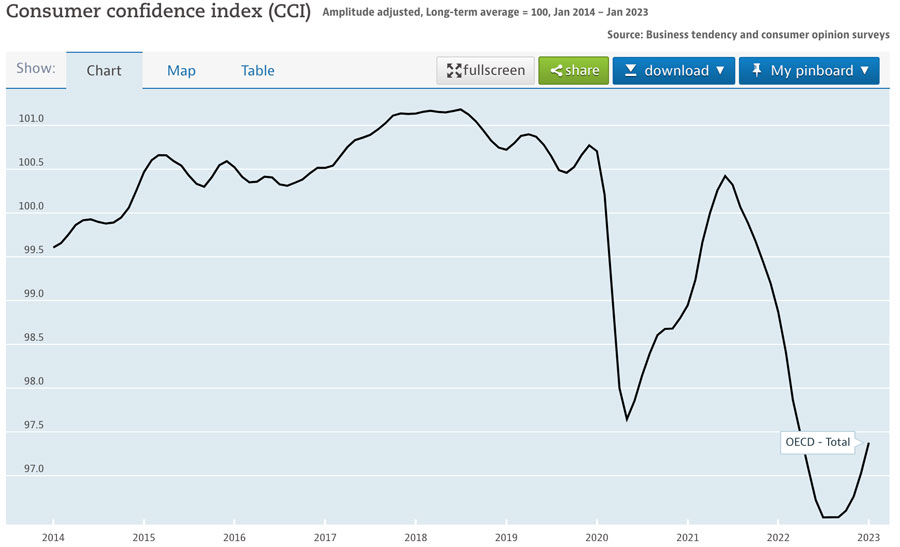

Inflation is the increase in the general price level of goods and services over time. As the prices of goods and services increase, the purchasing power of a given amount of money decreases. This means that people can buy fewer goods and services for the same amount of money.

Inflation can be particularly harmful to people who have fixed incomes or fixed interest rates. It can also negatively impact low-income households, as they may struggle to afford essential goods and services when prices rise. Overall, inflation can lead to a reduction in the standard of living for many people, as it can erode their current income and make it more challenging to afford the goods and services they need. This has a direct effect on consumer confidence. Consumer confidence refers to the level of optimism or pessimism that consumers feel about their current and future financial situation, as well as the overall state of the economy. The consumer confidence index measures how confident people feel about spending their money on goods and services.

High consumer confidence usually indicates that people feel optimistic about their financial situation and are more likely to spend money on discretionary goods and services, such as travel and entertainment. Conversely, low levels of consumer confidence can signal that people feel uncertain or pessimistic about the economy and are more likely to save their money or spend it on essential goods only.

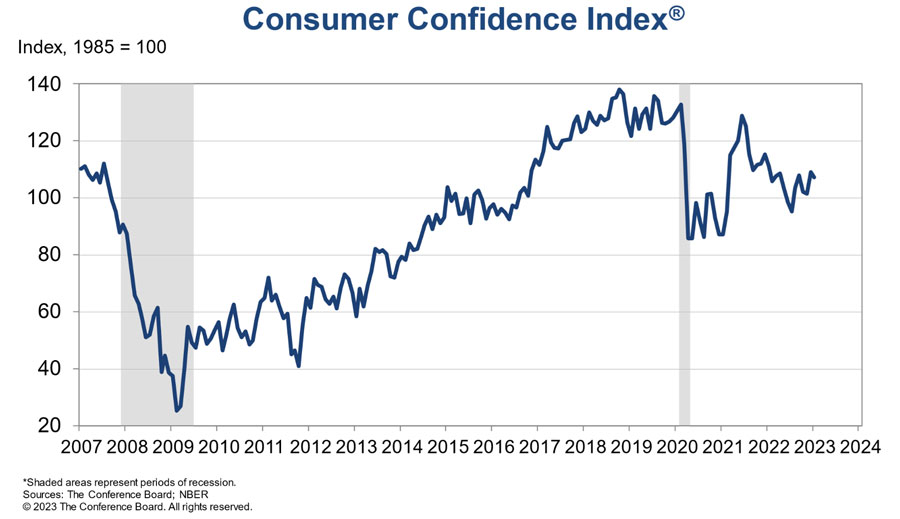

The following graph shows how the confidence levels have dropped significantly from mid-2021 to 2022. Any level below 100 means lower confidence, and above 100 means higher confidence.

Image Source: OECD

Image Source: OECD

To put it into perspective, in this US Consumer Confidence Index, we can see how levels have dropped, but compared to the 2007 financial crisis, the drop is much smaller. However, the significant fall started with covid-inforced global lockdowns and was the biggest one of the decade; now are experiencing the effects of the post-covid era and a more complex world due to the war in Ukraine.

Image Source: The Conference Board

Image Source: The Conference Board

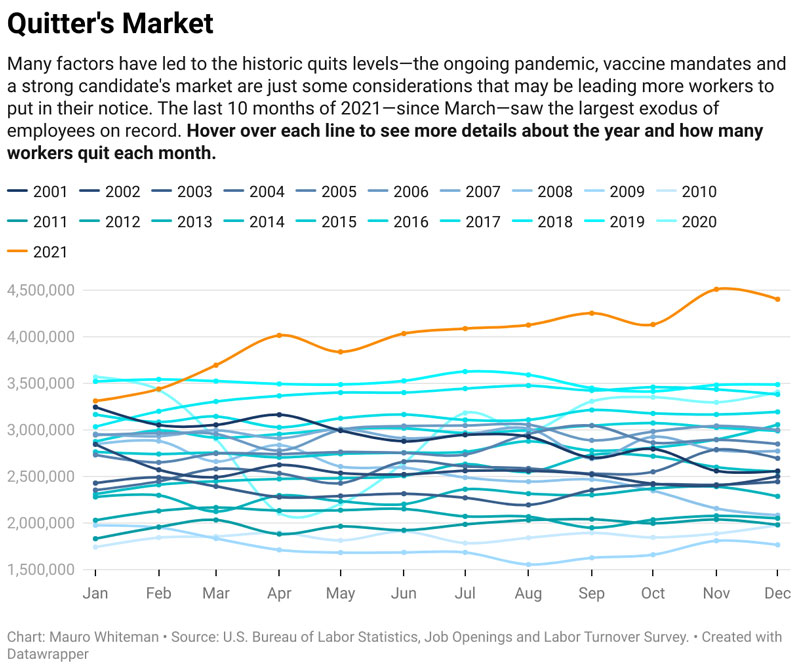

The Covid-19 pandemic has had a significant impact on the workplace, with one of the most notable social effects being the Great Resignation, a term coined by Anthony Klotz in May 2021. This movement, which originated in the US and had a particularly significant impact there, has now spread to many parts of the world.

According to Klotz, the Great Resignation movement emerged during the Covid-19 pandemic as individuals placed more emphasis on work-life balance, job satisfaction, and remote work. In the US alone, approximately 47 million people resigned from their jobs voluntarily in 2021, and another 46.6 million followed in 2022.

Employees found it easier to resign from their jobs if they were not receiving a decent wage, suffering from burnout, or feeling excessive pressure. The pandemic provided people with a great opportunity to upskill or reskill, as they had more time to reflect on their professional goals and desired job positions.

As workers became more discerning, companies felt compelled to re-evaluate their job offers and improve the quality of their positions. People resigned from their jobs to find better work, start their own businesses, or acquire new skills. Employers in low-wage sectors are struggling to fill their open positions.

The following graph illustrates the significant increase in the number of quitters in 2021 compared to previous years.

Image Source: SHRM

Image Source: SHRM

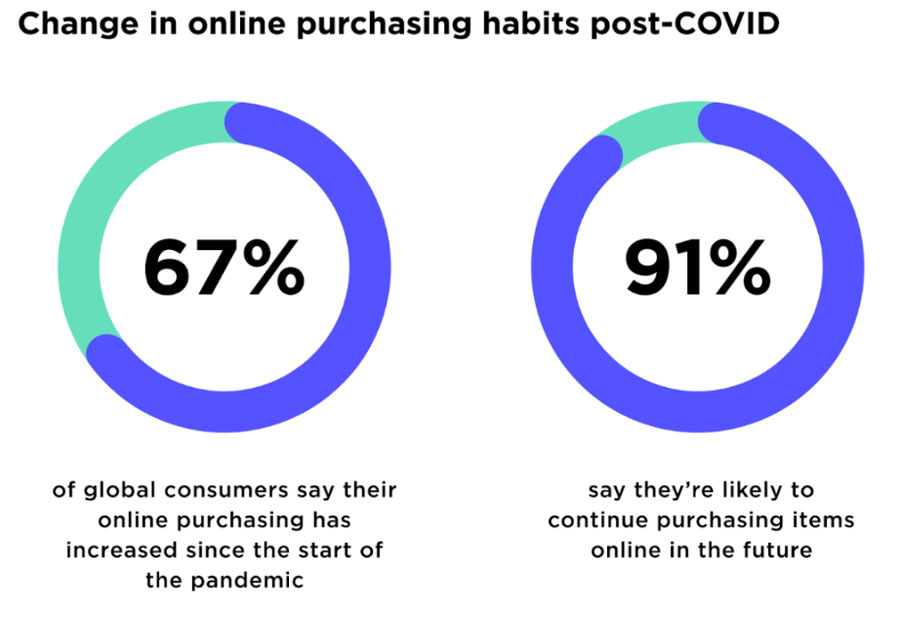

Although the growth of e-commerce was already on an upward trajectory before the COVID-19 pandemic started, 2020 witnessed the largest annual increase in online sales to date. According to the Stackla post-pandemic survey, 67% of participants reported an increase in online purchasing since the pandemic began, with 27% citing a significant increase.

Younger consumers, in particular, demonstrated a marked preference for online shopping. Now, with the Covid-19 pandemic no longer representing a novelty, we can safely say online shopping is not a trend anymore, and it’s here to stay.

Image Source: Nosto

Image Source: Nosto

Online shopping was already popular before the covid-19 pandemic accelerated our need to buy goods online. Safety issues, social distancing and a shift in how consumers perceived their own personal shopping experiences increased online shopping dramatically.

However, the interesting part of this trend is how much has seeped into our shopping reality, and e-commerce continues to be the go-to shopping strategy for millions of people worldwide. In a report by Netelixir in 2021, surveyed participants were asked to select their preference between online shopping or in-store shopping, and 54% indicated they preferred to shop online.

In this ChannelAdvisor 2022 report on Consumer Behaviour, data suggests that consumers spend the same or more online than they were a year ago, and inflation and rising costs aren’t influencing their shopping habits. According to the ChannelAdvisor survey, 23% of consumers spend less money online than they were 12 months ago, 31% spend more than 12 months ago, and 46% spend roughly the same amount.

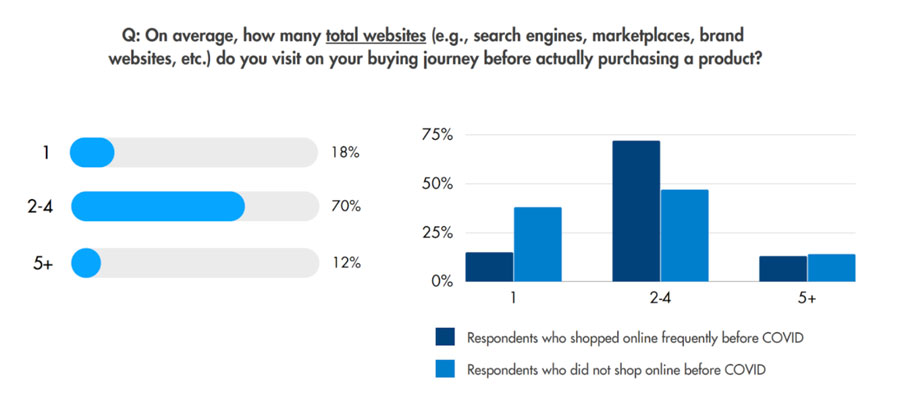

Another critical insight from this study is that consumers’ digital journey is becoming more complex and multifaceted, and they are interacting with numerous touchpoints throughout the browsing and buying process. This trend is particularly evident among younger consumers, who exhibit greater agility in digital spaces and are more likely to engage with multiple channels before making a purchase:

Image Source: Channel Advisor

Image Source: Channel Advisor

Whether this is a positive or negative thing depends on how businesses and consumers adapt to this evolving landscape. On the one hand, the use of multiple touchpoints and channels can offer consumers more options and convenience, enabling them to find what they want and make purchases more easily.

On the other hand, the complexity of this journey can create challenges for businesses seeking to understand and engage with their customers effectively across multiple channels. Ultimately, the impact of this trend on the overall buying experience will depend on how well businesses are able to navigate and optimise the complex digital landscape.

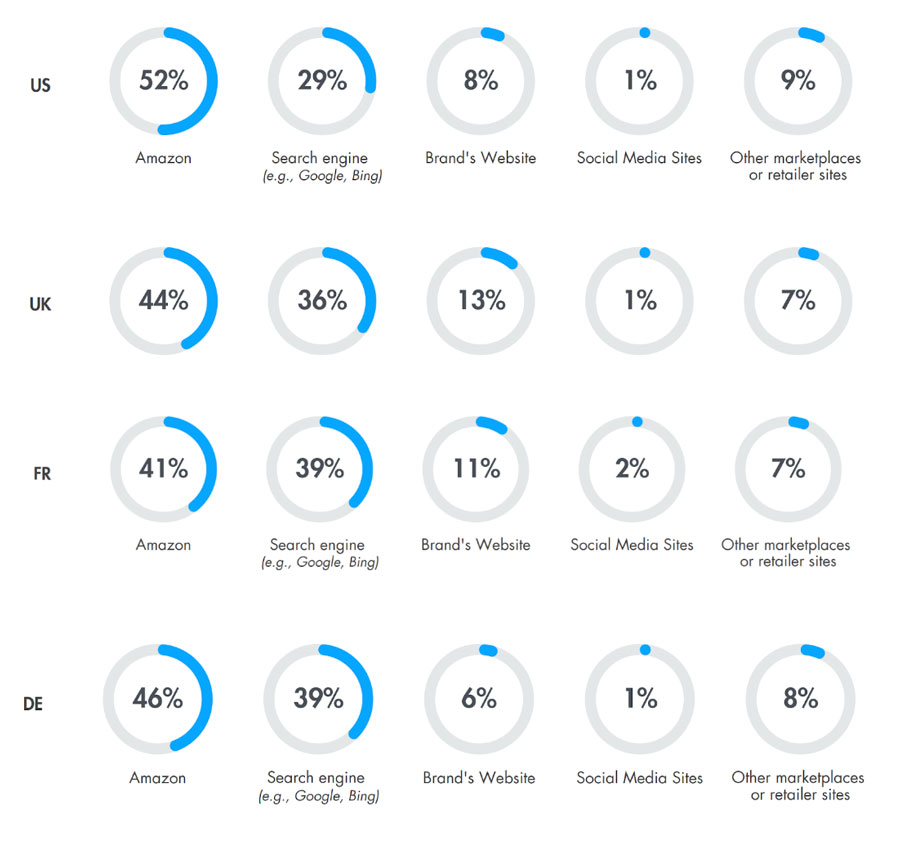

According to the data by ChannelAdvisor, the touchpoints that are most relevant to the shopping journey vary across countries. The following image shows data from the most relevant countries:

The Covid-19 pandemic has not only led to a surge in online shopping but has also resulted in an increase in other online activities, such as online gaming and consuming media content. According to a report by Stackla, 72% of respondents have reported an increase in their social media usage since the onset of the global pandemic. For Gen Z specifically, this percentage is even higher, with 79% of respondents reporting an increase in social media time and 46% stating that the increase was significant.

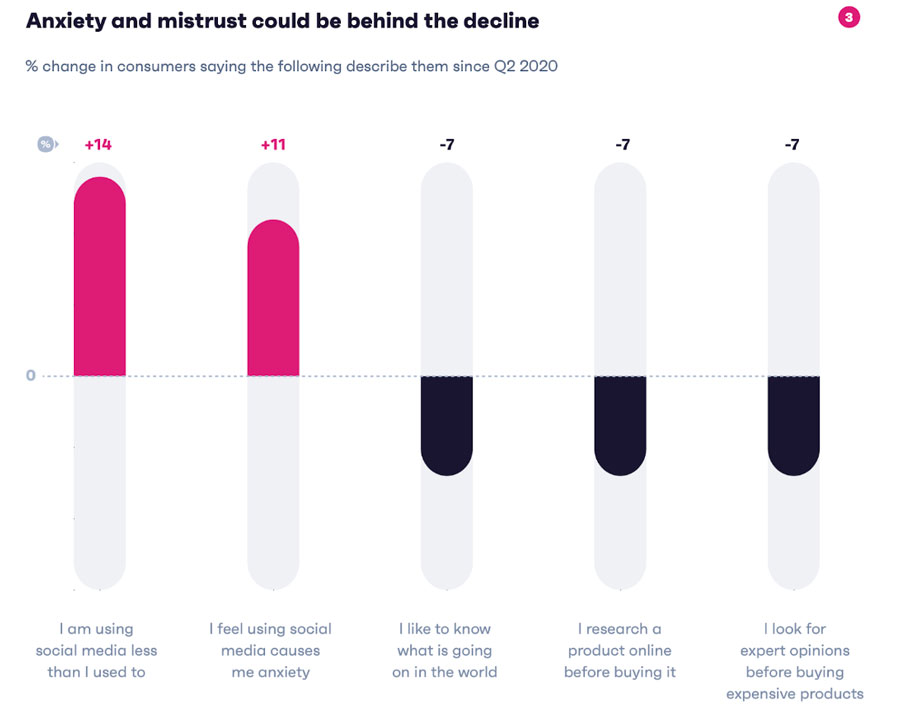

Even if online shopping and social media use are still growing trends, not all our internet habits are continuously on the rise. According to GWI, the daily average time people spend online has almost returned to pre-pandemic levels, even in internet growth markets. The decrease in online time is noticeable in regions like the Middle East & Africa and Latin America.

The reduction is attributed to a lack of free time, and fewer people use the internet daily than during lockdowns. This suggests that traditional online activities have plateaued while foundational internet behaviours are changing. With concerns about the prevalence of misinformation online and its potential impact, people are becoming more mindful of their online activity. In addition, social media has been linked to increased anxiety and stress, which may lead some to limit their time spent scrolling through feeds.

Image Source: GWI

As our online experiences evolve and become increasingly entangled with our in-person needs and expectations, phygital solutions are becoming the go-to trend for brands to provide experiences that merge physical and digital realities.

This includes initiatives such as buy online, pick up in-store (BOPIS), curbside pickup, virtual try-ons, and augmented reality shopping. By integrating these experiences, retailers are able to provide a seamless and personalised shopping journey for consumers, ultimately enhancing their overall experience and increasing customer loyalty.

Phygital solutions aren’t just a fad, they represent the new dawn of our shopping and social daily experiences, and it becomes harder to differentiate between online and offline needs. As Leta Capital claims in their 2021 State of Phygital report, “The digital economy will start cannibalising itself unless it expands offline”.

The digital economy, which refers to the economic activity that results from billions of everyday online connections among businesses, people, devices, data, and processes, may become unsustainable and self-destructive if it relies solely on online interactions.

To avoid this, it’s necessary to expand the digital economy offline by adopting phygital solutions that bridge the gap between the physical and digital worlds, creating a seamless and integrated experience for consumers and businesses. This approach can help to enhance customer engagement, create new business models, and improve customer experiences by combining the convenience and accessibility of digital technologies with the sensory and emotional aspects of the physical world.

The 2021 State of Phygital report identifies a shift from the Information Revolution to the Phygital Revolution, which combines macroeconomic and technological factors into a new world order. Despite the rapid progress of Information Technology, it cannot rescue the offline economy, leading to a possible cannibalisation of the digital economy.

The authors suggest that technologies like Augmented & Mixed Reality, IoT, and 5G will unite under the Phygital umbrella and cause a global redistribution of wealth and assets, leading to a dramatic disruption of the offline world and opening the gateway to the offline economy for digital enterprises.

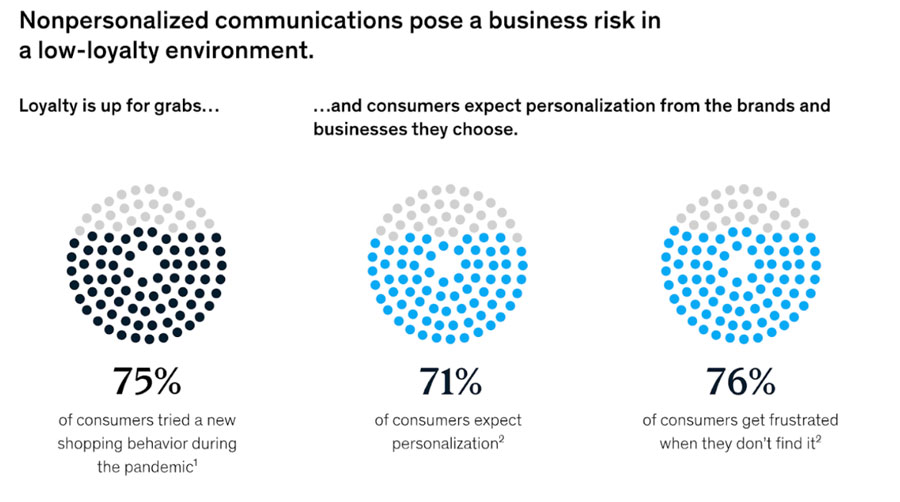

Brand loyalty has decreased in recent years, with consumers now having access to more options and information than ever before. This has led to a surge in personalisation strategies as brands seek to engage customers and build stronger relationships with them.

Personalisation can take many forms, from customised product recommendations to targeted marketing messages, but the goal is always the same: to create a more tailored and relevant experience that resonates with consumers and keeps them coming back for more. By leveraging the power of personalisation, brands can establish deeper connections with their customers and differentiate themselves from the competition in an increasingly crowded marketplace.

Consumers’ digital behaviour across all industries is greatly influenced by their desire for personalised and niche content. This trend is significantly impacting traditional media and entertainment consumption habits. According to McKinsey’s data, consumers now view personalisation as the default standard for engagement:

Image Source: McKinsey

Image Source: McKinsey

This is consistent with Stackla’s data, which claims that 31% of users leave an e-commerce site without making a purchase because the experience wasn’t personalised enough. In Stackla’s survey, 88% of participants say authenticity is important when deciding which brands they like and support, and 50% claim authenticity is very important to them.

Image Source: Nosto

Image Source: Nosto

The report suggests that users consider User Generated Content (UGC) the most authentic content. In the view of consumers, user-generated content holds 8.7 times more impact than influencer content and 6.6 times more influence than branded content. In addition, a significant 79% of people have reported that user-generated content has a substantial impact on their purchasing decisions.

According to McKinsey, 76% of consumers consider receiving personalised communications important when considering a brand, and 78% of consumers are more likely to repurchase from a brand that provides personalised content. Personalisation is a powerful tool for building long-term customer loyalty, as it generates data from recurring interactions, allowing brands to design even more tailored experiences. This leads to a flywheel effect that results in increased customer lifetime value and loyalty.

Despite the importance of customisation for users, companies are struggling to adapt to this trend. According to Twilio’s State of Personalisation 2022 report, less than half of companies personalise communications based on real-time customer behaviour.

And data from Cheetah Digital suggests that brand personalisation efforts and user privacy concerns are deeply linked: about half of the consumers (49%) are frustrated by irrelevant content or offers, 41% receive messages that don’t reflect their wants and needs, and 31% feel that a brand has not recognised their shopping or loyalty history.

Additionally, 35% of consumers feel frustrated when receiving messaging based on information that hasn’t been shared directly with the brand. Relationship marketing depends on personalisation, meaning that brands must deliver value, relevancy, and meaningful experiences based on individual preferences and data, not on third-party or inferred data that may have been collected by tracking or other means.

Undoubtedly, digitalisation has become an essential component of all industries worldwide. According to research by the Manpower Group, the IT industry’s organisations show the most optimistic hiring plans, with a 35% profit. By the middle of this decade, an estimated 85 million jobs may disappear by a shift in the division of labour between humans and machines, while another 97 million new ones will take place to adapt to the division of labour between humans, machines and algorithms. Automatization is a growing trend that the tech workforce must face. It’s paramount that workers keep up with the latest advances to take advantage of them. AI and machine learning don’t have to be seen as a threat but as an opportunity to increase productivity.

Moreover, based on the World Economic Forum predictions, 1.1 billion jobs will be radically transformed by technology in the next decade, which accelerates the need for highly skilled and cutting-edge workers.

The 2021 Industry Skills report by the online learning platform Coursera reveals that the pandemic has hastened the rate of global digitisation. In the same line, Microsoft’s CEO Staya Nadella said in 2020 that:

“we’ve seen two years’ worth of digital transformation in two months. From remote work teamwork and learning to sales and customer service, to critical cloud infrastructure and security”.

However, since the progress made during the pandemic is unlikely to be undone, there is a risk that digital skills gaps across numerous sectors may worsen.

Coursera’s report emphasises the need to upskill current workforces, with crucial skills being cloud computing, cybersecurity, data analysis, and software development. Additionally, Microsoft forecasts that by 2025, there will be 149 million new digital jobs in domains like cybersecurity, data analysis, privacy and trust, machine learning and AI, cloud and data roles, and software development.

As more businesses adopt new technologies, there is a growing need for professionals with expertise in these areas, and the shortage of workers with these skills has led to a global skills gap, where businesses cannot find the right talent to meet their needs. The costs of retaining talent have led to intense competition and higher salaries, making it a lucrative field for job seekers.

The increasing adoption of technology has led to the creation of new opportunities, but it has also introduced challenges, particularly in meeting the demand for tech professionals with the right skills. The Manpower study presents the fact that large companies (with more than 250 employees) struggle the most to recruit and retain talent compared to smaller firms (those with fewer than 10 employees).

The skills that companies look for differ, if it is a small company or a bigger one. Small companies, like early-stage startups, usually seek that the worker knows a little about everything because they normally need to wear different hats. But companies need many workers with specific skills when they get bigger, which leads to specialised hiring requisites that make filling all the demanding positions more difficult.

For many companies, it becomes complicated to hire a worker with the required depth of technical knowledge and business understanding to implement digital tools in a sophisticated manner.

Healthtech is one example of how digitalisation has transformed business operations. A survey by Global Data found that 41% of healthcare industry professionals viewed the lack of specific skills and talents as a significant hindrance to the uptake of emerging technologies in the industry.

In finance, digitalisation has led to the growth of fintech, creating new opportunities and challenges for financial institutions, investors, and customers alike and making financial services more accessible to underserved populations. As a relatively new industry, the lack of awareness, the huge competition from other industries and the requirement of niche skill sets, such as financial, technology and data analytics, are leading to a talent gap in the sector.

Also, the retail industry has been impacted by the integration of digital technology. The rise of e-commerce is expecting a growth rate (CAGR) of 11.35% from 2023-2028, leading to a growing demand for digital marketing, website development, and logistics professionals.

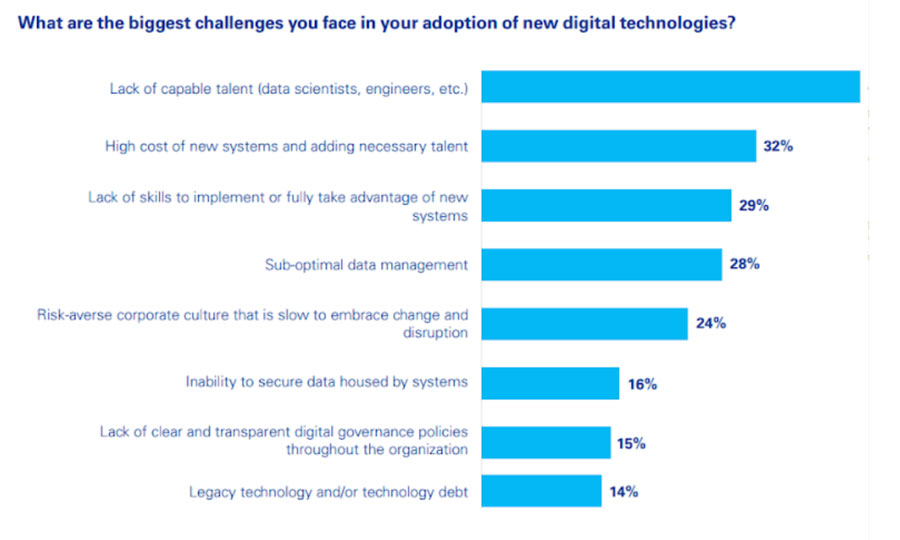

With the growth of Industry 4.0, or the Forth Industrial revolution, which involves the use of automation, the Internet of Things (IoT), and other kinds of “smart” and connected production systems such as cloud computing and analytics, manufacturing has also been highly influenced by digitalisation. This technological equipment allows manufacturers to meet the demands of a rapidly changing global market, but according to KPMG, 48% of manufacturing firms consider the lack of capable talent as the biggest challenge they face.

Based on data from the KPMG Global Tech Report released in September 2022, the biggest challenge businesses face in their adoption of digital technologies is the lack of capable talent, followed by the high cost of purchasing and implementing new systems and sourcing necessary talent.

Image Source: KPMG

Image Source: KPMG

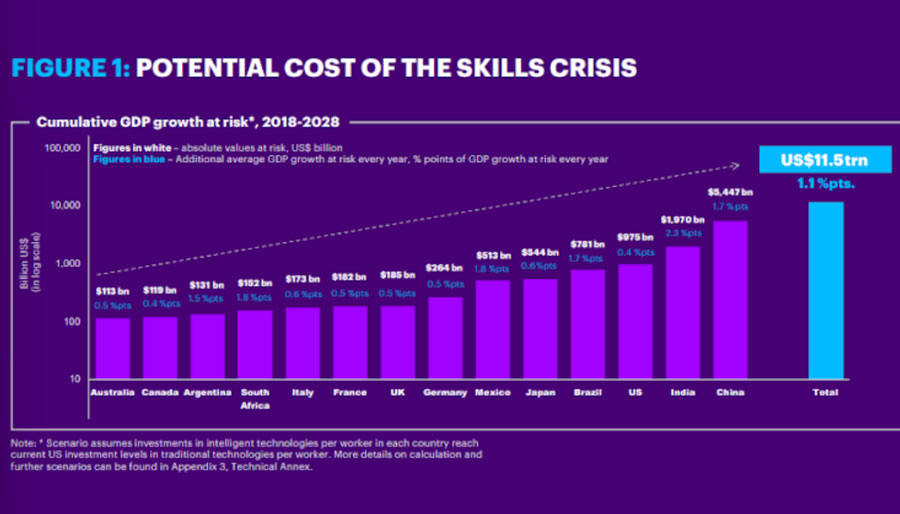

Globally, the lack of digital skills has negative consequences. For instance, if the digital skills gap is not addressed, the G20 countries could miss out on as much as $11.5 trillion of cumulative GDP growth by 2028, according to estimates by Accenture. This equates to a loss of approximately 1.1 percentage points of cumulative GDP growth across the 14 countries measured.

The extent of the risk to growth varies depending on the country’s economy, industry, and distribution of labour across different roles. India faces the highest risk of GDP growth loss due to the digital skills gap, with an average of 2.3 percentage points yearly. South Africa and Mexico follow closely behind, with a risk of 1.8 percentage points of GDP growth annually, while China and Brazil face a risk of 1.7 percentage points of GDP growth annually.

In contrast, Canada and the United States face relatively low risk, with a loss of only 0.4 percentage points of GDP annually. Similarly, Australia, France, the United Kingdom, and Germany also face relatively low risk, with a loss of 0.5 percentage points of GDP annually.

Image Source: Accenture

Image Source: Accenture

Despite the threat of an economic decline in 2023, the demand for talent remains high, especially in growth sectors. The digital transformation forces us to look for creative ways to cover these positions with a medium/high level of qualification.

The influence of digitalisation is expected to continue growing, with new technologies such as artificial intelligence, blockchain, and the Internet of Things transforming businesses’ operations. To meet this demand, businesses must invest in training and development programs to upskill their existing workforce. In this report, upskilling refers to expanding people’s capabilities and employability so they can fully participate in a rapidly changing economy.

According to a global survey led by McKinsey in 2021, skills building has become the most sought-after strategy to close the skills gap, with 69% of organisations doing more skill building now than they did before the COVID-19 pandemic (more than hiring, contracting or redeploying employees).

In times of workplace uncertainty, an average of 66% of employers surveyed for the Future of Work Report by the World Economic Forum expected to get a return on investment in upskilling and reskilling their employees. In fast-growing and dynamic industries, such as the tech industry, it is essential for businesses to ensure that their employees have the skills and knowledge required to stay ahead of the curve.

Investing in training and upskilling allows businesses to keep up with the latest trends and developments in the tech industry. As the industry is constantly evolving, it’s still crucial for companies to ensure that their employees are well-equipped with the latest knowledge and skills. This can help businesses to maintain a competitive edge and stay ahead of their competitors.

Also, it can increase employee productivity and efficiency. When employees have the necessary skills to carry out their jobs, they can work more efficiently and effectively, reducing the time and cost required to complete tasks, improving the work’s quality and increasing overall productivity.

An illustrative study by MIT Sloan School of Management found that a 12-month workforce training program focused on soft skills delivered 250% of ROI within eight months of completion due to the increased productivity associated with applying soft skills to businesses.

Employee satisfaction also increases with training programs because the experience of learning and appropriating new skills empowers employees to perform better. Furthermore, it sparkles personal development and generates self-motivation. According to a survey conducted by Statista, 75% of employees worldwide were satisfied or very satisfied with their company’s reskilling and upskilling programs.

Moreover, according to the Udemy survey, the vast majority of employees see potential opportunities in being pushed to learn new skills, responding that they’re excited to learn new skills and transition to a new career or job function in the future. In the context of Great Resignation, upskilling is converted efficiently to retain talent.

Another strategy to address the skills gap is changing degree-based hiring practices to hiring processes based on skills. Attracting digital talent is a crucial component of any digital skills strategy. However, there are challenges with current hiring practices, particularly with respect to evaluating skills during the hiring process and the mismatch between job descriptions and actual job requirements.

Companies need to understand job markets and requirements better and develop skills-based hiring practices to address these issues. This requires a greater emphasis on skills, in addition to formal education degrees, in a way that employers can easily recognise and respond to. For instance, some companies have started removing degree requirements from job postings to increase the pool of potential hires.

By reversing the so-called “degree inflation”, the Skilled Through Alternative Routes (STARs) have an opportunity to enter the workforce breaking the limits of economic mobility. Machine learning, AI, and automated pre-selection platforms can also potentially help with a skill-based hiring approach by standardising recruitment and creating structured interview settings that evaluate hard and soft skills while removing personal and demographic information.

Such a skill-based hiring approach expands the available talent pool, reduces unconscious bias through objective assessment of relevant skills, and facilitates faster internal movement between departments. Overall, creating skills-based hiring practices provides incentives for workers to invest in their skills, signalling the market value of new credentials, according to this article by McKinsey & Company.

On the other side, governments worldwide must work closely with educational institutions to develop relevant and up-to-date curricula that prepare students for future jobs. The rise of digital technology has revolutionised how we live, work, and learn. The digital age has brought tremendous benefits to society but has created a gap between what students learn in schools and what they need to know to succeed in the modern workforce.

It is essential for the educational system to change to address this digital skills gap and prepare students for the future. One step to address the digital skills gap is to treat digital competencies as transversal competencies taught across all subjects in the curriculum, integrated into other learning areas. This approach teaches students to apply basic digital skills in different contexts, empowering them to pursue tech careers.

It is also important to address the digital divide. Many students do not have access to the technology and resources needed to develop digital skills. The educational system, together with the governments, should work to provide equal access to digital tools and resources, regardless of a student’s background or socioeconomic status.

It has also been highlighted that building digital skills across society has the potential to open up opportunities for those who have been traditionally “left behind”, fostering diversity, equity and inclusion. To bridge the digital divide, it is paramount to improve digital literacy, which involves helping people acquire the skills they need in order to use digital technology effectively.

Here are some strategies to improve digital literacy:

- Provide training and support: teaching people how to use devices, navigate the internet, and use digital tools such as social media, online banking, and e-commerce platforms is essential. This can be done through online courses, in-person training, or community workshops.

- Use simple language. Digital technology can be complex, and people unfamiliar with it may find it overwhelming. Using simple language and avoiding technical jargon can help people understand how to use technology more easily.

- Encourage experimentation. People learn best by doing. Encouraging experimentation and exploration can help people build confidence in their ability to use digital technology. This can involve allowing people to try new apps or platforms and helping them troubleshoot problems as they arise.

- Teach critical thinking. Digital technology can be a powerful tool and a source of misinformation and confusion. Teaching critical thinking skills can help people evaluate the information they find online, spot fake news, and avoid scams and phishing attacks.

- Foster a culture of learning. Digital technology is constantly changing, and people need to be able to adapt to new tools and platforms as they emerge. Fostering a learning culture can help people stay up-to-date with the latest digital trends and technologies.

Improving digital literacy is essential for bridging the digital divide and ensuring that everyone has the opportunity to benefit from the digital age. By providing training and support, using simple language, encouraging experimentation, teaching critical thinking, and fostering a learning culture, we can help people acquire the skills they need to thrive in a digital world.

Image Source: World Economic Forum

Image Source: World Economic Forum

Along this line, the World Economic Forum launched a project in 2020 called the Reskilling Revolution that has reached out to 350 million people since then. This programme aims to prepare the global workforce with the skills needed to confront technological disruption and the green transition challenges and contribute to building a fairer, more inclusive world that will benefit the economy and society through better skills and education for generations to come.

This initiative embraces public and private sectors to advance an entirely different agenda, where people’s futures and global economic prospects are enhanced by mobilising worldwide mass action on reskilling, upskilling and education transformation. The World Economic Forum roadmap for 2023-2024 includes accelerating reskilling and upskilling worldwide and promoting skills-based labour markets.

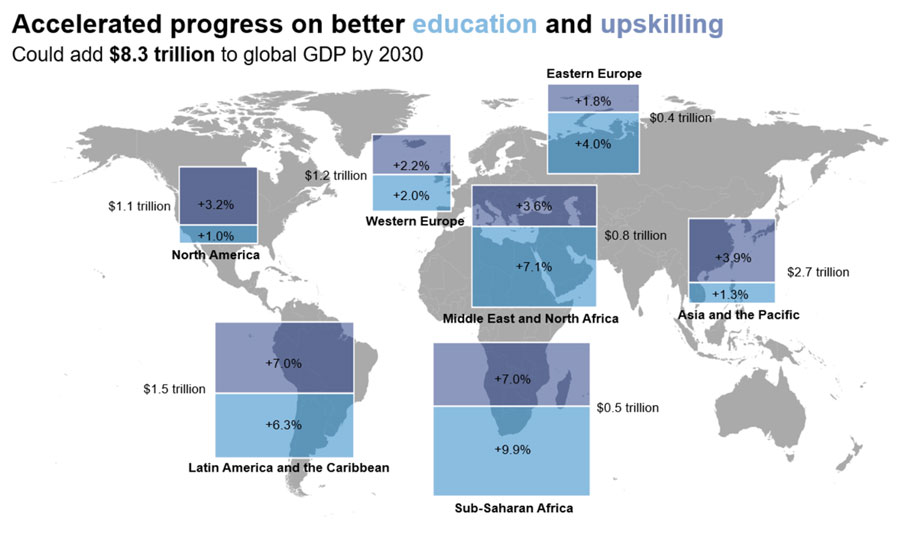

In a new report, Upskilling for Shared Prosperity launched during the Davos Agenda 2021, PwC and the World Economic Forum make a clear case for why leaders across industries should prioritise upskilling of the current workforce.

The report urges governments to take an agile approach to boost national skills upskilling initiatives, working with businesses, non-profit institutions, and the education sector. This includes initiatives to create green economy jobs and support technological innovation. The report estimates that if countries upskill their citizens in line with OECD industry best practices, this will lead to an additional $6.5 trillion in GDP growth, creating 5.3 million net new jobs for the year 2030.

In light of the above, by implementing these strategies, businesses and society as a whole can adapt to the digital age and prepare for the future of work.

Gen Z, also known as the post-millennial generation, is the generation born between the mid-1990s and the mid-2000s. This generation is the first to grow up in a fully digital age, with access to technology and the internet from a young age. As they enter the workforce, they bring with them a unique set of skills and expectations, particularly when it comes to technology.

Gen Z has a natural affinity for technology and is comfortable using a wide range of digital tools and platforms. They are digital natives who have grown up using social media, messaging apps, and other online tools as part of their daily lives, which makes them well-suited for jobs that require technical skills.

Moreover, a study by the Work Force Insitute points out Gen Z for valuing flexibility, work-life balance, and remote work. According to this McKinsey article, as Gen Z entered the workforce in a hybrid-working world brought on by the COVID-19 pandemic, flexibility is a major pull factor for their career development.

They are interested in jobs that allow them to work from anywhere, and they are comfortable using digital tools to communicate and collaborate with colleagues, as it is part of their daily life. As a result, companies that offer remote work opportunities and flexible schedules may be particularly attractive to Gen Z job seekers.

Attracting Gen Z to the tech workforce is important for the industry not only because soon they will surpass Millenials as the most populous generation on earth, also because they will nourish the talent pool with highly skilled and tech-savvy workers. Gen Z is known for its creativity, innovation and desire to impact society positively. By tapping into these qualities, tech companies can bring fresh perspectives and new ideas to drive innovation and help companies stay competitive.

Furthermore, Gen Z has unique insights into what tech consumers want and need as they are the first generation to grow up completely immersed in technology. Their technological experience can lead to new ideas for improving user interfaces, developing better apps and streamlining workflows.

Additionally, Gen Z is the most ethnically and racially diverse generation in history, and their views on gender and identity are unprecedented and untraditional. With their entrance into the tech workforce, they’ll also bring diverse perspectives and experiences that can help companies to develop more inclusive products and services that better meet the needs of a broader range of customers.

Image Source: McKinsey & Company

Image Source: McKinsey & Company

Overall, the entrance of Gen Z into the tech workforce will likely have a significant impact on the industry. With their tech-savvy skills, they are likely to drive innovation and change how technology companies operate. Companies that want to attract and retain Gen Z employees will need to adapt to their unique expectations and preferences, including offering opportunities for upskilling, career development, and work-life balance.

The Digital Transformation 4.0, Industry 4.0 or the Fourth Industrial Revolution are terms used to describe the integration of digital technologies in all areas of society, including business, government, education, and healthcare. The 4.0 digital transformation is a wave that started in the mid-2010s, and it’s a continuation of the earlier stages of digital transformation, which have been driven by the widespread adoption of the internet and mobile technologies. In McKinsey’s words:

“is the next phase in the digitisation of the manufacturing sector, driven by disruptive trends including the rise of data and connectivity, analytics, human-machine interaction, and improvements in robotics”.

The term 4th industrial revolution was coined by Klaus Schwab, a German economist and the founder and executive chairman of the World Economic Forum, an international organisation that brings together world leaders, business executives, and academics to discuss global issues and promote public-private cooperation.

The term 4IR (4 Industrial Revolution) describes the current era of technological advancement, which is characterised by the integration of physical, digital, and biological systems.

As the World Economic Forum head, Schwab has advocated for public-private partnerships to address global challenges and promote sustainable economic growth. He has called on business leaders to adopt a more stakeholder-centric approach to corporate governance, prioritising the needs of customers, employees, and communities alongside those of shareholders.

In his book «The Fourth Industrial Revolution«, Schwab argues that it is essential for governments, businesses, and individuals to work together to ensure that the benefits of this new era are shared equitably and that the potential risks are managed effectively.

These are some of the key points of his book:

- The fourth industrial revolution (4IR) is characterised by the convergence of technologies across physical, digital, and biological domains. These include artificial intelligence, robotics, the internet of things, autonomous vehicles, 3D printing, and biotechnology.

- The 4IR can potentially transform our economy and society, but it also poses significant challenges. It will disrupt many traditional industries while creating new ones. It will also profoundly impact employment, education, and social structures.

- Schwab argues that the success of the 4IR will depend on our ability to manage its impact. This will require new forms of governance, collaboration between different stakeholders, and a focus on human-centred design.

- He also emphasises the importance of ethical considerations in developing and deploying new technologies. This includes ensuring privacy and security, preventing the concentration of power in the hands of a few, and ensuring that technology is used for the greater good.

- Finally, Schwab argues that the 4IR presents an opportunity for a new type of capitalism that is more inclusive and sustainable. He calls for a «stakeholder economy» that recognises the importance of shareholders, employees, customers, and the wider community.

Image Source: Researchgate

Image Source: Researchgate

Boston Consulting Group has coined the term “Bionic Companies” to refer to “organizations that blend digital and human capabilities—and apply them to all aspects of their business”.

To achieve a successful digital transformation of a business, companies can follow six steps recommended by the experts. These steps are crucial in improving the current success rate from 30% to 80%. It is essential to note that these steps are presented as a commercial service to the clients.

Nonetheless, they provide valuable insights into the process of digital transformation of a company.

- Crafting a clear, Integrated Strategy

- Commit to leadership from the Top to the Middle

- Putting the best people in the right places

- Adopting an Agile governance mindset

- Monitoring and Measure your transformation progress

- Creating a business-led tech and Data Platform

As we can see, these steps to transform a company to adopt a digital mindset has a lot to do with managing, collaborating and teaching people how to work together towards these new objectives to create a new organisational culture and less to do with just digitalising the processes and buying software.

Digital transformation is driving significant changes in how businesses operate, creating new business models and disrupting traditional industries. One of the key features of the 4.0 digital transformation is the ability to collect, analyse, and use vast amounts of data to gain insights into customer behaviour, product performance, and operational efficiency. This allows businesses to make data-driven decisions and create more personalised experiences for employees and customers.

The 4.0 digital transformation also drives changes in the workforce, with an increasing focus on technology-related skills, such as data analytics, software development, and cybersecurity. As a result, companies need to invest in employee training and development programs to ensure that their workforce is equipped with the necessary skills to succeed in the digital age.

4IR shapes every aspect of our personal and professional lives and the private and public sectors. From how we work and communicate to the products and services we use. As the pace of technological change accelerates, it will be essential for businesses and employees to stay ahead of the curve and learn, adapt and collaborate in the design of new technologies to remain competitive in the global economy.

We have introduced this prompt to Chat GPT, the text generative AI in beta phase created by Open AI, which has been on every headline since it was released in November 2022, the following:

“Explain to me what is Generative AI”.

And this is its answer:

Generative AI refers to a type of artificial intelligence that can create or generate new content, such as images, music, or text, that is not based on existing data or patterns. It works by using deep learning neural networks that are trained on large datasets to create new data that is similar to the training data.

There are two main approaches to generative AI:

- Generative Adversarial Networks (GANs) – This involves training two neural networks: a generator network that creates new content and a discriminator network that tries to distinguish between the generated content and real content. The generator network is then adjusted based on the feedback from the discriminator network to improve the quality of the generated content.

- Autoencoder Networks – This approach involves training a neural network to compress the input data into a smaller set of features, and then use another neural network to reconstruct the original data from the compressed features. By modifying the compressed features, new data can be generated.

Generative AI has numerous potential applications, including content creation, art, music, and even synthetic voice or video creation. However, as with any AI technology, there are also concerns about the ethical implications and potential misuse of generative AI.

The answer is a bit technical, but it’s a representation of how “smart” this AI is and how capable of making us not distingüish much if we are talking to a machine learning model or to a human being. We have to keep in mind that those are not answers that are already written on the internet, they are original and unique responses created from its vast dataset, and depending on your prompt, it could give you a similar answer in many different ways.

These same text prompting mechanisms are followed to obtain the results we want by AI generating images, AI generating music, AI generating voices, AI generating 3D models like Nvidia’s Magic 3D, Open AI’s Point-E or Google’s Dreamfusion.

Generative AI’s are growing in every sector, and we are just starting to see the potential of this technology. This tech can also create websites using text prompts, create videos, or create AI-generated human models to use online without worrying about copyright. There are also generative AI that can create code and AI powered tools to help UX designers.

Image Source: Imagen Video

Image Source: Imagen Video

The following image shows snapshots of many other videos generated through this Google Imagen Video AI.

Image Source: Imagen Video

Image Source: Imagen Video

In just a few months, generative AI has exploded. Within a week of its release, ChatGPT obtained an average of 13 million daily users, and within two months, it reached over 100 million users, becoming the sole internet application to achieve this milestone in history.

Generative AI has been labelled “The technology of the year”, and it’s expected to keep growing and conquering new fields very soon. There’s been a huge generative AI adoption and development in several companies in order to provide an AI service to their clients. The generative AI race has begun.

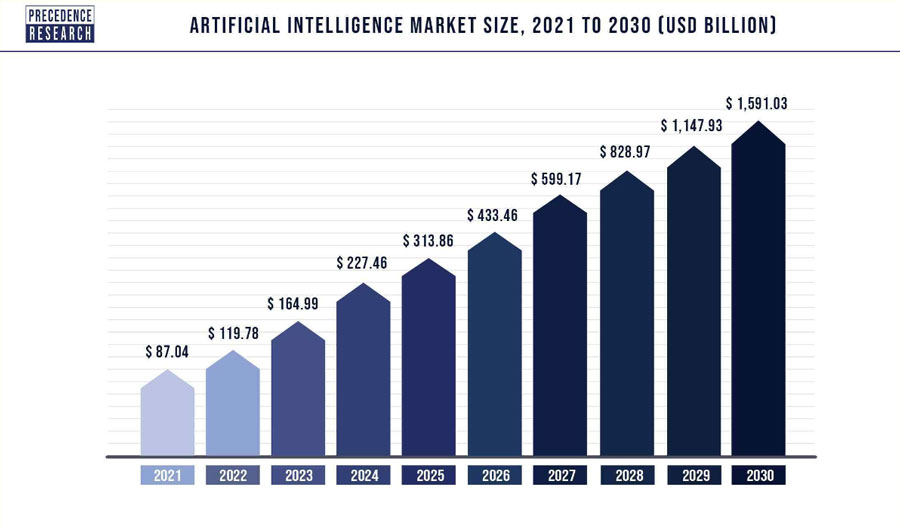

Big companies both admire and fear what popular generative AI’s like the ones produced by Open AI can do. The most repeated headline is the one saying how Google is on high alert because of ChatGPT because it could directly threaten its business model. AI has become a big force in the digital economy, as more and more companies are using it to deliver better services. AI companies are receiving great amounts of funds, and the industry is expected to reach $313,86 billion in 2025, and 1.597.1billion in 2030.

Image Source: Precedence Research

Image Source: Precedence Research

According to the World Economic Forum, AI will be responsible for creating 97 million jobs in 2025, some of which will be Data Sourcing, Data Annotators and Data Labelers, Data Analysts, AI engineers and DevOps.

One of the new job opportunities AI will create is the Prompting Engineer, which is responsible for using the right prompts for generative AI to obtain the exact desired result. It’s believed that, as generative AI models evolve, this role will be increasingly relevant. AI will have both consumer-level and professional-level applications, and while generative AI can produce impressive results, more complex prompts are often required to achieve specific goals.

Certainly, this type of technology is sparking a significant social debate across various domains. One area of concern is how companies that develop these artificial intelligences may potentially violate copyright laws. As a result, many generative AI companies are facing lawsuits, leading to the need for more clear legislation on the appropriate usage and limitations of the datasets used by machine learning models. Copilot is a prime example, having been hit with a class-action lawsuit for allegedly copying billions of lines of public code from Github, which could potentially be considered illegal.

Generative AI ethics is a growing concern, as no generative model can claim to be neutral:

“OpenAI, for instance, effectively decides whether ChatGPT takes stances on the death penalty (no opinion), torture (it’s opposed), and whether a man can get pregnant (it says no). With its AI illustrator Dall-E, the organization influences what type of a person the tech portrays when it draws a CEO. In each case, humans behind the scenes make decisions. And humans are influenceable”.

This serves as a reminder that generative AI can be biased, potentially perpetuating societal stereotypes and being subject to content moderation or censorship by its companies.

The metaverse refers to a virtual reality space where people can interact with a computer-generated environment and with each other, often using avatars (virtual representations of themselves). The term «metaverse» was first coined in Neal Stephenson’s 1992 science fiction novel «Snow Crash,» but has since been adopted by many people to describe the concept of a shared, immersive virtual world.

The metaverse is typically thought of as a fully realised, three-dimensional world that people can explore, interact with, and even create within. It is often imagined as a seamless and interconnected network of virtual spaces that people can move through just as they move through physical space in the real world, but we really can’t yet know the real shape that the different metaverses will look like.

We can think of the old metaverse created by Second Life, where you share your life with others in a virtual space, or we can think of Epic Games’ Fornite and its free access without VR equipment, with concerts like the one by Travis Scott with 27 million players attendance and with a Balenciaga high fashion collaboration with branded skins for sale.

Image Source: Campaign

Image Source: Campaign

On October 28th 2021, at Connect 2021, Mark Zuckerberg announced Meta to the world. This was not only a rebranding of Facebook; it was an attempt to clean facebook’s image after several years of scandals and a bad reputation.

Meta is also a holding company for all their products, such as Facebook, Instagram and Whatsapp. Facebook also created Meta to look into the digital future and try to lead the way to what is known as the metaverse. Supposedly a new era of the internet where Virtual Reality, Augmented Reality and Mixed Reality are embedded in the new social immersive internet experience, where you can go to class, work with your colleagues or go to virtual concerts.

The idea of the metaverse is not new, as many companies have been developing their own versions of this idea. Microsoft is working on his “Industrial Metaverse Stack”, Nvidia Omniverse to create and operate metaverse applications, and many other initiatives.

This new era of the internet mixes a lot of new technologies to make it possible. We are constantly reading headlines about all the buzzwords: Web3, NFT, DAO, Blockchain, VR/AR/MR, IoT, CryptoCurrencies, AI, 3D reconstruction, Digital Twins, Edge Computing and 5G, etc.

If this metaverse economy thrives and people adopt these technologies into their day-to-day lives, there’s a new window of opportunity for professionals all around the globe to take these new jobs: Avatar clothing designers, Data bounty hunters, Metaverse Event Directors, Ecosystem Developer, Metaverse Safety Manger or Hardware Creator, and many others.

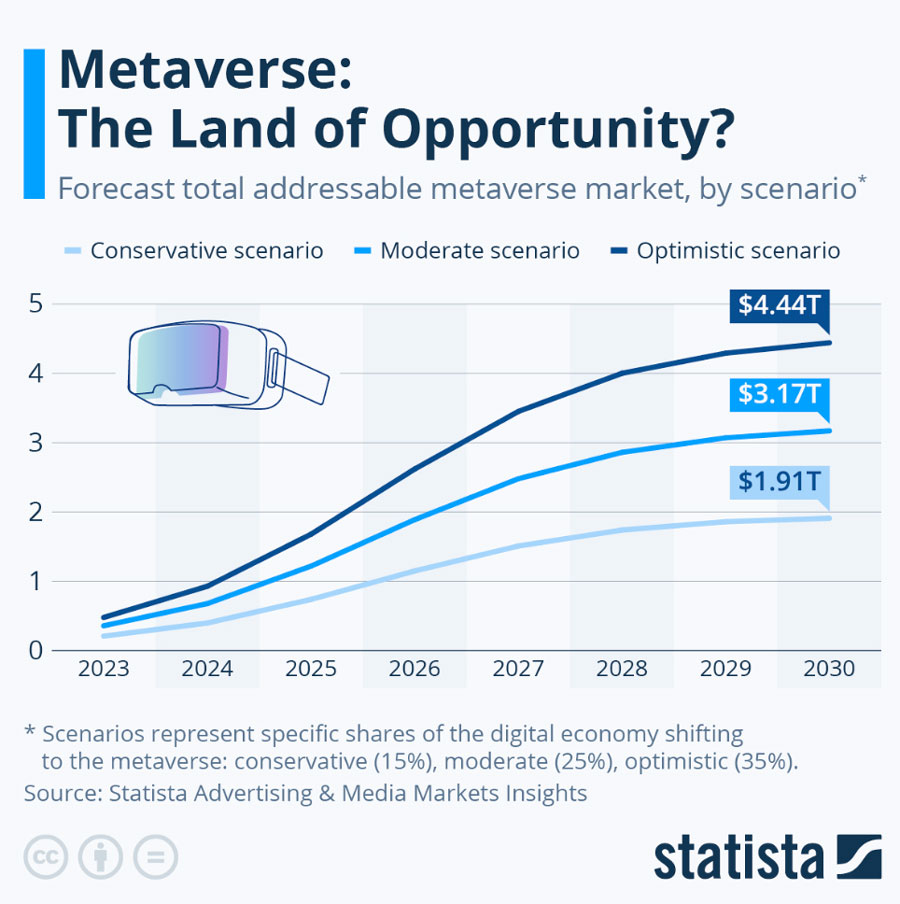

It’s believed that the metaverse market size in 2022 was around 61,8 billion and will rise to 426,9 billion in 2027 at a CAGR of 47,2%. It might reach 1.525,7 billion in 2030.

Image Source: Statista

Image Source: Statista

Meta and its CEO, Mark Zuckerberg, have faced significant financial losses in their investments in the metaverse. Despite this, the company still plans to invest in the metaverse in 2023. After rushing to be the first to bring this technology to the market, the company will now focus on efficiency and cutting expenses, reducing its planned investment from $34 – $37 billion to $30 – $33 billion through 2023. Metaverse technology is expected to become widespread by the end of this decade, and significant efforts are required to create the necessary technologies and infrastructure for it to work effectively.

The convergence of recent technologies in the metaverse makes it a promising technology that has the potential to bring significant value to consumers, professionals, companies, and governments.

We are seeing the beginnings of what’s known as the “2G and 3G switch-off” as the world moves to the more efficient and fast 4G and 5G networks. According to GSA (Global Mobile Suppliers Association):

“By the end of September 2022, GSA had identified 142 operators that have either completed, planned or are in progress with 2G and 3G switch-offs in 56 countries and territories”.

The first generation of mobile networks, known as GSM or 1G, was launched 44 years ago in Japan by NTT, a telecommunications company similar to the American AT&T. This network only allowed for voice calls, and no data could be shared, with no protection for communication.

2G (Second Generation Mobile Networks) were launched in 1991 in Finland over the existing GSM network, bringing many benefits:

- Basic data services allowed users to text and send pictures.

- Digital encryption enabled more secure phone conversations.

- Allowed a more efficient use of radio spectrum, reducing costs by enabling more users on each frequency band.

Today this network is considered old, and almost every country will switch it off at the end of this decade. Despite the imminent change, it’s still being used: “in rural areas as a fallback option when more modern networks like 4G or 5G have yet to be rolled out”. According to Streetwave, 2G offers wide-range coverage capability, has a globally standardised infrastructure, works well both indoors

and outdoors and uses less power than other networks. Some countries might switch off 3G networks before 2G because it is still relevant for the M2M market (IoT), as all devices are embedded with 2G.

In 1991 the Japanese NTT launched the 3G network:

This new network changed how consumers perceived mobile phones, seeing them less as voice-calling devices and more as social-connectivity devices. Where their fast connection, up to 14 Mbps, video calls, web-surfing, file-sharing, or online playing started in the years to come to become a reality.

4G was widely deployed in 2009 in Oslo and Stockholm by the telco Telia, reaching up to 100Mbps. This network is globally available, being slowly overtaken by 5G.

4G has helped greatly to shape the digital world we know today, from streaming services and apps to mobile-oriented companies, and has led to a global 67% smartphone penetration rate, being 82% in North America and 78% in Europe.

While 4G has served us well, 5G is drawing the interest of numerous industries as it has the potential to facilitate the continued growth, expansion, and progress of new technologies.

In 2019, the deployment of 5G was initiated through a collaborative effort of multiple organisations involved in the 3rd Generation Partnership Project (3GPP).

5G is around 100 times faster than 4G and has better latency, more bandwidth and increased security. One of the biggest changes with 5G technology is that it enables what’s called “Network Slicing”, allowing each antenna to “slice” its network area to connect multiple devices with different requirements.

This enables a multi-connected device system for the world we live in, with not only smartphones on the street but also self-driving cars, wearables, sensorized buildings and other IoT systems. 5G is also cloud-based and virtual, with many of its innovations based on software more than hardware.

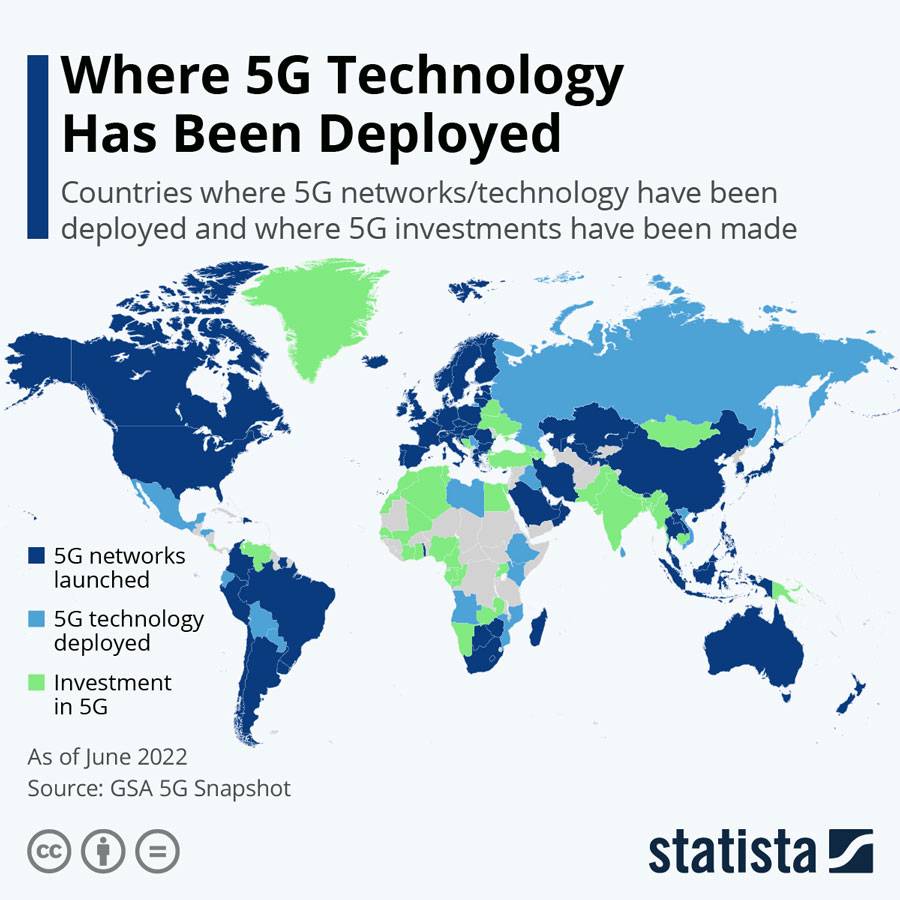

5G is currently being deployed all over the world, being the more developed countries the ones with faster adoption of this network.

Image Source: Statista

Image Source: Statista

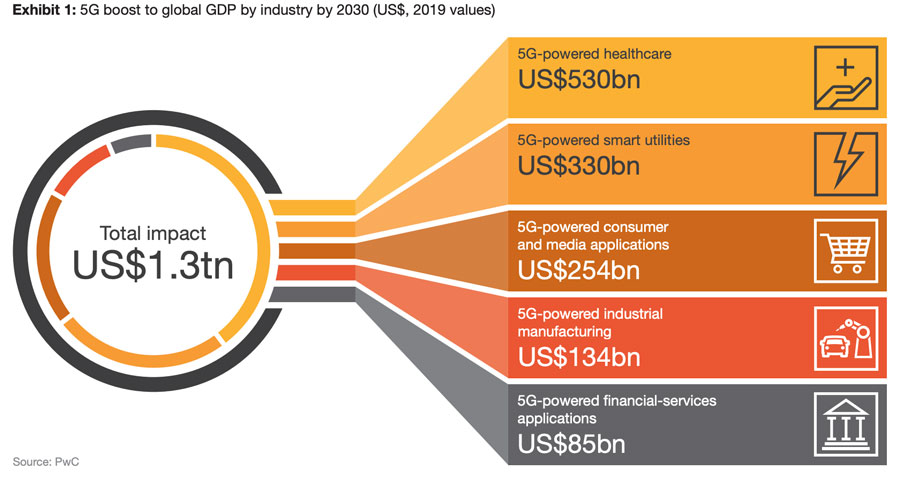

As you can see in the next graphic, it’s estimated that by 2030 5G will increase global GPD (Gross Domestic Product) by $1.3tn in different sectors, being healthcare the ones that will most benefit from this technology:

Image Source: PWC

Image Source: PWC

The tech industry has been leading the remote work revolution for years, and the Covid-19 pandemic has accelerated this trend, making social distancing and working from home the norm. Companies have had to adjust to this new reality, and the tech industry has been at the forefront of this transformation.

The impact of remote work on the tech industry has been massive, affecting corporate culture, employee productivity, and satisfaction. One of the major advantages of remote work in the tech industry is the capability to recruit talent globally. Since companies are no longer restricted to hiring from a particular geographic area, they can now hire the most talented individuals, regardless of their location.

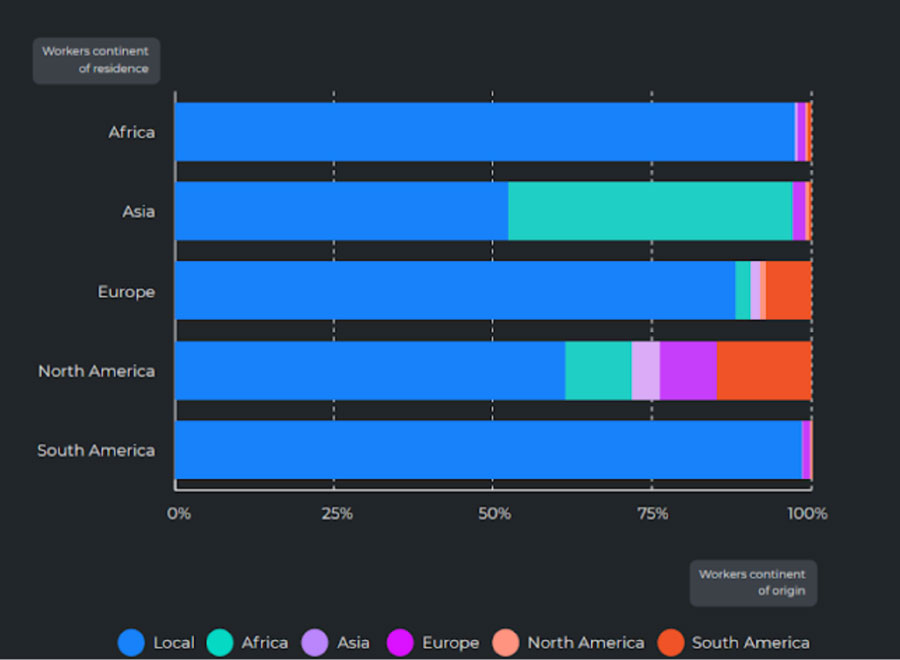

Landing Jobs has mapped workers’ movement between different continents, establishing the following results.

Image Source: Landing.Jobs

Image Source: Landing.Jobs

In the North American job market, there is a notable proportion of employees from different continents, particularly from Africa and South America (with the latter showing better compatibility with the time zone). The representation of European and Asian workers is relatively small. South America also has the most tech professionals working for companies across borders, especially in North America.

Despite the fact that the technology workforce in Europe is mainly made up of locals, South American employees are becoming an increasingly significant group. In addition, African workers are also gaining traction in Europe, likely due to their time zone compatibility being better than other regions.

In general, according to Landing Jobs, tech professionals are very open to relocating to another country or continent. Not only working remotely for a company across borders

is trending high, but relocating to another country or continent is now a real consideration for most tech professionals. The 2021 Gitlab Remote Work report calls this trend “the great relocation”. At the time, their data claimed 1 out 3 workers planned to relocate and work abroad.

Image Source: GitLab

Image Source: GitLab

The biggest shift to working lives has undoubtedly been location-based, as many people have noticed that with the right tools, it’s possible to be productive and maintain business continuity throughout remote working. This has opened up opportunities for companies to expand their talent pool and tap into a global workforce, leading to more diverse and skilled teams. Furthermore, the shift towards remote work and a globalised workforce has placed new demands on workers, such as the ability to collaborate effectively in virtual teams and communicate across cultures.

Image Source: Owl Labs

Image Source: Owl Labs

The globalisation of the tech workforce has also highlighted the importance of language skills in the tech industry. English has traditionally been the dominant language in the tech industry, but as companies increasingly hire from non-English speaking countries, a new type of skills gap has been created, where job seekers who aren’t fluent in English may be at a disadvantage. This can limit the diversity of perspectives and ideas within the industry and lead to a lack of representation of certain groups.

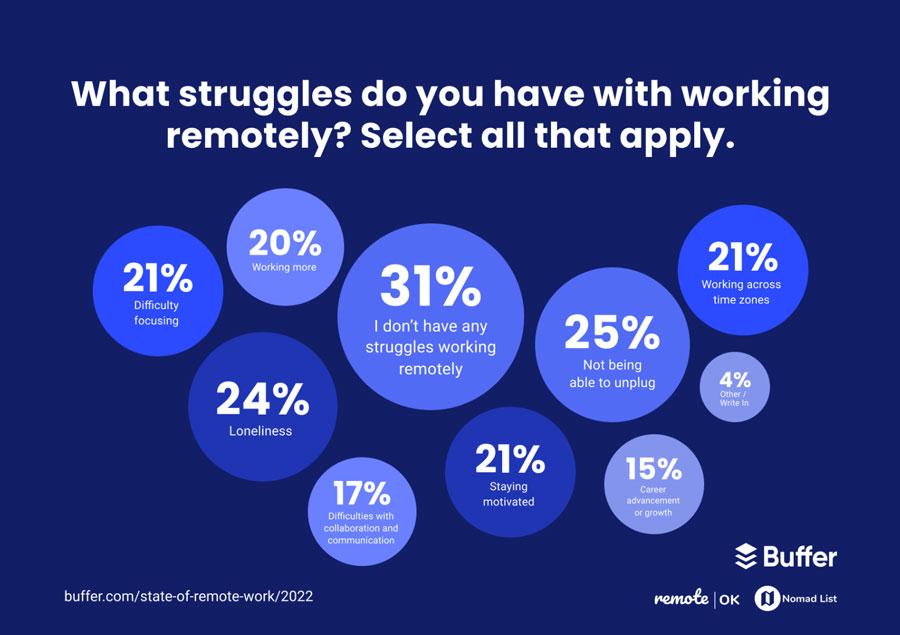

While remote work has many benefits, it also comes with its own set of challenges. Some of the main challenges include difficulty in maintaining a work-life balance, communication issues, isolation, lack of access to proper equipment and infrastructure, and potential security risks. According to data from the Owl Labs report on remote and hybrid work, 42% of workers are concerned that working remotely will impact their career progression, and 41% find it hard to fit into the company’s culture when working remotely.

Moreover, remote workers may find it challenging to separate work and personal life, as the boundaries between the two may become blurred. It is important for both employers and employees to address these challenges proactively and find ways to mitigate them to ensure a successful remote work experience.

Image Source: World Economic Forum

Image Source: World Economic Forum

To handle the challenges of a recession, business leaders need to communicate their plans and strategies proactively. They should show empathy and support towards affected workers, which will earn them respect and trust. It is crucial to address all the needs of the employees, not just their monetary requirements. The workplace should be a safe haven for employees, which makes them feel included, provides them with job flexibility, and enables them to maintain a healthy work-life balance. Creating such a conducive work environment must be a top priority for business leaders.

By 2025, cybercrime is expected to reach $10.5 trillion, making up 50.48% of the total digital economy. This indicates that cybercrime is growing more rapidly than the healthy digital economy, presenting significant challenges for companies but also great opportunities for cybersecurity professionals worldwide.

Currently, cybercrime costs the global economy $6 trillion, accounting for 43% of the Digital Economy. These professionals are among the better digital paid professionals, as you can see here.

As the specialist Steve Morgan states in Cybersecurity Ventures:

“Over an eight-year period tracked by Cybersecurity Ventures, the number of unfilled cybersecurity jobs grew by 350 per cent, from one million positions in 2013 to 3.5 million in 2021. For the first time in a decade, the cybersecurity skills gap is levelling off. Looking five years ahead, we predict the same number of openings in 2025”.

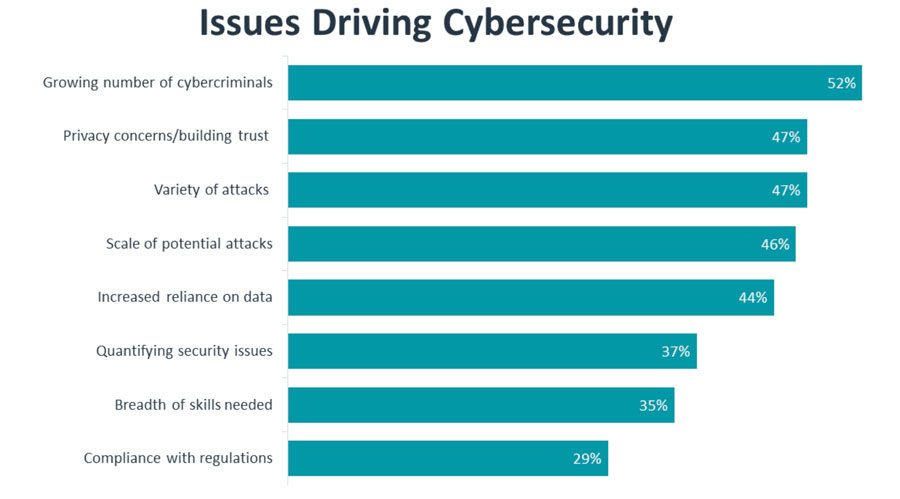

As highlighted in CompTIA’s 2022 State of Cybersecurity report, companies worldwide face various cybersecurity challenges. One of the key issues is the disconnect between the root causes of cyberattacks and their symptoms, which is a major pain point for many organisations.

Image Source: CompTIA

Image Source: CompTIA

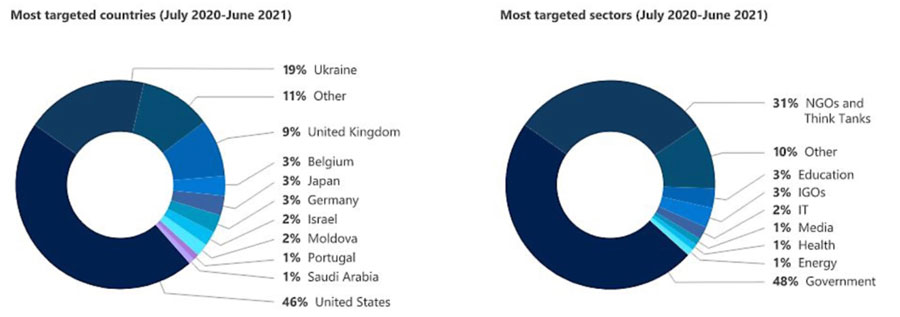

According to Microsoft’s Digital Defense Report, cybercrime is increasing due to various threats and evolving methods of attack, including ransomware, phishing, and cybercrime as a service. Weak security measures, incomplete data protection strategies, and ineffective operations are contributing factors. Internet of Things (IoT) devices are also increasingly vulnerable to cyberattacks.

Hacktivism is on the rise, with private citizens conducting cyberattacks for social or political reasons. A comprehensive response is needed to combat these growing threats.

Cybersecurity is increasingly being recognised as a national security issue by many countries worldwide. This is due to the significant impact that cyberattacks can have on critical infrastructure, government operations, and the economy. A successful cyberattack can cause widespread disruption, financial loss, and even loss of life.

As a result, governments are investing in cybersecurity measures and partnerships with the private sector to protect their citizens and assets from cyber threats. The stakes are high, and the need for strong cybersecurity has become a priority for many nations.

Image Source: Microsoft

Image Source: Microsoft

As the world becomes increasingly digital, the risk of cyberattacks also grows. According to the World Economic Forum report, 2022 Global Cybersecurity, emerging technologies such as AI, robotics, and the internet of things (IoT) present new vulnerabilities that leaders must consider when adopting new systems. The potential impact of automation and machine learning on cybersecurity is a significant concern for many, with experts predicting that these techniques will upend the traditional balance between attack and defense.

Overcoming the barriers to achieving higher cyber resilience levels will require a collaborative effort from both the public and private sectors. It is essential to incorporate cybersecurity and cyber resilience into leadership thinking and analytical processes to prepare for potential cyber disasters and improve overall cyber resilience.

The digital tech industry has a complex relationship with sustainability. On the one hand, the industry is often viewed as a key enabler of sustainability by developing innovative technologies that can help reduce environmental impacts and promote sustainable practices.

On the other hand, the industry is also a significant consumer of energy and natural resources, and the rapid growth of digital technologies has contributed to the proliferation of electronic waste and other environmental challenges. As a result, there is a growing awareness within the industry of the need to balance the benefits of technology with the need for sustainability, and many companies are actively working to reduce their environmental footprint and promote sustainable practices.

Initiatives such as the Network for the Digital Economy and Environment aim to promote scientific and academic research on the environmental impact of digital technologies like Artificial Intelligence, Blockchain, the Internet of Things, and Sharing Economy.

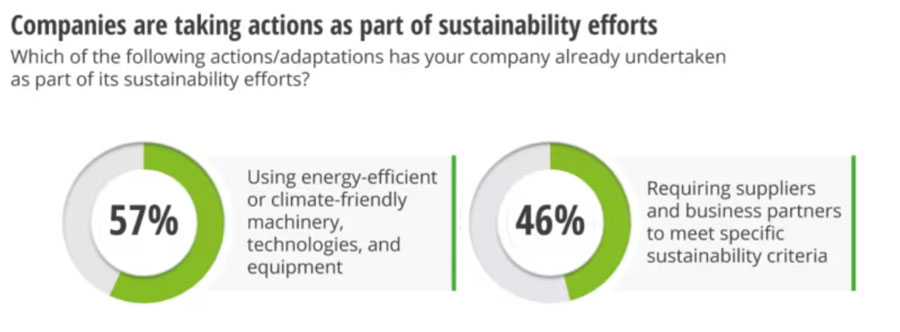

The focus on environmental sustainability remains a top priority for both consumers and boardrooms, with climate change taking centre stage. According to a Deloitte survey, 98% of consumers believe that brands are responsible for improving the world, and 40% prefer to purchase sustainable products. The same survey found that 35% of consumer product executives feel that consumer attitudes have a greater impact on driving their companies towards sustainability compared to investor demands, boards, or other stakeholders.

Image Source: Deloitte

Image Source: Deloitte

According to a KPMG report, On average, 80% of N100 companies worldwide report on sustainability, with a 5% increase since the last KPMG survey in 2017. The technology sector’s reporting rate is slightly higher at 83%.

The research also shows that N100 companies are catching up with the G250, which has reported on sustainability since 2011, with over 90% reporting. While the G250’s sustainability reporting rate fluctuates marginally year-to-year due to changes in the group of companies, it’s likely that the N100 reporting rate will continue to climb steadily.

In Deloitte’s 2022 CxO Sustainability Report: The Disconnect Between Ambition and Impact surveyed C-level business leaders’ claim to feel increaiginly apprehensive about the environment, but they also express optimism.

Nearly 90% of respondents agreed that with immediate action, we still can limit the worst impacts of climate change. That figure was just 63% in the previous survey. Despite their positive outlook, C-suite executives struggle to embed climate considerations into their culture and strategy and obtain meaningful transformation.

Image Source: Deloitte

Image Source: Deloitte

One of the biggest sectors demanding talent is ICT (Information and Communications Technology), as there is a big skills gap previously discussed deeply in this report. As observed in this rating, many of the best-paid jobs today are roles in digital technology.

The World Economic Forum outlines the following video how new emerging technologies like AI are causing disruptions in the job market and suggests measures that companies and governments can take to address this issue. The most effective solution is to provide employees with education and training to upskill or reskill, as it is projected that by 2025, 85 million jobs could be displaced by technology while 97 million new jobs, more suited to the changing landscape, may emerge.

The World Economic Forum has created the “Reskilling Revolution” program that aims to: “empower one billion people with better education, skills and economic opportunity by 2030”.

Image Source: World Economic Forum

Image Source: World Economic Forum

In today’s fast-paced world, the ability to adapt and learn new skills quickly is more important than ever. Upskilling and reskilling are essential for individuals who want to remain relevant and competitive in their careers as new technologies and industries emerge.

At the company level, upskilling and reskilling can help ensure that employees have the skills they need to meet the changing demands of the business and can help companies stay competitive in the marketplace. It can also improve employee retention and job satisfaction, as workers are given opportunities to learn and grow within their roles.

On a national level, upskilling and reskilling can play a critical role in ensuring the workforce is prepared for the jobs of the future. Governments and educational institutions can provide training and education programs to help individuals gain the skills they need to thrive in the new economy while also addressing issues such as income inequality and unemployment.

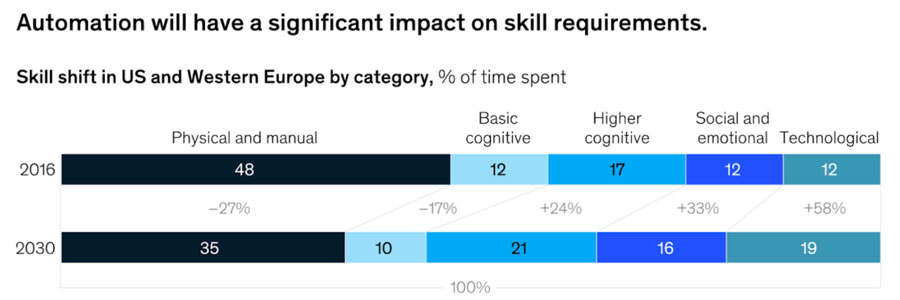

According to McKinsey, physical and manual skills in predictable and repeatable tasks are anticipated to decrease by approximately 30% in Europe and the United States. Meanwhile, the requirement for basic literacy and numeracy skills is expected to drop by almost 20%. However, the demand for technological skills, particularly the interaction with technology, is expected to rise by over 50%, and the necessity for complex cognitive skills is expected to increase by 33%. High-level social and emotional skills, such as initiative-taking, leadership, and entrepreneurship, are also predicted to increase by more than 30%.

Image Source: McKinsey & Company

Image Source: McKinsey & Company

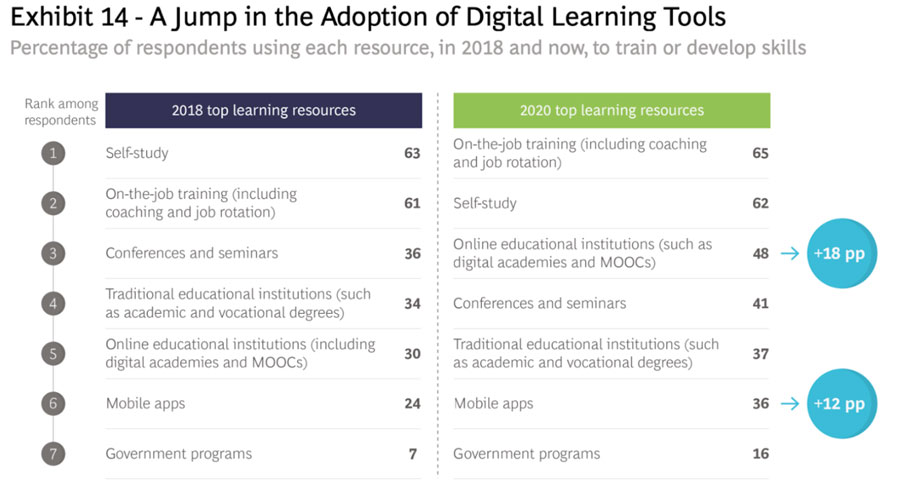

The ways in which people learn digital skills have evolved over time. In the past, people may have relied on traditional classroom-based instruction or self-study. However, new ways of learning have emerged with the rise of the internet and digital technology. Online courses, interactive tutorials, and video-based learning are just a few examples of the many options available for learning digital skills.

These methods allow people to learn at their own pace and on their own schedule, often without the need for expensive textbooks or other materials. Additionally, many digital skills can be learned through hands-on practice, which can be facilitated through virtual environments or simulated work scenarios. Overall, the availability of digital learning resources has made it easier than ever for people to acquire the skills they need to succeed in a rapidly changing digital landscape.

Image Source: BCG

Image Source: BCG

Investing in upskilling and reskilling existing employees can be more cost-effective for a company than hiring new workers. This is because upskilling programs can help close skills gaps within the company, reduce turnover, and increase productivity. Upskilling also demonstrates to employees that the company values their development and encourages loyalty, which can result in higher job satisfaction and engagement.

In contrast, hiring new workers can be expensive, as it requires recruiting, training, and onboarding costs, and there is always a risk that new hires may not be a good fit for the company culture.

Overall, upskilling can be a win-win solution for both the company and its employees.

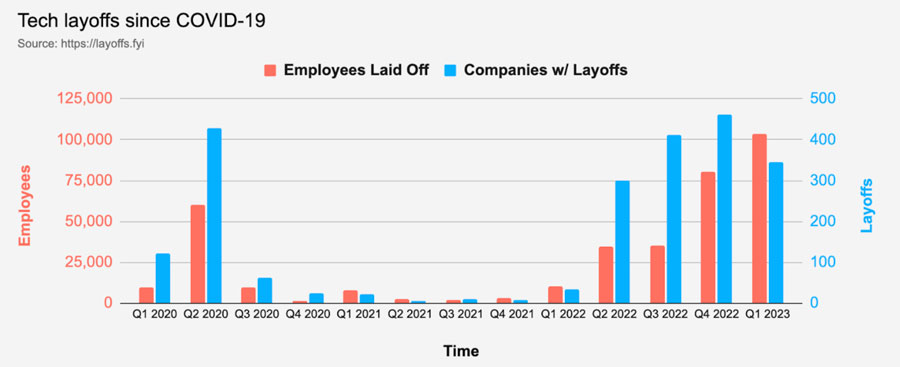

As Covid-19 made its way into our lives, the need for digital solutions in the personal, professional, educational and public sectors increased. Companies in different sectors were in need of tech professionals, and digital companies started to hire people quickly to grow their teams as the demand for online services was very high. This led to a miscalculation of how long the pandemic would be or how high the digital economy would grow in the next years.

When the pandemic’s effects slowed down and most of the world started to enter the post-pandemic era, digital tech companies worldwide began to readjust their workforce due to this “overhiring”.

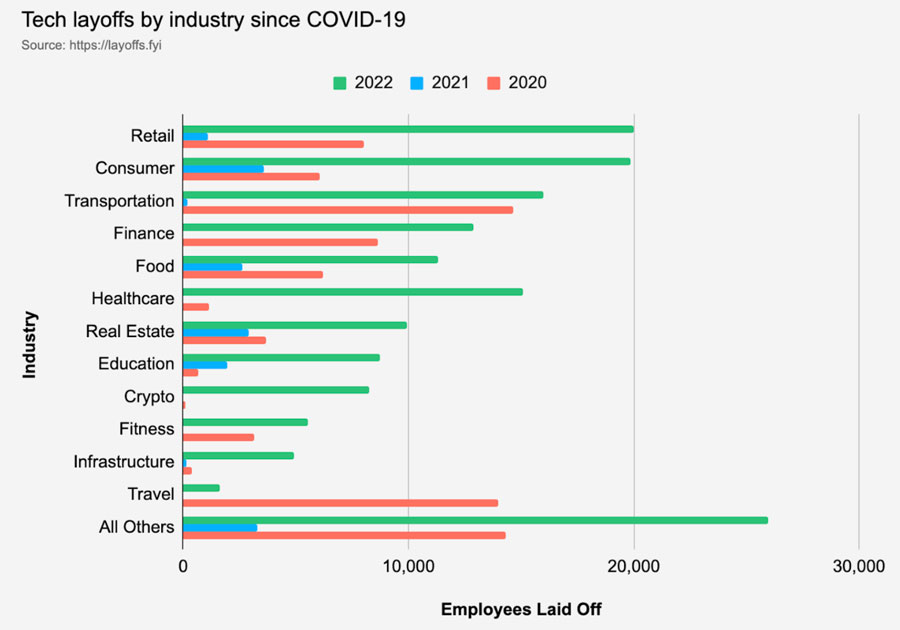

According to Layoffs.fyi, 1.045 companies made 160.097 layoffs in 2022, and just in January and mid-February 2023, 356 companies laid off 104.557 employees.

The following chart illustrates the number of employees who have been laid off since the onset of the Covid-19 pandemic, as well as the number of companies that have implemented layoffs.

Image Source: Layoffs.fyi