Of the 50 sovereign European states recognised by the United Nations, only 27 are members of the European Union. Ironhack has a presence in 6 countries across geographical Europa: Spain, Portugal, France, Germany, Netherlands and the UK.

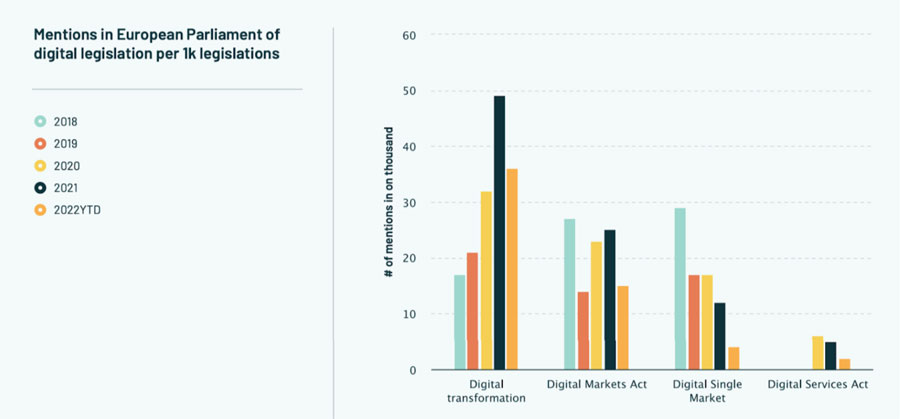

The European Union created, in 2015, the Digital Single Market, which aims to make digital life between European countries much easier. For Europe to become digitally advanced, it needs to remove unnecessary regulatory barriers and transition from separate national markets to one EU-wide regulation. These changes could lead to the significant economic growth of up to €415 billion annually, benefiting job creation, competition, investment, and innovation within the EU.

The EU’s Digital Single Market Strategy is built on three pillars:

- Access: better access for consumers and businesses to digital goods and services across Europe.

- Environment: creating the right conditions and a level playing field for digital networks and innovative services to flourish.

- Economy & Society: maximising the growth potential of the digital economy.

The goal is to create a European model for data, technology and infrastructure that “strengthen its digital sovereignty and set standards”.

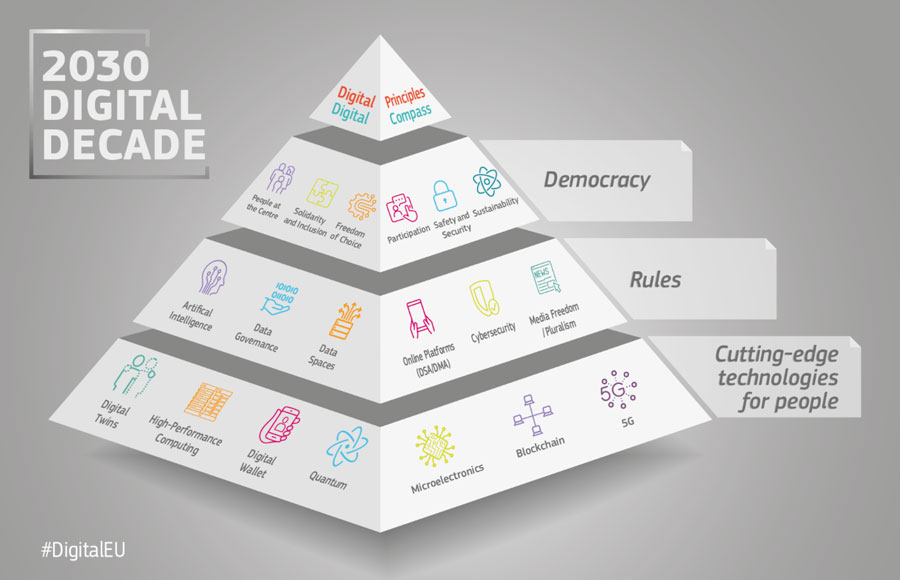

As part of the Digital Single Market initiative, the EU intends to offer a European Digital Identity to all EU citizens. This will standardise identification, legal documentation, traffic tickets, and other aspects, enabling access, payment, and modification of personal information through a single app. These endeavours are part of the EU’s Digital Decade plan, which aims to transform the digital landscape in the coming years:

«The digital world should be based on European values – where no one is left behind, everyone enjoys freedom, protection and fairness. Europe’s Digital Decade is where everyone has the skills to use everyday technology. […] Connectivity reaches people living in villages, mountains and remote areas, so everyone can reach online opportunities and participate in the benefits of the digital society.

Key public services and administrative procedures are online for the convenience of citizens and businesses. The Digital Decade is a comprehensive framework that will guide all actions related to digital. The aim of the Digital Decade is to ensure all aspects of technology and innovation work for people”.

Image Source: European Commision

Image Source: European Commision

The EU’s Digital Decade program is focused on achieving four primary objectives. These include developing a digitally competent population and a workforce consisting of highly skilled digital professionals.

The program also aims to establish secure and sustainable digital infrastructures, facilitate digital transformation for businesses, and promote the digitalisation of public services. The EU intends to work towards these goals to ensure that its citizens are equipped to navigate the increasingly digital landscape of the future.

The EU’s Digital Decade program hopes to achieve several main objectives. The program is focused on creating a safe and secure digital world, enabling everyone to participate in digital opportunities, and ensuring that no one is left behind. Additionally, the program aims to provide small businesses and industries with access to data and digital technologies while promoting the convergence of innovative infrastructures to work together.

The EU also seeks to ensure that small and mid-sized enterprises can compete in the digital world on fair terms and that public services are readily available online. Furthermore, the program emphasises research that focuses on developing and measuring the impact of sustainable, energy and resource-efficient innovations. Finally, the EU intends to ensure that all organisations can maintain cybersecurity to protect their digital assets.

The European program aims to achieve the following primary objectives:

- A safe & secure digital world.

- Everyone can participate in digital opportunities / no one is left behind.

- Small businesses and industries have access to data.

- Start-ups & SMEs (Small and mid-size enterprises) have access to digital tech.

- Innovative infrastructures converge to work together.

- SMEs can compete in the digital world on fair terms.

- Public services are readily available online.

- Research is focussed on developing and measuring the impact of sustainable, energy and resource-efficient innovations.

- All organisations can ensure cybersecurity.

Here you can discover the European Digital Targets for 2030 and beyond.

The European Union’s Digital Decade goals are currently progressing at a slower pace than expected. At the current rate, it is estimated that the goals will not be met until 2040, a decade behind schedule. The EU’s projected economic value by 2030 is €1.3 trillion, which is considerably lower than the potential value of €2.8 trillion if the goals were to be achieved on time. However, if the progress towards the Digital Decade goals can be accelerated, there is a possibility of unlocking up to €1.5 trillion in additional economic value by 2030.

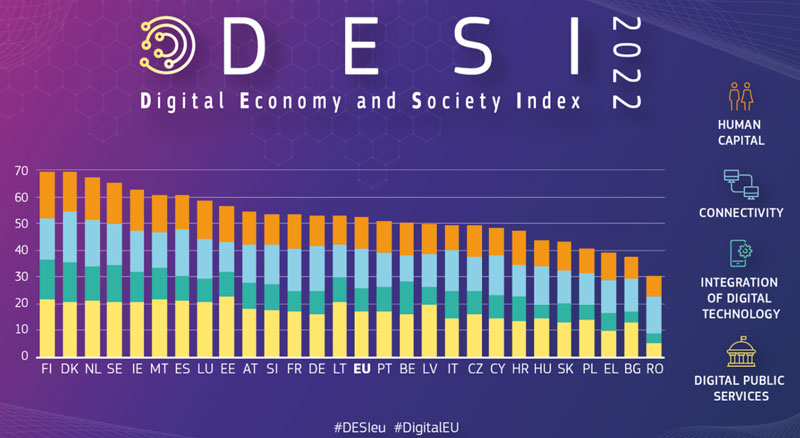

In order to monitor the progress of digitalisation and innovation in each country, the EU employs two separate analyses: the Digital Economy and Society Index (DESI) and the European Innovation Scoreboard. Since 2014, DESI has been tracking member states’ digital progress across four areas: human capital, connectivity, integration of digital technology, and digital public services.

On the other hand, the European Innovation Scoreboard (EIS) provides a comparative assessment of research and innovation performance among EU member states and selected third countries, identifying the relative strengths and weaknesses of their research and innovation systems. These tools allow the EU to better understand each country’s advancements in digitalisation and innovation and to develop strategies for further improvement.

The DESI 2022 results show that while most EU member states are progressing in their digital transformation, there is still low adoption of key digital technologies by businesses and insufficient digital skills among the population. Finland, Denmark, the Netherlands, and Sweden are still the frontrunners, but they also face digital challenges.

Image Source: European Commission

Image Source: European Commission

Human Capital

In 2021, 87% of people aged 16-74 used the internet regularly, but only 54% had basic digital skills. The Netherlands and Finland lead the EU in digital skills, while Romania and Bulgaria lag behind. There is a shortage of ICT specialists in the EU labour market, with 55% of enterprises having difficulty filling vacancies.

Additionally, there is a gender imbalance, with only 19% of ICT specialists and one in three STEM graduates being women. The Path to the Digital Decade proposal aims to increase the number of employed ICT specialists to at least 20 million by 2030, compared to 8.9 million in 2021. Sweden and Finland currently have the highest proportion of ICT specialists in their labour force.

Connectivity

The EU has full broadband coverage, but only 70% of households can access fixed, very high-capacity network (VHCN) connectivity with gigabit speeds. FTTP coverage increased from 43% to 50% in 2021, while DOCSIS 3.1 coverage increased from 28% to 32%. Malta, Luxembourg, Denmark, Spain, Latvia, the Netherlands, and Portugal have the highest fixed VHCN coverage. 5G coverage also increased to 66% of populated areas, but only 56% of the total 5G harmonised spectrum has been assigned, which limits the deployment of advanced applications.

Integration of digital technology

In 2021, only 55% of small and medium-sized enterprises (SMEs) in the EU have adopted basic digital technologies. Finland and Sweden have the most digitalised SMEs, while Romania and Bulgaria have the lowest rates. By 2030, the Digital Decade target is to have at least 90% of SMEs with a basic level of digital intensity. Although more companies are becoming digitalised, the use of advanced digital technologies such as AI and big data remains low. At least 75% of companies should adopt AI, cloud, and big data technologies by 2030, as per the Path to the Digital Decade proposal. Finland, Denmark, and Sweden are the most digitally transformed countries for businesses.

Digital public services

In 2021, the quality scores for digital public services for citizens and businesses reached 75 out of 100 and 82 out of 100, respectively. Among the Member States, Estonia, Finland, Malta, and the Netherlands have the highest scores, while Romania and Greece have the lowest. The proposed target of the Path to the Digital Decade is to ensure that all key public services for citizens and businesses are fully available online by 2030.

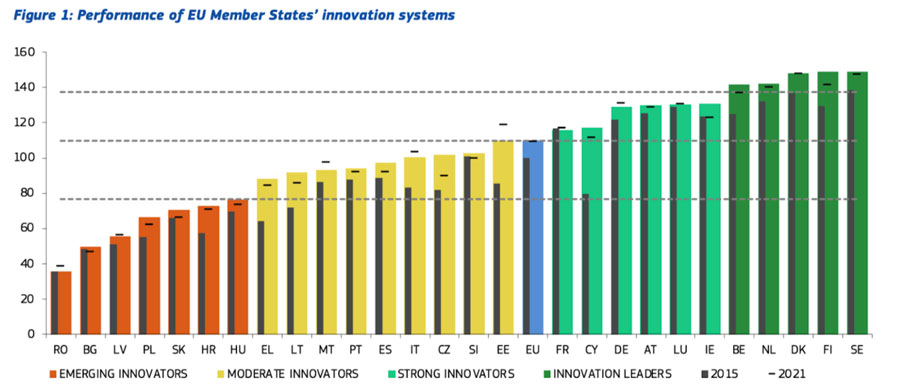

The European Innovation Scoreboard (EIS) assesses the research and innovation performance of EU Member States and selected third countries. Almost all EU Member States have increased their innovation performance since 2015, with the EU increasing by 9.9 percentage points.

Business process innovators, international scientific co-publications, and innovative SMEs collaborating with others were the indicators with the highest improvements. However, the lowest-performing countries are falling further behind.

Member States fall into four performance groups: Innovation Leaders, Strong Innovators, Moderate Innovators, and Emerging Innovators. Belgium, Denmark, Finland, the Netherlands, and Sweden are Innovation Leaders, while Bulgaria, Croatia, Hungary, Latvia, Poland, Romania, and Slovakia are Emerging Innovators.

Image Source: European Commission

Image Source: European Commission

The achievement of gigabit connectivity throughout Europe by 2030 is vital for ensuring that every business and citizen can participate in society. This goal can be attained using any technology, but it is recommended that the focus is on next-generation, sustainable fixed, mobile, and satellite connectivity. As the decade progresses, households, schools, hospitals, and businesses will all require high-speed data infrastructures for cloud computing, eEducation, eHealth, and high-performance computing, with new digital features and capabilities expected to become available, providing a new perspective to a digitally enabled society.

According to the Dutch VPN company Surfshark and their Digital Quality of Life (DQL) Index, which examines digital quality across countries, seven of the top-ranking nations are located in Europe.

This index looks at 5 indicators:

- Internet affordability.

- Internet quality.

- Electronic infrastructure.

- Electronic security.

- Electronic government.

Image Source: Surfshark

Image Source: Surfshark

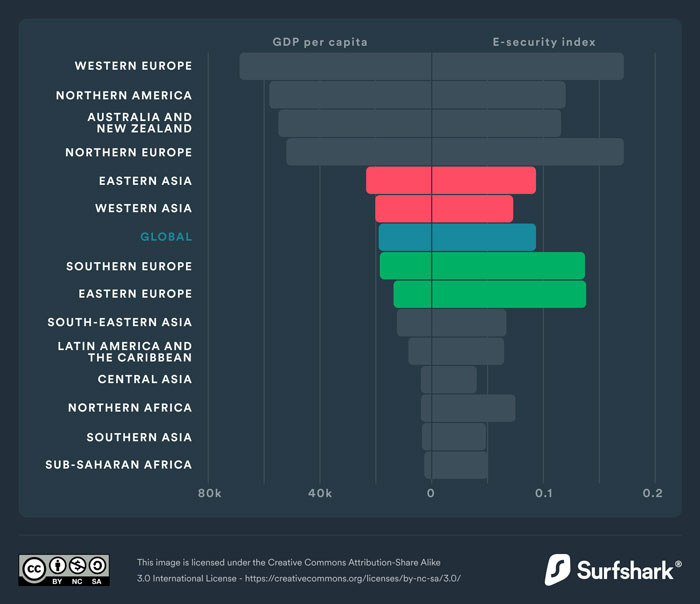

The European countries with the highest Digital Quality of Life are also highly ranked globally in terms of their Gross Domestic Product (GDP), according to the World Bank.

Although Europe is among the wealthiest continents with the highest level of Digital Quality of Life, as shown in the following graph, a larger GDP does not always correspond to better Digital Quality of Life. This difference is particularly noticeable in southern and eastern Europe.

Image Source: Surfshark

Image Source: Surfshark

According to data by Digital Europe, in their Mind The Gap report, the majority of experts support the EU target of bringing 100 Mbps connections to all European households by 2025. However, some experts find them insufficient. These experts argue that the current targets are not ambitious enough given the available technology, with several markets already offering multi-gigabit services up to 10 Gbit/s and 25 Gbit/s services emerging, with 50 Gbit/s services expected to be available in the coming years.

The experts surveyed by Digital Europe agree that the targets should be considered a starting point and not a limit and should not only be used to catch up with the deployment of gigabit networks but rather as a minimum that Europe should strive for in the global technology competition.

Statista’s data indicates that the value of the data economy in the 27 EU countries and the United Kingdom was estimated to be over 440 billion euros in 2020. The data economy encompasses the overall impact of the data market on the economy, which includes generating, collecting, storing, processing and exploiting data using digital technologies. The value of the Data Economy is only expected to grow as it becomes a focus for the European Union.

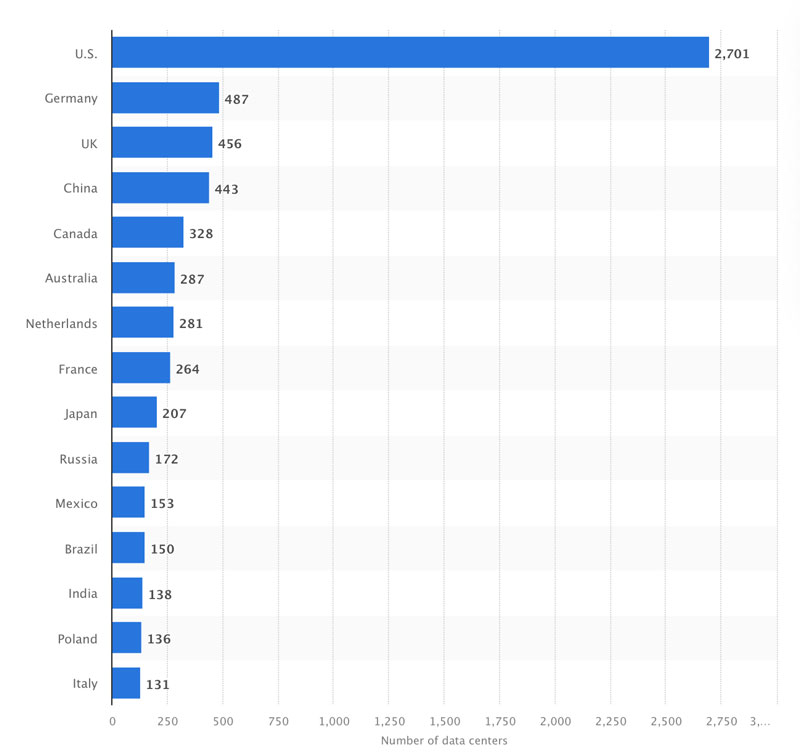

Data Centers play a crucial role in the overall Data Economy, as they are essential to maintain the infrastructure that supports it. According to Statista, the US has almost 4.5 times more Data Centers (2,701) than any other country, with Germany (487) and the UK (456) following closely behind. The top 15 also include the Netherlands and France.

Once again, this highlights Europe’s strong position globally, emphasising the significance of the digital economy in the continent.

Image Source: Statista

Image Source: Statista

The Data Centers Market, which includes all hardware-related expenses incurred when establishing and maintaining an IT infrastructure, continues to grow globally at a fast pace. Cloud services have evolved into a strategic factor for tenants, developers, and investors interested in new markets. Major cloud service providers now offer assurance for future scalability and validation of market fundamentals, making them a key determinant for investment decisions.

The past year has seen a surge of interest in secondary markets like Madrid, Milan, Zurich, Berlin, Warsaw, Oslo, and Barcelona. Meanwhile, official regulations have shed light on the political challenges in Amsterdam, Frankfurt, and Dublin, with efforts to reduce pressure on local resources and promote sustainable development. Both large and small markets offer opportunities for savvy investors as the region’s development activity remains on an upward trend.

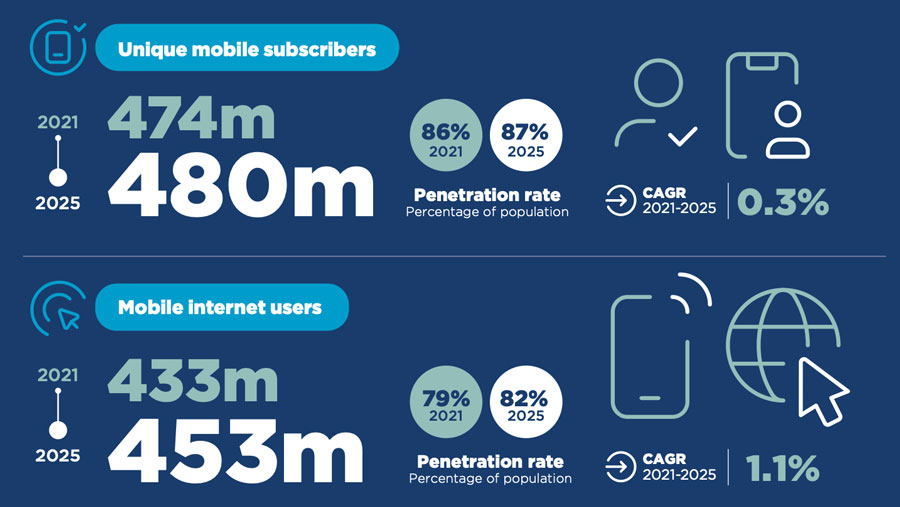

As the mobile market continues to expand, 5G technology has become increasingly crucial to facilitate the latest innovations in digital technology, such as the metaverse. Currently, 86% of Europeans are mobile subscribers, with 79% using mobile internet. These figures are expected to rise by 2025.

Image Source: GSMA

Image Source: GSMA

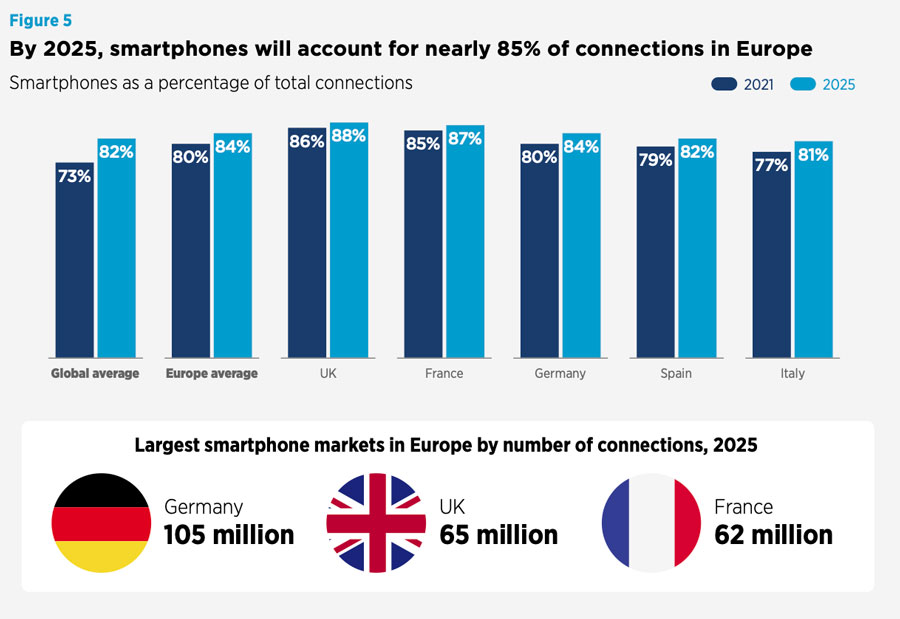

Furthermore, it is projected that 85% of all internet connections in Europe will be made through smartphones by 2025. The countries leading in smartphone penetration in 2021 are Germany, the UK, and France, followed by Spain and Italy, as illustrated in the chart below.

Image Source: GSMA

Image Source: GSMA

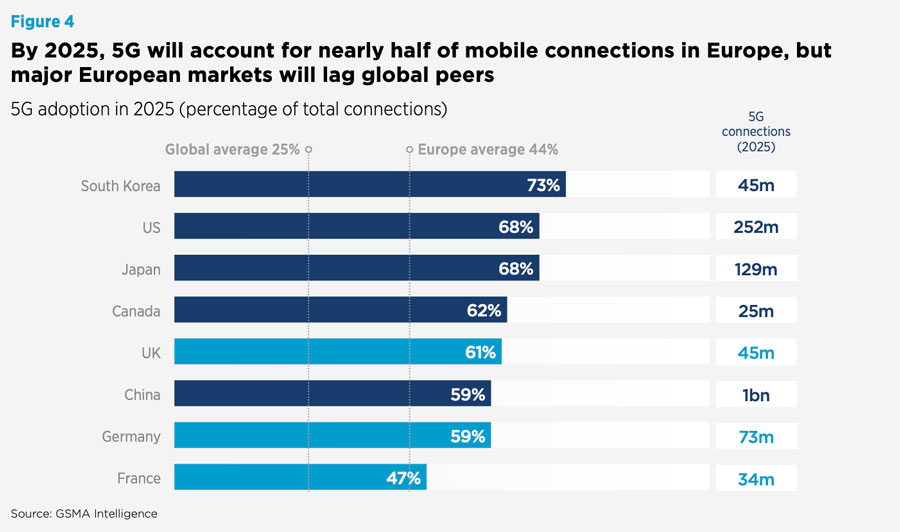

Despite significant efforts to develop infrastructure and provide 5G networks to its population, Europe has lagged behind other countries in adopting this technology. While the majority of European countries have deployed commercial 5G services, and nearly two-thirds of operators in the region have launched 5G networks, Europe still lags behind global leaders such as Japan, South Korea, and the US in terms of adoption. By 2025, it is predicted that there will be 311 million 5G connections across Europe, representing a 44% adoption rate.

Image Source: GSMA

Image Source: GSMA

The European 5G Observatory provides quarterly reports on the progress of the 5G network in Europe. These reports allow us to gain a more comprehensive understanding of the ongoing efforts, processes, and advancements being made by European countries and the European Union as a whole.

The Covid-19 pandemic has accelerated the digital transformation in Europe as governments, businesses, and individuals have had to adapt to new ways of working, learning, and communicating. The pandemic has highlighted the importance of digital infrastructure, tools, and services in maintaining business continuity, providing remote access to healthcare and education, and enabling social interactions while adhering to social distancing measures.

The crisis has fueled the conversation around digitalisation, with increased investments and initiatives to strengthen digital infrastructure, upskill the workforce, and promote digital innovation across sectors.

Image Source: Atomico

Image Source: Atomico

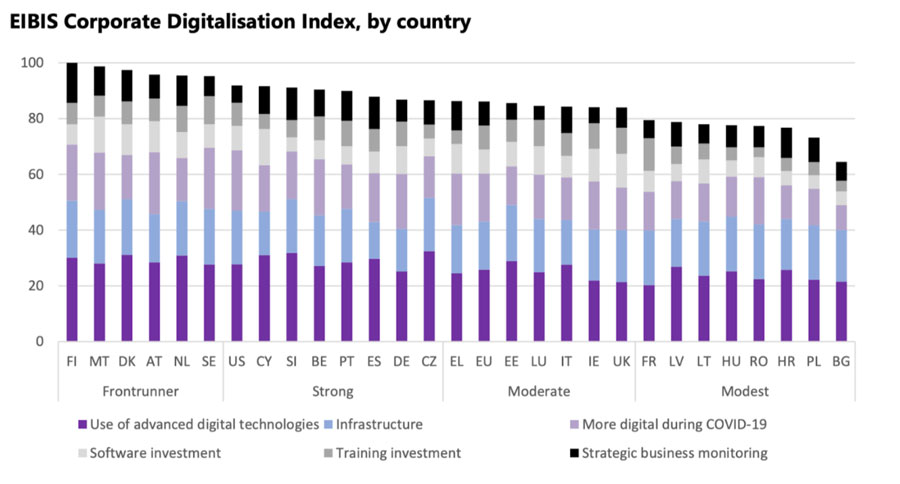

Based on the results of EIBIS’s report on digitalisation, 46% of businesses within the European Union took measures to enhance their digital capabilities during the first stage of the pandemic. Nonetheless, the data highlights noticeable variations among different firm sizes, industries, and nations.

In particular, in Western and Northern Europe, almost half of the firms (48%) adopted digital measures, compared to 43% in Southern Europe and 37% in Central and Eastern Europe. Business and public response to fast digitalisation and their ability to adapt rapidly to new consumer needs are factors that determine a country’s digitalisation performance, according to EIBIS.

Image Source: European Investment Bank

Image Source: European Investment Bank

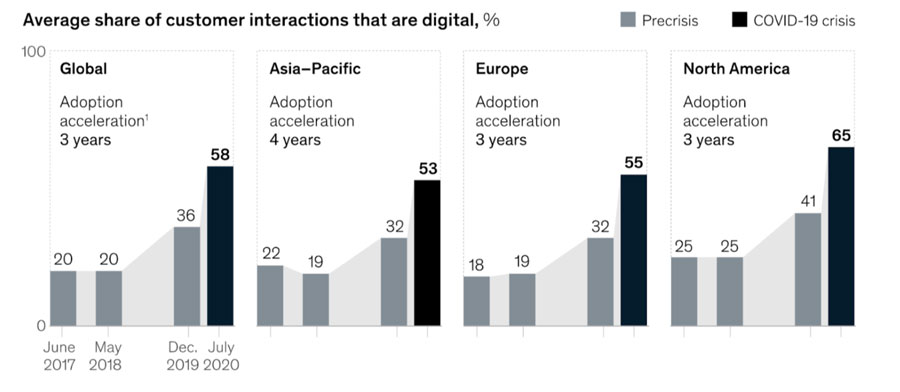

During the pandemic, digitalisation hasn’t just been adopted by governments and companies: consumers have also shifted towards online channels, leading to a corresponding response from companies and industries. The findings from a McKinsey survey affirm the rapid transition towards engaging with customers via digital means, surpassing the rates of adoption recorded in previous surveys.

Since the outbreak of the pandemic, there has been a significant shift towards digital products and services among consumers in Europe. With restrictions on physical movement and the closure of many businesses, consumers turned to online channels for everything from shopping and entertainment to communication and education. This shift has been particularly evident in areas such as e-commerce, online streaming, and teleconferencing, which have seen a surge in demand.

In addition, the pandemic has accelerated the adoption of digital payment methods, as consumers have sought to minimize physical contact and reduce the risk of infection. Now, years after the first wave of Covid-19 changed the tech landscape in a question of weeks, it’s safe to say the pandemic has served as a catalyst for the digital transformation of many aspects of consumer behaviour in Europe.

Image Source: McKinsey & Company

Image Source: McKinsey & Company

According to data from the European Parliament, the EU experienced a significant digital adoption increase during the first wave of the Covid-19 pandemic, as it went from 81% to 95%. The digital sector faced negative impacts during the first wave of the pandemic, with the disruption of supply chains slowing down production in several countries.

The manufacturing sector experienced a fall in demand for hardware due to decreased demand caused by industry shutdowns, and as a result, there was lower demand for digital manufacturing and service products. Despite these setbacks, there was a significant increase in demand for digital infrastructure due to the need for telework. During 2020, the number of people employed in the industry increased by 0.9% compared to the previous year, and the value-added increased by 1.8%.

The Covid-19 pandemic has had a negative impact on innovation performance indicators such as innovation expenditures, innovative sales, and venture capital expenditures, with all showing a decline in 2020.

Additionally, GDP fell in 2020 compared to 2019 for 22 Member States, which also negatively affected indicators that include GDP in the denominator. Although Covid-19 negatively impacted exports, exports of medium- and high-tech products and knowledge-intensive services were less affected than total exports, resulting in an overall positive effect on their export shares. However, it is still uncertain how much of an impact the pandemic will have on innovation in the long run.

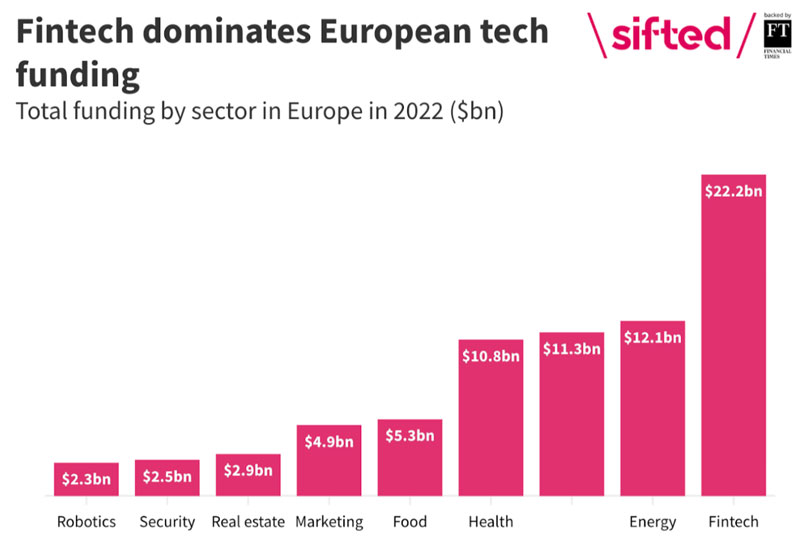

The Atomico State of European tech 2022 report describes Europe’s startup scene as resilient. The years have characterized the market with a slower pace and the shift towards prioritizing growth efficiency, moving away from a grow-at-all-costs mindset.

As the economic downturn causes uncertainty in global markets, venture capital investors are becoming more cautious and selective. They are looking for companies with growth potential and balance efficiency, sustainability, and profitability. European’s Fintech and Energy sector led the scene in growth and funding, according to Dealroom.

Image Source: Sifted

Image Source: Sifted

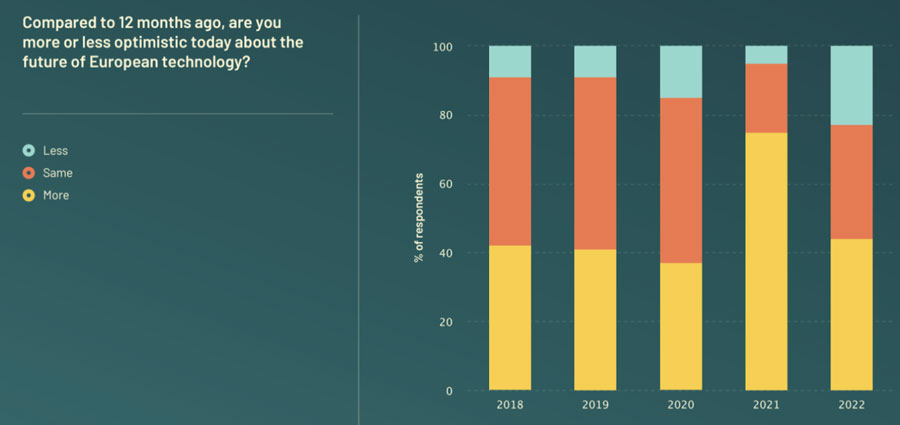

Founder sentiment towards the fundraising environment has drastically changed over the course of 2022, with 82% of respondents in the Atomico survey stating that raising venture capital has become more challenging. This shift in sentiment is the largest change recorded in the past five years of surveying the ecosystem, indicating the reality of the new market environment.

Despite the challenges, internal and external, to the startup scene, the general feeling is optimistic. According to the Atomico survey, 77% of all respondents remain optimistic or have become more optimistic about the future compared to 12 months ago.

Surprisingly, only 23% of respondents reported decreased optimism compared to last year, possibly due to their ability to distinguish between short-to-mid-term financial downturn impacts and the long-term prospects of the European tech industry. This industry’s future ultimately depends on the strength of the entrepreneurial ecosystem and the driving force of technological innovation.

Image Source: Atomico

Image Source: Atomico

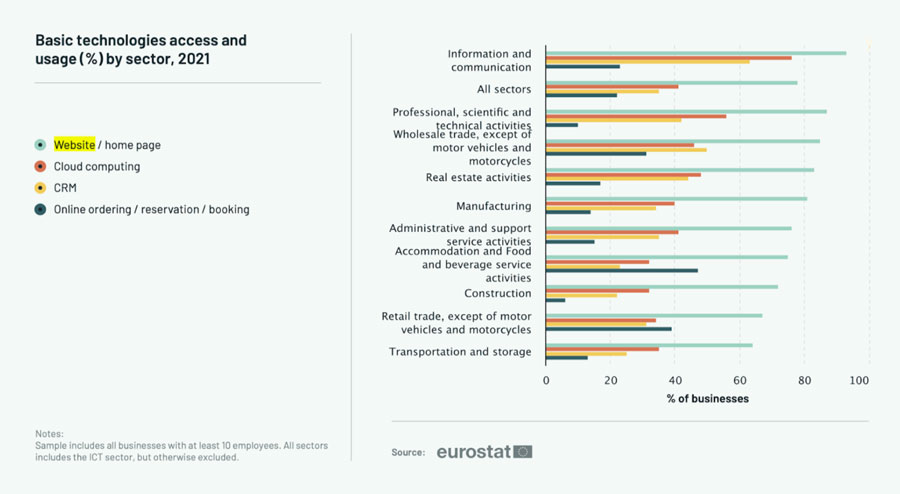

Although there has been a decrease in investment activity, investors continue to search for prospects in the European tech industry. The pandemic has expedited the adoption of technology, but there is still considerable potential for growth in Europe.

As an illustration of this, many European businesses still do not have a website, or if they do, they are not leveraging cloud technology to expand their operations. According to Atomico statistics, one-third of retail companies in Europe lack a website, and nearly 60% of businesses with at least 10 employees are not utilizing cloud services.

Image Source: Atomico

Image Source: Atomico

Companies are shifting their focus from solely growing quickly to reducing costs and achieving profitability. The market is demonstrating its ability to adapt to challenges and is better equipped than ever to navigate uncertainty. Private mergers and acquisitions have seen a rise, and this trend is projected to persist.

The tech industry has emerged from the pandemic stronger and more efficiently, thanks to the rapid adoption of digital technologies. However, the effects of the pandemic were strong: from hiring freezes to layoffs to adapting business models. According to data from European Startups, as the surge of investment experienced during 2021 wears off, it becomes decisive for the future of the tech landscape in Europe to foster great collaboration between the public and private sectors.

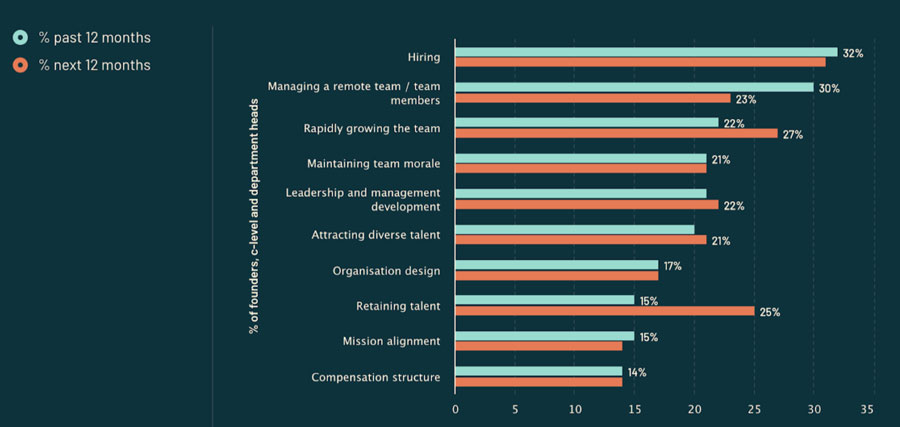

The retention and acquisition of talent remain top challenges for founders as they reflect on the past year and plan for the future. Interestingly, managing remote teams has become as challenging as hiring, if not more so.

As they look to the future, founders remain focused on growth, which includes rapid hiring and retention of current talent. This determination and forward-looking mindset is a promising indication of their expectations for 2023 as they actively seek out the right people to help them charge forward.

Image Source: State of European Tech 22

Image Source: State of European Tech 22

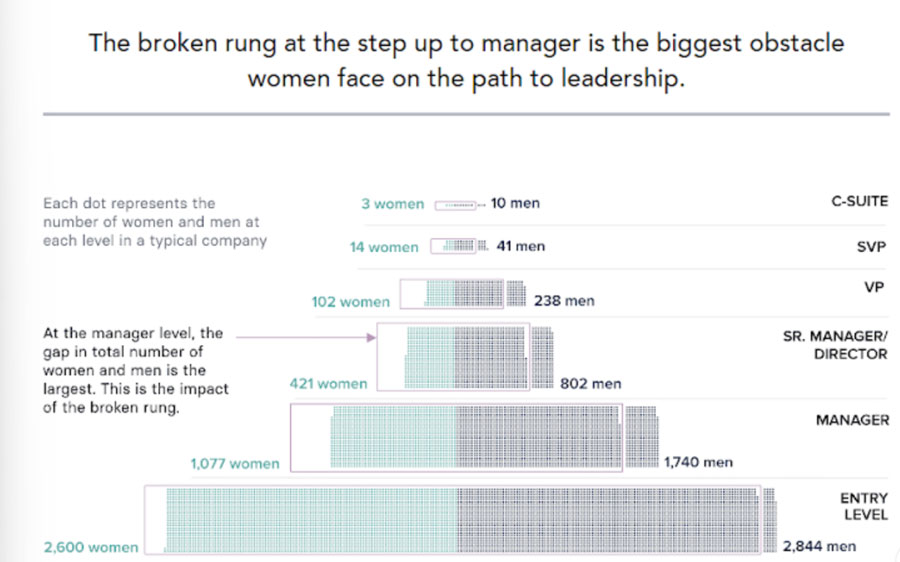

European startups also face a significant challenge: bettering their diversity. The data on VC funding for underrepresented groups in the European tech ecosystem is concerning. According to Atomico’s State of European Tech report, founding teams composed entirely of minority ethnic entrepreneurs receive a mere 0.7% of total funding into European unicorns, while only 1.4% of European unicorns are established by founders from that demographic.

Additionally, the report reveals that women-only founding teams received just 1% of VC funding in Europe in 2022, down from 3% in 2018. Funds with women-only general partners raised only 1% of capital, and women represent only 15% of general partners in Europe.

The European tech industry is facing significant challenges when it comes to gender diversity. Despite the efforts of many organizations to promote gender equality in the workplace, women continue to be underrepresented in the tech sector. The lack of diversity in the industry not only limits opportunities for women but also leads to a lack of diverse perspectives and creativity, hindering innovation.

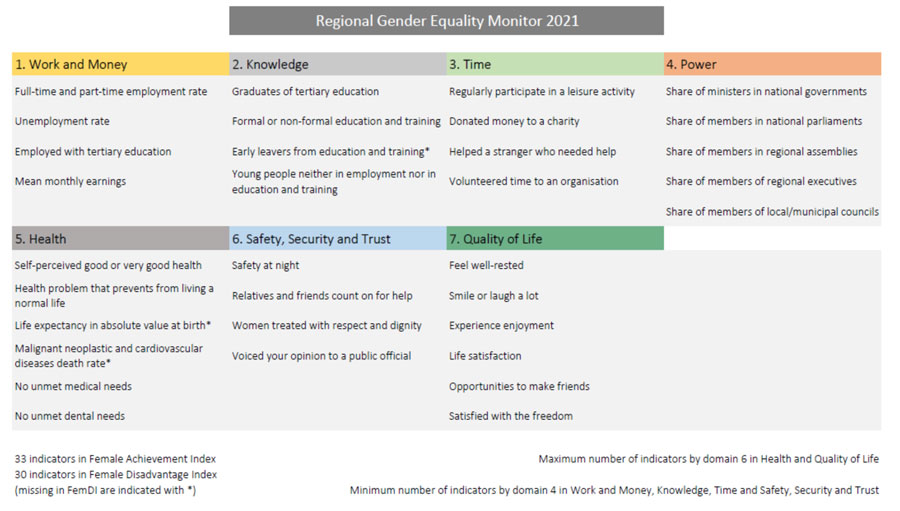

The Regional Gender Equality Monitor, created by the European Commission, utilizes two indices – the Female Achievement Index (FemAI) and the Female Disadvantage Index (FemDI) – to assess gender equality across regions. These indices analyze 33 indicators across seven domains, including Work & Money, Knowledge, Time, Power, Health, Safety, Security & Trust, and Quality of Life.

Image Source: Cohesion Data

Image Source: Cohesion Data

Currently, the indices indicate the following trends, as pointed out by the key findings which are still being worked on:

- On average, women in more developed regions are able to achieve more and are at less of a disadvantage, while most women in less developed regions face big challenges.

- Within countries, women in capital regions tend to achieve more and are at less of a disadvantage.

- In general, regions with a lower female achievement index have a lower gross domestic product per capita, while regions with a higher level of female achievement have a higher level of human development.

- Finally, the quality of government is higher in regions where women achieve more.

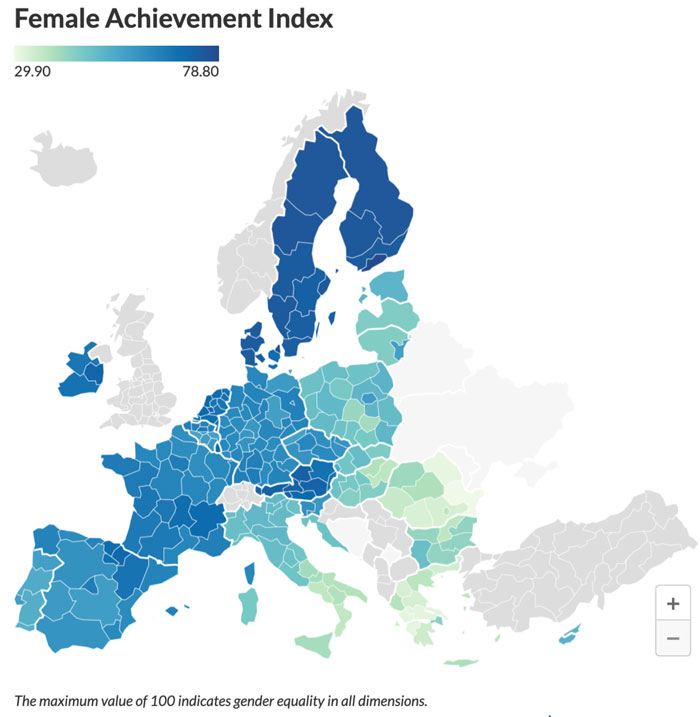

There are huge differences in gender equality between different European countries.

While some European countries have made significant strides in promoting gender equality, others continue to lag behind, according to The Gender Equality Monitor. For example, in countries such as Finland, Denmark and Sweden, gender equality is relatively strong, with women occupying a high percentage of leadership positions and having a smaller gender pay gap.

In other countries such as the Czech Republic, Slovakia, and Romania, gender equality is less well-developed, with women facing bigger barriers to entering the workforce and experimenting a bigger pay gap.

In countries with strong gender equality, women tend to have better access to education, healthcare, and other social services. This can lead to higher rates of economic growth, greater political stability, and a more equitable distribution of resources.

Image Source: Cohesion Data

Image Source: Cohesion Data

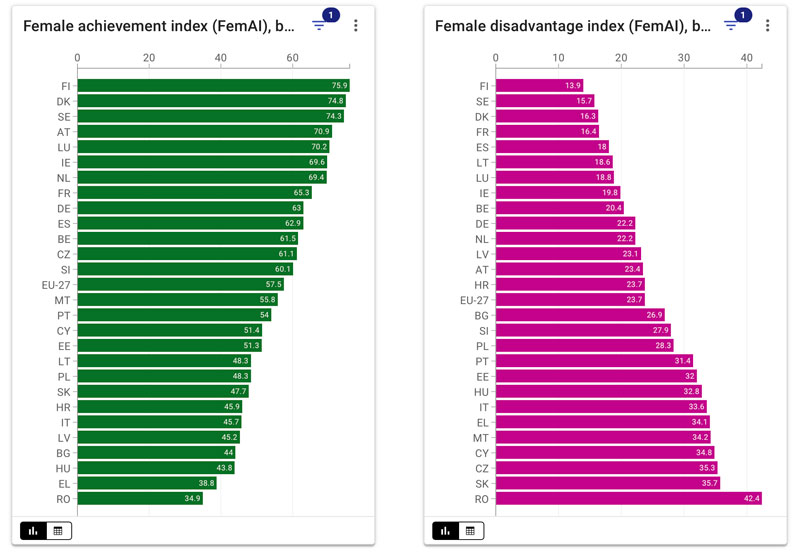

The countries ranking highest in the Female Achievement Index are Finland, Denmark, Sweden, Austria, and Luxembourg. These countries have made significant progress in all seven domains studied and demonstrate greater gender equality.

Image Source: Global Europe

Image Source: Global Europe

On the other hand, the top five countries in the Female Disadvantage Index, which reflects the extent of structural disadvantages faced by women, are Finland, Sweden, Denmark, France, and Spain. These countries offer women better opportunities for education, work, access to power positions, health, safety, and quality of life.

The 2021 Women in Digital Scoreboard by the Commission shows that there is still a gender gap in specialist digital skills, with only 19% of ICT specialists and one-third of STEM graduates being female.

The Digital Compass aims to reach convergence between women and men in having 20 million employed ICT specialists in the EU by 2030. However, there is a smaller gap for internet and internet user skills, with 85% of females using the internet regularly compared to 87% of males. Women in Finland, Sweden, Denmark, Estonia and the Netherlands are the most digital while Romania, Bulgaria, Poland, Hungary and Italy have the lowest female participation in the digital economy and society.

According to Web Summit, women continue to face discrimination in the workplace. The survey revealed that nearly two-thirds (67%) of women feel that they are paid less than their male colleagues in the last 12 months, a significant increase from 2019, when 46.4% felt they were paid fairly. Additionally, half of the women (49.5%) surveyed reported experiencing sexism in the workplace.

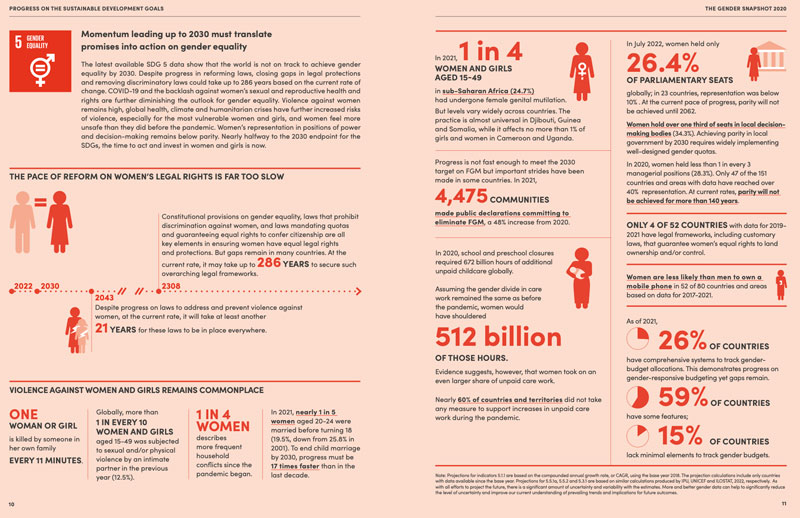

Gender Equality is a crucial objective in the UN’s Sustainable Development Agenda to achieve by 2030. However, despite the efforts, progress has been slow, and gender parity may not be achieved for another 286 years. The Gender Snapshot Report 2022 highlights the global status quo of gender equality and exposes the types of violence that continue to hold women back.

Image Source: UN Women

Image Source: UN Women

Image Source:

Image Source:

Image Source:

Image Source:  Image Source:

Image Source: