The Americas comprise 35 countries between North, Central and South America (or sometimes between North America and Latin America, including Central and South America), with around 1.02 billion people in total. Of the 8.02 billion people on the planet, that’s around 12,5% of the world’s population.

The Americas are characterised by much contrast and diversity in many ways, from Canada in the northern hemisphere to Costa Rica in the centre or Chile in the Southern hemisphere.

The main spoken language in The Americas is not English (with around 280 million speakers, mostly in the US and Canada), it is Spanish, with around 418 million speakers, followed by Portuguese (209 million, mostly in Brazil) and French (14 million, mostly in Canada).

That means Spanish is spoken in the continent by around 48% of the population as a first or second language (almost half of the population), around 36% speak English, 23% approximately speak Portuguese and French around 3%.

The continent has a big contrast between huge cities and metropolitan areas and very small countries and rural areas.

The Americas has some of the biggest metropolitan areas in the world, including São Paulo, Brazil. (22,430,000 people). Mexico City, México. (22,085,000 people). New York, US. (18,867,000 people). Los Angeles, US. (18,644,680 people) or Buenos Aires, Argentina. (15,370,000 people).

Whereas also has small countries like Puerto Rico, with a total of 3,256,028 people, Uruguay, with 3,426,260 people and Panamá, with 4,351,267 people.

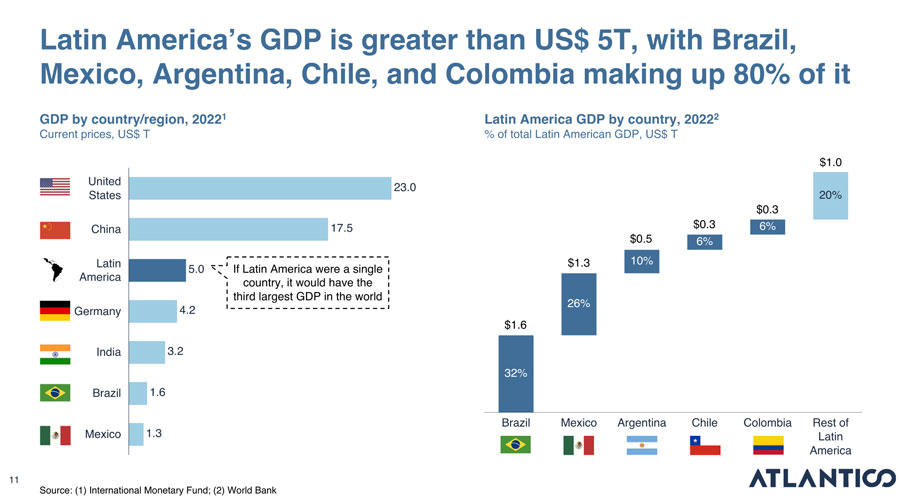

The Americas also have significant disparities in terms of development and wealth distribution. The United States is the wealthiest country in North America, accounting for most of the region’s GDP. In 2022, the US GDP was approximately 23.32 trillion USD, representing 85.4% of North America’s GDP.

In South America, Brazil is the largest economy and accounts for the majority of the south’s GDP, around 50.2% (with approximately 1.609 trillion USD in 2022).

Mexico, Argentina, Chile, and Colombia, account for more than 80%.

Image Source: Atlantico

Image Source: Atlantico

The significant differences in development levels among countries in the Americas created a major challenge when trying to make meaningful comparisons between them. While some countries in the region boast advanced economies and infrastructure, others are struggling with poverty and underdevelopment.

These disparities are particularly evident when it comes to issues such as gender equality, healthcare, education, and human rights. In order to address these challenges and work towards a more equitable and sustainable future for all, it is essential to take a nuanced approach that considers the unique circumstances and needs of each country and community.

The North American countries are now working together to forge a regional agenda and offer subnational governments the opportunity to collaborate and share best practices on open platforms.

The United States-Mexico-Canada Agreement (USMCA) is a free trade agreement between the United States, Mexico, and Canada, signed in 2018 and went into effect in 2020. The agreement replaces the North American Free Trade Agreement (NAFTA) and includes modernised provisions to reflect changes in trade and technology over the past 25 years.

The USMCA aims to create a level playing field for American workers, farmers, and businesses; encourage more investment; and provide stronger protections for intellectual property rights.

This agreement has laid the groundwork for digital integration across North America and established a clear basis for collaboration on open government data. By improving government services, North American countries believe that they can build public trust and strengthen their democracies individually and collectively.

The Digital Trade chapter discusses the following party agreements in more depth, but these points help us understand where the efforts are being made:

- Electronic Authentication and Electronic Signatures.

- Online Consumer Protection.

- Personal Information Protection.

- Paperless Trading.

- Cross-Border Transfer of Information by Electronic Means.

- Location of Computing Facilities.

- Unsolicited Commercial Electronic Communications.

- Cooperation.

- Cybersecurity.

- Source Code.

- Interactive Computer Services.

- Open Government Data are discussed in detail.

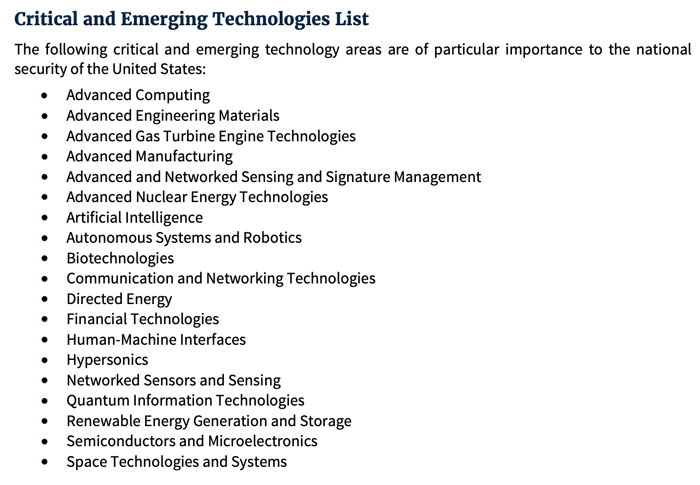

The US has updated its list of critical and emerging technologies (CETs) that can contribute to national security and innovation. The list includes subfields and is intended to guide efforts to promote US technological leadership, attract diverse science and technology talent, and protect against security threats.

The list has already influenced new policy guidance for National Interest Waivers. The 2021 CET list aligns with the three national security objectives outlined in the 2021 Interim National Security Strategic Guidance:

- Protect the security of the American people.

- Expand economic prosperity and opportunity.

- Realise and defend democratic values.

Here are the main technologies the US government thinks they have to promote in order to become a more technologically advanced country. This list gives us a hint of the tech trends for the US and, most surely, for the rest of the world.

Image Source: The White House

Image Source: The White House

To see the subfields in every tech sector exposed above and have a deeper understanding, go here.

The following paragraphs are mostly based on the ITU “Digital trends in the Americas region 2021” report, as it gives us a panoramic view of the state of digital tech in The Americas as a continent.

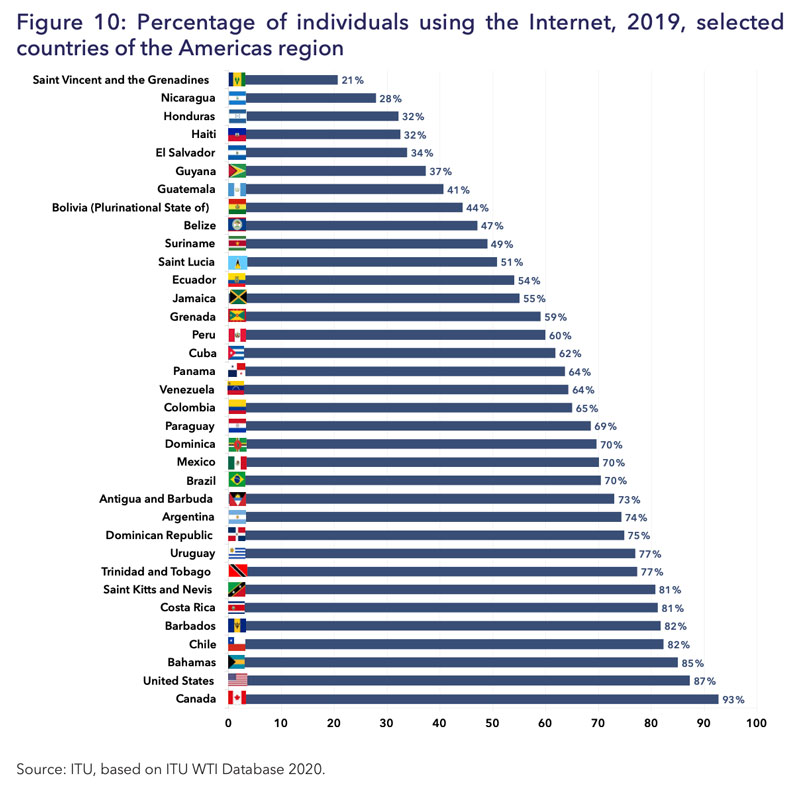

The COVID-19 pandemic has magnified the challenges faced by the Americas region regarding ICT (Information and Communications Technologies) infrastructure and usage.

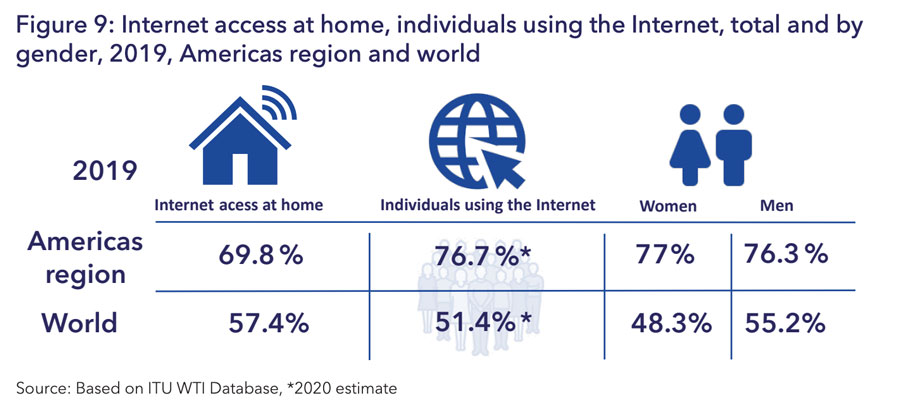

While there has been growth in most areas, lack of connectivity remains a significant barrier for many. While mobile network coverage is high, only 76.7% of individuals are using the Internet, and there is a significant rural-urban divide, with only 49.9% of rural households having access to the Internet in 2019.

Image Source: ITU

Image Source: ITU

Despite this, the ITU report shares that the region achieved internet access and usage gender parity in 2019, making the region the only one that achieved gender parity with a score of 1.01 per cent. When the value is less than one, it suggests that the usage of the Internet is more common among men than women, while a value greater than one suggests the opposite. Gender parity is indicated by values between 0.98 and 1.02.

The region is well above the world average for Internet access at home, with 69.8% of households having Internet access in 2019. Additionally, 76.7% of individuals in the Americas were using the Internet, which is also above the global average.

The Americas has achieved gender parity when it comes to Internet use. This means that nearly the same number of men and women use the Internet. Gender parity in Internet use is an important goal because it helps ensure that everyone has equal access to the opportunities and resources that the Internet provides, such as education, job opportunities, and social connections.

Image Source: ITU

Image Source: ITU

4G is the leading mobile technology in the Americas region, but around 285 million people were still not connected to the mobile internet by the end of 2019 due to high costs and lack of quality access. While infrastructure has improved, affordability remains low. The Americas region has a higher household internet access penetration rate than the global average, but access is unevenly spread across the region.

And there is significant room for improvement in basic, standard, and advanced ICT skills. Most countries have achieved basic ICT skills levels above 20% and above 10% for standard skills, but advanced skill levels were below 10% for most countries. This is how ITU understands the different ICT skills:

- Basic skills: Copying, moving files, copying and pasting, sending emails, transferring files.

- Standard skills: Using arithmetic formulas, connecting and installing devices, creating electronic presentations, finding, downloading, installing, and configuring software.

- Advanced skills: Writing computer programs using specialised programming languages.

Image Source: ITU

Image Source: ITU

Digital technologies offer great opportunities for Latin American and Caribbean (LAC) countries, but access to the internet and digital technologies is highly unequal across income groups and ethnicities.

The Covid-19 pandemic highlighted the risks of the slow adoption of digital technologies, but embracing digital transformation can help LAC countries overcome the socioeconomic impacts of the crisis and create more and better jobs.

Adequate governance, legal, and regulatory frameworks are needed to enable the potential of the digital revolution while also creating appropriate safeguards.

The digital transformation market in North America is expected to experience rapid growth, with a projected increase from $166.07 billion in 2017 to $757.63 billion by 2025, representing a CAGR of 22.1% from 2018 to 2025.

This growth is primarily driven by the increasing adoption of digital solutions by organisations to reach a larger audience through smart devices such as smartphones and tablets and the rising penetration of internet services.

The decreasing prices of internet and smart devices in emerging countries have also led to significant growth in the number of smartphone and internet users, thereby creating a huge potential for companies to reach large mass of audiences worldwide.

For instance, on-demand transportation companies like Uber and Lyft have successfully utilised digital platforms to reach a huge audience. Similarly, SMEs (Small and Medium-sized Enterprises) in the fastest-growing e-commerce market increasingly use online platforms to expand their market reach, enhance external communication, augment sales, and improve productivity.

Currently, the United States dominates the global digital transformation market, as the region is highly advanced in technology and economy and is one of the early adopters of new technology in any market.

Most of the industry verticals in the region have already adopted digital transformation solutions, and the number of companies in different verticals continues to increase.

Latin America has been making positive progress during the COVID-19 pandemic expanding connectivity and digital adoption. However, 45% of Latin Americans still do not have access to the internet, and investment in connectivity will be critical to bridging the digital divide and reducing inequalities.

To increase connectivity and technology adoption, governments and the private sector must face up to some inconvenient truths, including the need for significant investment in closing the digital divide and the need for smart and flexible regulations to support investment.

Latin America has made significant advances in digital transformation, but it still lags behind economies with more developed levels of digitalisation. The report indicates that the region is in an intermediate digital development stage, according to the Digital Ecosystem Development Index, significantly behind the average of OECD countries and other advanced regions.

The region has invested significantly in telecommunication, but there is still a need for improvement in cybersecurity and artificial intelligence capabilities.

The Covid-19 pandemic has led to a significant increase in cybercrime globally, including online scams, phishing, malware, and attacks exploiting vulnerabilities in systems.

The rise of cybercrime in the region has been financially motivated by groups targeting organisations with ransomware. In 2020, Latin America had the highest cyber-attack rates, with Costa Rica and Argentina being the victims of major ransomware attacks.

The cybersecurity market in Latin America was valued at nearly 12.9 billion U.S. dollars in 2019, indicating a growing need for security solutions. This market is expected to double by 2025, reflecting the increasing demand for cybersecurity measures.

Brazil, Mexico, and Colombia are the most targeted countries in Latin America, accounting for almost 90% of cyber-attacks recorded in the region. These countries have become prime targets for cybercriminals due to their large populations, growing economies, and increasing internet connectivity.

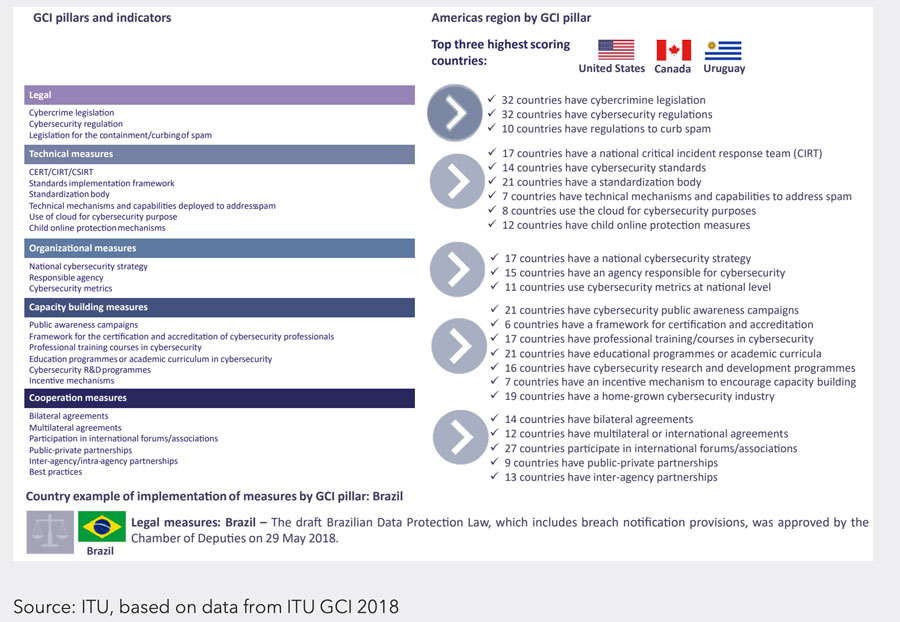

The Americas region has made progress in ensuring the safe and secure use of ICTs, but the commitment to cybersecurity is uneven across countries. Only three countries demonstrate high commitment, while eight have developed complex commitments and engage in cybersecurity programs and initiatives.

The United States, Canada, and Uruguay rank highest regarding cybersecurity measures. The Global Cybersecurity Index measures ITU Member States’ commitment across five cybersecurity pillars:

Image Source: ITU

Image Source: ITU

As the Covid-19 pandemic accelerated digital transformation, it also highlighted infrastructure gaps that pose a significant constraint to mitigating the impact on the economy and society.

The cybersecurity market in Latin America is growing rapidly, with an estimated compound annual growth rate of around 11.8% from 2022 to 2027. This is a significant increase, as the market was valued at 5.73 billion U.S. dollars in 2021 and is expected to exceed 10 billion U.S. dollars by 2027.

This growth is likely driven by the increasing number of cyber-attacks in the region and the growing awareness of the importance of cybersecurity for individuals, governments, and businesses.

As the adoption of technology and the use of the internet continues to grow in the region, the need for cybersecurity measures and solutions will also continue to increase, driving the growth of the cybersecurity market in Latin America.

The United States is one of the most targeted countries for cyber attacks, accounting for 46% of attacks globally between July 2020 and June 2021. The impact of cybercrime on US citizens is significant, with an estimated 53.35 million affected by cybercrime in the first half of 2022 and a total loss of $6.9 billion in 2021.

For businesses, ransomware attacks pose a serious threat, with 60% of US organisations having their data encrypted in successful ransomware attacks. While the cost to rectify these attacks decreased by 49% from 2020 to 2021, at an average cost of $1.08 million, just 50% of US organisations have full cyber insurance coverage.

A further 28% have cyber insurance with exclusions or exceptions, and 12% have no coverage at all, putting them at risk of financial ruin if they suffer an attack.

A recent study conducted by WFH Research revealed that almost 30% of all jobs in the United States remain remote, even as the country emerges from the COVID-19 pandemic. This is a significant increase from the 4% of jobs that were remote prior to the pandemic in 2019. Although the number of remote jobs has decreased from its peak of 61% during the pandemic, the fact that a significant portion of jobs remains remote has had a profound impact on society.

The shift towards remote work has fundamentally altered the way people live and work, blurring the boundaries between work and personal life and prompting many to rethink their career and living choices.

It has also highlighted the importance of digital infrastructure, particularly high-speed internet and reliable technology, in enabling remote work. As the world continues to adapt to the new normal, the trend towards remote work is expected to continue, with long-lasting implications for the economy and society as a whole.

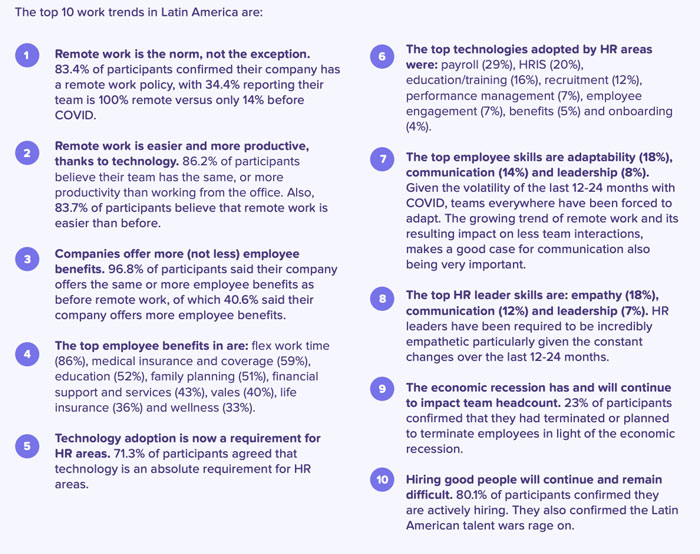

According to a survey made by Runa, remote work has grown fast in Latin America and is expected to stay, with 34,4% of participants reporting their teams are 100% remote versus 14% before Covid-19.

Image Source: Runa

Image Source: Runa

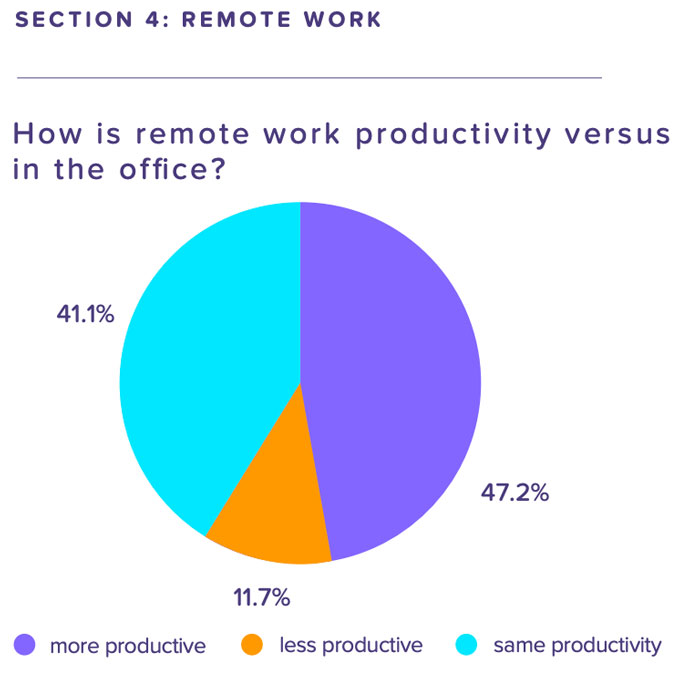

This statistic indicates that a significant portion of Latin American workers believe that remote working can actually lead to increased productivity. Nearly half of the respondents (47.2%) reported being more productive when working remotely, while 41.1% reported that their productivity levels remained the same.

These results suggest that, for many workers, the shift to remote working since Covid-19 has not only not impacted negatively their ability to get work done but has improved it. Only a small percentage of respondents (11.7%) reported being less productive while working remotely.

Image Source: Runa

Image Source: Runa

The phenomenon known as the «Great Resignation,» also referred to as the «Big Reshuffle» or the «Big Quit,» began in the United States as the COVID-19 pandemic disrupted the job market.

Essentially, it refers to a significant number of employees voluntarily leaving their jobs to seek out new opportunities, to upskill or reskill, to find a better work-life balance and to make desired changes in their lives. This job market movement has spread to other countries as well.

The impact of the pandemic on work-life balance, the shift to remote work, and the desire for more flexibility and autonomy have all contributed to this trend. In 2021, approximately 47 million Americans left their jobs, which was a significant increase from previous years. The trend continued in 2022, with even more people leaving their jobs, with around 50 million people quitting.

The reasons for quitting are diverse, with some seeking better pay or benefits, more fulfilling work, or a better work-life balance. Others have chosen to start their own businesses, pursue further education or training, or take a break from work altogether.

The Great Resignation has created significant challenges for employers who are struggling to retain employees and fill vacant positions. Some industries have been hit particularly hard, such as hospitality, service-work industries and healthcare.

As the Great Resignation continues, it is likely to have far-reaching implications for the job market, the economy, and society as a whole. Employers will need to adapt to the changing needs and expectations of their employees, giving higher pay and improving conditions, and individuals will continue to explore new opportunities and seek out more meaningful and fulfilling work.

Image Source: Statista

Image Source: Statista

While the Great Resignation phenomenon may have hit the United States the hardest, the effects of the pandemic and the changing job market have been felt worldwide. Even in countries where there hasn’t been a surge in resignations, employees are still looking for better opportunities, and employers are being forced to adapt to changing expectations.

The pandemic has brought about a global shift in how people think about work, with many employees now placing a higher value on work-life balance, flexible working arrangements, and job satisfaction. Employers have had to respond by creating more appealing job opportunities that meet these expectations.

Prioritising employee well-being and mental health, as well as addressing systemic inequalities in the workplace, has become increasingly crucial for employers. Those who fail to take action risk losing valuable talent to competitors who offer a more inclusive and supportive work environment.

The effects of the pandemic on the job market have prompted a necessary debate around the future of work, as employers and employees worldwide are re-evaluating their priorities and expectations.

The “PwC’s Global Workforce Hopes and Fears Survey 2022” was held in 44 countries to more than 52.000 employees and has shown that workers with specialised or scarce skills are more empowered, and 29% of respondents said their countries lacked people with the skills necessary to perform their jobs. While companies invest in their current workforce through upskilling and increasing wages, only 40% of employees said their company is upskilling, and only 26% said their employer is automating or enhancing work through technology.

The PWS’s survey reveals that employees are more concerned about not receiving sufficient training in digital and technology skills from their employers than being replaced by technology.

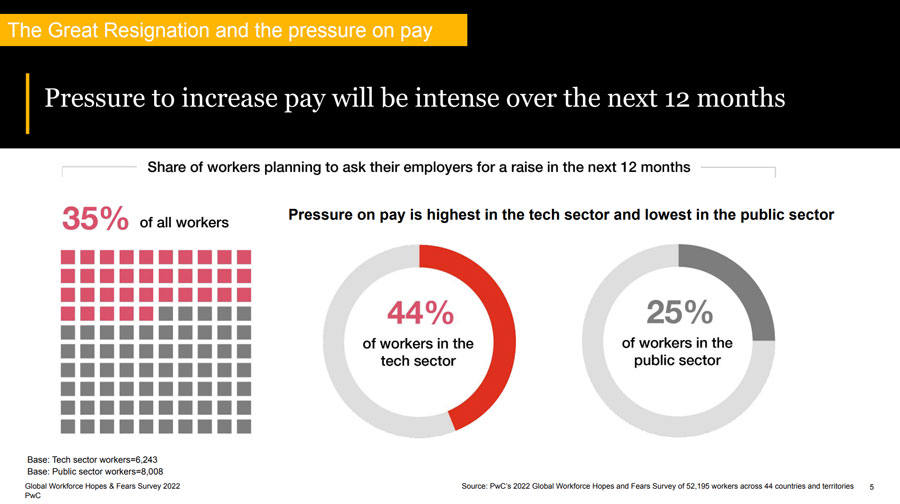

When it comes to retaining employees, pay is a crucial factor that cannot be ignored. A competitive salary not only helps to attract top talent but also plays a pivotal role in keeping existing employees satisfied and engaged.

In the tech sector, which is known for its rapid growth and high competition, compensation packages are a key tool in the war for talent.

According to PWC’s survey, as many as 44% of the workforce in the tech sector have indicated that they plan to ask for a raise in the next 12 months, signalling the growing importance of compensation in this industry.

Image Source: PWC

Image Source: PWC

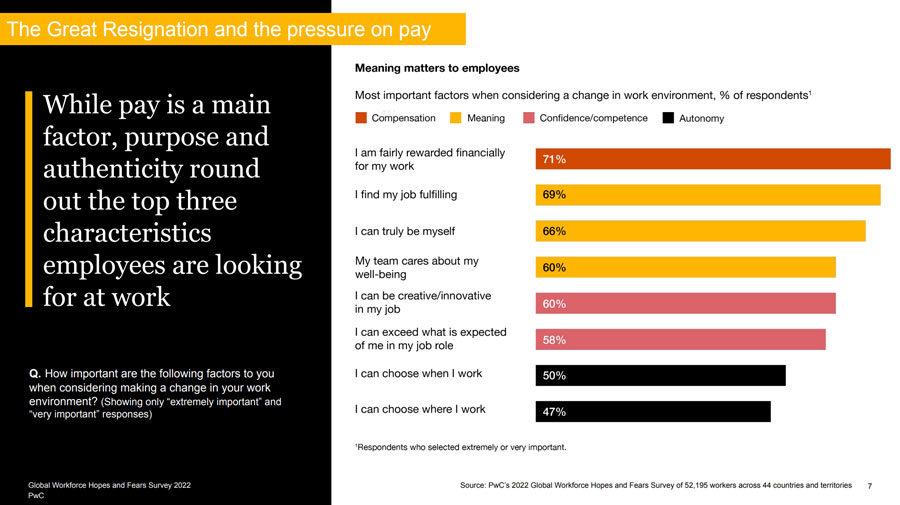

While pay and benefits are important, they are not the only factors that impact employee retention and job satisfaction. Employees also want to feel fulfilled and valued in their work and that they are able to bring their authentic selves to the workplace. Creating a flexible work environment where employees can be creative and choose when or where they work can be just as a determining factor to stay at the current job as offering competitive pay.

Image Source: PWC

Image Source: PWC

Companies must consider the needs and satisfaction of in-person employees as they adjust their workforce strategies for hybrid work. According to the survey, 45% of employees who cannot work remotely report lower job satisfaction than those in hybrid or fully remote work settings.

Additionally, companies should recognize the important role these in-person employees play in society and their responsibility to them. A majority of employees prefer a mix of in-person and remote work, and younger employees are more likely to work remotely.

The North American venture capital deal values saw positive growth in 2020, reaching USD 182 billion by 2021’s end, up 29% from 2020, with an annual average growth rate of 14% since 2016.

Although the number of transactions declined, the pandemic-friendly sectors such as biotechnology, software companies, self-driving cars, secure payment processing, and online gaming received significant shares of capital.

Funding for startups and growth-stage private companies in North America held up at historically high levels in 2021.

Venture capital investment in Canada remained strong in 2021, with a focus on B2B solutions, fintech, and Edtech. Meanwhile, U.S. fintech funding surpassed 2020 levels, with investment and capital markets companies receiving the most funding, and insurtech and payments also popular targets.

The startup and scaleup ecosystem in The Americas is characterized by a wide range of players with diverse profiles, resulting in significant differences between North America and Latin America.

Funding for U.S. startups fell by one-third from their peak in 2021, with private venture-backed companies raising a total of $238.3 billion in 2022, 31% lower than the record of $344.7 billion in 2021.

Despite this, 2022 saw $162.6 billion closed across 769 funds, setting an annual record for capital raised and marking venture capital’s rise as an asset class for money managers.

The public market performance continues to weigh on private market investor sentiment, and initial public offerings remain scarce, limiting exit options for VC investors. Growth and late-stage firms now need to choose a «down round» or take structured financing with debt-like features.

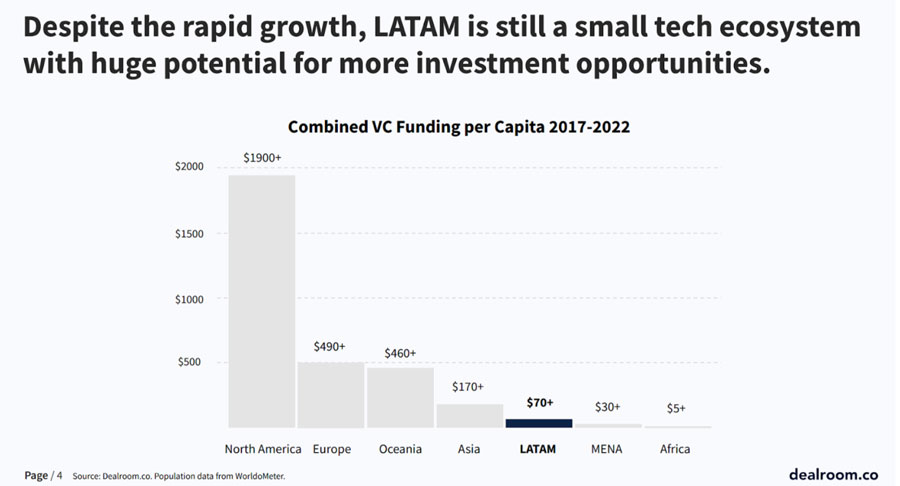

Over the past five years, the investment landscape in North America has seen a massive surge, with the investment amount tripling from 5.3 trillion dollars in 2017 to 17.6 trillion dollars in 2022.

In contrast, Latin America has witnessed an impressive increase in investment by 6.9 times, rising from 59 billion dollars in 2017 to 408 billion dollars in 2022. Despite these differences, both regions offer excellent opportunities for investors, entrepreneurs, and startups to tap into their markets and build thriving businesses, and a lot of room for LATAM to grow.

Image Source: Dealroom

Image Source: Dealroom

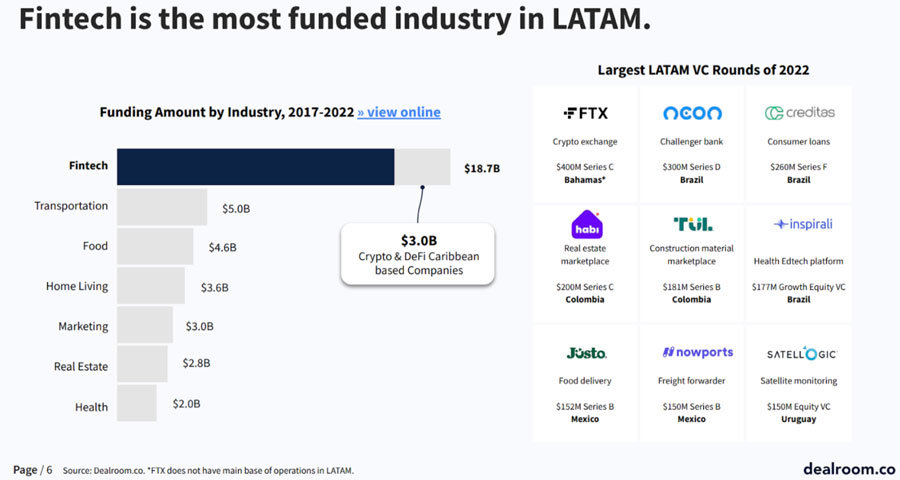

In Latin America, the fintech industry has emerged as a major focus for investment, with a significant portion of capital being allocated to this sector. In fact, investments in LATAM’s fintech industry have amounted to approximately 17.8 billion dollars, making it one of the most significant areas of growth in the region.

A growing number of investors have turned their attention to cryptocurrency and decentralized finance (DeFi) companies within the fintech space, allocating approximately 3 billion dollars of the total investment to these emerging areas.

Image Source: Dealroom

A study by the Inter-American Development Bank (IDB) reveals that women’s participation in digital transformation in Latin America and the Caribbean is limited by a lack of digital skills and competencies, with access to financing being one of the main barriers for female entrepreneurs in digital fields.

The study recommends specific public policies to reduce the gender gap in digital business transformations and highlights the need to change the culture through awareness campaigns and equitable early education in STEM, foster a culture of self-empowerment and ongoing training in digital technologies, and legal reforms to distribute family responsibilities more evenly among capable adults.

The IDB study also recommends companies develop gender equality policies, consider implementing flexible or hybrid work mechanisms, create mentoring programs, and adopt upskilling and reskilling measures for women in digital fields.

Women investors and founders in early-stage tech are underrepresented in Latin America, as they are global. Latin America’s lack of diverse representation among decision-makers has ramifications for entrepreneurs, as startups with global women co-founders captured only about 12% of VC funding in 2019.

To recover from the pandemic and build stronger, more inclusive economies, Latin America should focus on increasing women’s labour participation.

It’s predicted that Latin America could increase GDP by 14% over the next five years by better-incorporating women into the workforce. Some measures are already underway, such as the Women Empowerment Principles and Gender Impact Investment. However, challenges remain, including limited credit history and the gender wage gap. While the number of tech companies with women in executive positions is increasing, more needs to be done to advance women’s inclusion.

The Gender Equality Observatory for Latin America and the Caribbean shares different indicators of gender equality for the region.

Let’s look at some of these indicators:

1. People without incomes of their own

This indicator is the ratio of the total female/male population aged 15 and above with no incomes of their own and who are not studying, compared to the total female or male population aged 15 and above who do not study exclusively. This ratio is expressed in percentages and is further broken down by age and area of residence.

The analysis of this indicator reveals that women’s economic autonomy is still limited in many countries in the region. While the participation of women in the labour force has increased over the years, in 2019, almost one-third of women in the region did not have their own income and were dependent on others, usually men.

This lack of economic autonomy means that women have limited decision-making power in household money administration issues and are more vulnerable to economic shocks and dependent on others for their basic needs.

This highlights the need for policies and programs that promote women’s economic empowerment, such as improving access to education and training, increasing women’s participation in the labour market, promoting entrepreneurship and financial inclusion, and addressing gender-based discrimination and stereotypes.

By increasing women’s economic autonomy, not only can their own well-being be improved, but also that of their families and communities, contributing to more inclusive and sustainable development in the region.

Image Source: United Nations

Image Source: United Nations

The child marriage indicator measures the proportion of women aged 20-24 who were married or in a stable union before turning 18. Child marriage is considered a violation of human rights and puts children, particularly girls, at risk of harm and limits their development.

This harmful practice is associated with negative outcomes such as early childbearing, lower participation in the labour force as adults, lower education levels achieved, and a greater risk of experiencing gender-based violence.

The child marriage indicator is part of Sustainable Development Goal (SDG) 5, which aims to achieve gender equality and empower all women and girls by eliminating harmful practices such as child, early, and forced marriage and female genital mutilation.

The analysis of the indicator reveals that in the region, one in five women is affected by child marriage, with the highest prevalence in Suriname, Nicaragua, Honduras, Belize, the Dominican Republic, and Guyana. However, there are some countries with lower percentages of child marriage, such as Costa Rica, Argentina, Peru, and Jamaica.

Image Source: United Nations

Image Source: United Nations

The indicator measures the percentage of young women aged 15 to 19 who have given birth to at least one child at the time of the census. This indicator is used to assess the prevalence of teenage pregnancy, which is considered a persistent problem in the region.

Although the overall fertility rate in the region is declining, the rate of teenage maternity remains high and is one of the highest in the world, with Latin American and Caribbean countries having a teenage maternity rate of over 12%.

This rate is mainly composed of adolescents with lower incomes and lower levels of education, indicating that the problem disproportionately affects disadvantaged groups.

Teenage pregnancy can have serious consequences for the health and well-being of young women, as well as for their social and economic opportunities, as they may face barriers to education, employment, and full participation in society.

Image Source: United Nations

Image Source: United Nations

4. Women’s deaths at the hands of their intimate partner or former partner

This indicator tells us the number and rate of women who are killed by their intimate partner or former partner. The data includes the absolute number and rate per 100,000 women aged 15 and over. This issue is a serious violation of women’s rights and a major public health concern in Latin America and the Caribbean.

The Dominican Republic, Uruguay, and Honduras are the countries with the highest rates of women’s deaths at the hands of their intimate partner or former partner, with rates equal to or greater than 1.0 per 100,000 women.

Guyana, Antigua and Barbuda, and Grenada have the highest rates of women’s deaths at the hands of their intimate partner or former partner in the Caribbean, while Jamaica has recorded the highest absolute number of victims. It is important to address this issue to ensure the safety and well-being of women in the region.

Image Source: United Nations

Image Source: United Nations

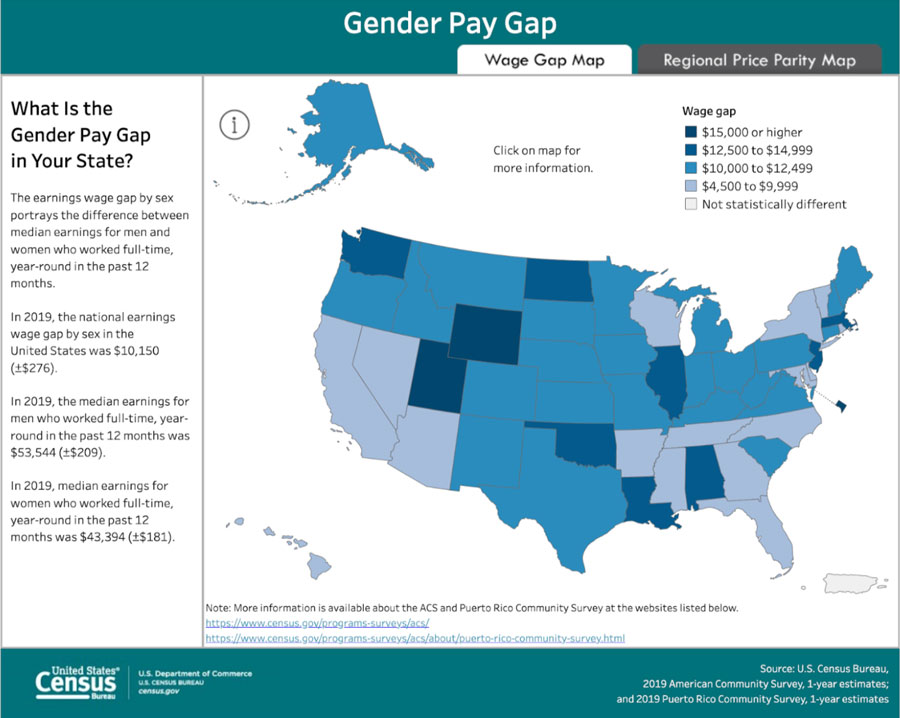

Women in the United States earn an average of 82% of what men earn, and the gender pay gap has remained relatively stable over the past 20 years. The wage gap is smaller for workers aged 25 to 34, where women earn 92 cents for every dollar earned by a man in the same age group.

Women are overrepresented in lower-paying jobs relative to their share of the workforce, but their increasing presence in higher-paying jobs traditionally dominated by men has contributed to narrowing the gap.

The reasons for the gender wage gap include women being treated differently by employers, women making different choices about how to balance work and family, and working in jobs that pay less. Working mothers are more likely to feel pressure to focus on responsibilities at home than working fathers.

Mothers are less likely to be in the labour force than women without children and, when employed, work fewer hours per week on average. Conversely, fathers are more likely to work longer hours and receive a “fatherhood wage premium,” which increases the gender pay gap. The pay gap also varies widely by race and ethnicity.

The gender pay gap has closed more among workers without a four-year college degree than among those who do have a bachelor’s degree or more education. Women have increased their share of employment in higher-paying occupations, such as managerial, business and finance, legal, and computer, science and engineering (STEM) occupations.

However, women are still underrepresented in managerial and STEM occupations. Looking across racial and ethnic groups, a wide gulf separates the earnings of Black and Hispanic women from the earnings of White men.

Image Source: US Census Bureau

Image Source: US Census Bureau

Image Source:

Image Source:  Image Source:

Image Source: