Developing a robust digital identity and industry in Germany has been a challenging process, replete with optimism and disappointment. Nevertheless, the nation currently finds itself at a pivotal juncture where general sentiments suggest a willingness to adopt a stronger digital identity. While the public sector may be prone to retracing previous missteps, the private industry is ready to move forward and adapt to a new European digital age.

The overall trend is that a new era for digital identity in Germany is imminent; solutions are being crafted by the public sector and through public/private collaborations, and consumer behaviour is shifting.

The German technology sector plays a crucial role in the digital age, making up 7% of Germany’s economic output, according to data from a Deloitte study, «Germany’s Technology Sector«. The sector drives innovation and enables new business models in other industries through its products and services.

In 2021, around one million people were employed in IT services and software in Germany, according to Statista. In the same year, the industry generated around 106 billion euros in revenue, and the software industry was responsible for 29.8 billion of that.

In 2022, the EU Digital Economy and Society Index, accountable for monitoring Europe’s digitalisation efforts, ranked Germany in the 13th spot out of the 27 members.

Image Source: Germany in the Digital Economy and Society Index

Image Source: Germany in the Digital Economy and Society Index

A spirit of innovation can also characterise German industry, and the country is internationally recognised as a leader in innovation. The Global Innovation Index, for example, ranks Germany as the 10th among the 51 high-income group economies and 7th among the 39 economies in Europe.

Despite having a strong economy and thriving industries, Germany needs to catch up in the digitalisation process compared to other EU countries. The country is facing some challenges in achieving the same level of technological development as its European peers, partly due to connectivity and digital infrastructure issues. Although the German tech sector continues to make significant contributions to the economy, the country still has work to do in order to fully realise its potential as a leader in the digital age.

Despite having a high internet penetration, at around 91%, high-speed connectivity is spotty and deficient. Germany is considered to have relatively slow internet speeds compared to some other developed countries, an issue that isn’t new. In 2017, Germany already struggled with slow internet, ranking in the 25th position in the ranking of countries with the fastest Internet access. This is partly due to a lack of investment in upgrading the country’s infrastructure and the challenges of providing internet access in rural areas.

Germany’s network infrastructure mainly relies on fibre optics, except for the final stretch connecting distribution boxes to homes. Telekom has a monopoly over these

boxes due to its use of vectoring technology, leading to a lack of motivation for innovation or improvement. Moreover, upgrading to fibre optics for the «last mile» can be a lengthy and costly process, particularly in rural areas.

While the expansion of fibre optics is progressing slowly, by the end of 2021 was at around 15%, and 89% of households had internet access of at least 100Mbit/s (5% more than in the same period in 2020).

In 2013 the then-German Chancellor was mocked for calling the internet «uncharted territory,» and seven years later, the COVID-19 pandemic highlighted persistent digital weaknesses in Germany’s public sector. The country had to deal with a pandemic and its devastating effects on top of schools with outdated computers or health centres relying on fax machines.

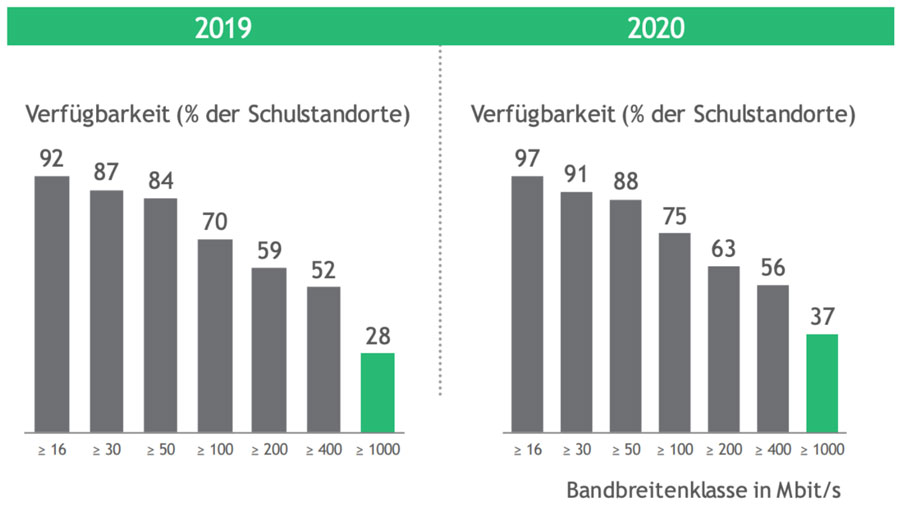

With the sudden shift to remote work and online learning, many people have come to rely heavily on the internet to maintain their daily routines. However, slow or unreliable internet can hinder productivity and make it difficult for individuals to complete essential tasks. In addition, low connectivity can also impact businesses, making it challenging for them to remain competitive and operate effectively in a digital age. The COVID-19 pandemic has highlighted the importance of digital infrastructure, highlighting the need for countries to invest in and improve their digital networks. For example, according to this study by Boston Consultancy Group, the coverage of schools with adequate broadband access was less than 40% at the time of the first Covid wave:

Germany is actively working to catch up in the tech sector. The government has set ambitious goals to improve the country’s digital infrastructure. By the end of 2025, half of all German households are expected to have access to fast fibre optic connections, and the goal is to eliminate mobile dead zones by the end of 2026. Other measures include digitising health records, digitalising administration to allow for online vehicle registration and ID applications, analysing mobility data to improve transportation infrastructure, and using technology to address the effects of the climate crisis.

Germany is actively working to catch up in the tech sector. The government has set ambitious goals to improve the country’s digital infrastructure. By the end of 2025, half of all German households are expected to have access to fast fibre optic connections, and the goal is to eliminate mobile dead zones by the end of 2026. Other measures include digitising health records, digitalising administration to allow for online vehicle registration and ID applications, analysing mobility data to improve transportation infrastructure, and using technology to address the effects of the climate crisis.

Although Germany has struggled with digitalisation in the public sector, its private sector is more digitally advanced, particularly in terms of startups. The startup scene in Germany is thriving, with numerous successful companies emerging in recent years, including around 25 unicorns (companies valued at over 1Bn). The country has a robust ecosystem for startups, with supportive government policies, a large pool of talented individuals, and access to capital.

Germany has a diverse and decentralised startup landscape, making it unique compared to other countries. This is reflected in the diversity of regional startup ecosystems across the country, which showcase Germany’s decentralised economic structure. The following image illustrates how diverse the startup scene looked at the end of 2021, shown in the Deutscher Startup Monitor 2021:

Image Source: Deutscher Startup Monitor 2021

Image Source: Deutscher Startup Monitor 2021

The presence of a wide range of start-up ecosystems provides opportunities for entrepreneurs and innovators to find the right environment to develop and grow their businesses, regardless of location.

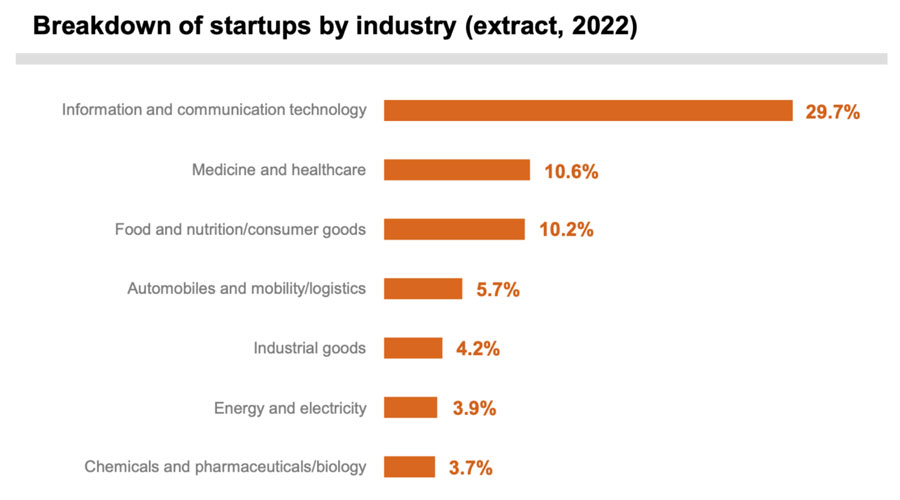

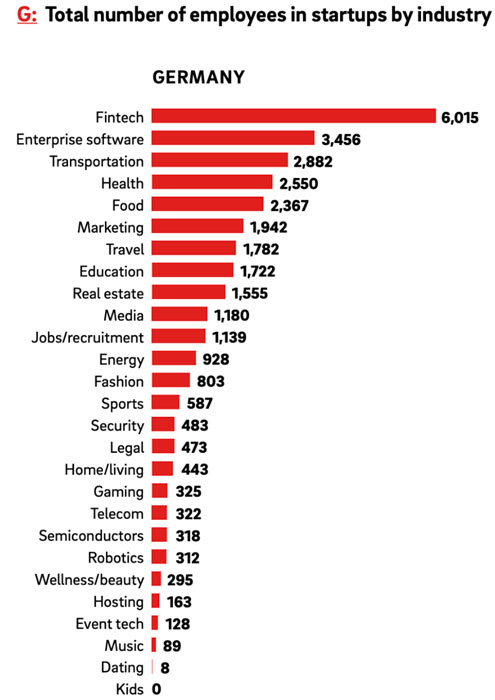

Startups play a vital role in driving innovation across all sectors of the economy. The primary industry is still information and communication technology, accounting for 30% of all startups. The medical and healthcare, as well as the nutrition and food/consumer goods sectors, are among the top 3, according to the German Startup Monitor 2022.

Image Source: German Startup Monitor 2022

Image Source: German Startup Monitor 2022

According to Startup Genome, 10% of all new startups established since 2018 are Fintech companies. The favourable environment for Fintech startups is primarily due to a well-considered regulatory approach that simplifies compliance. Berlin is also a hub for developing AI solutions in the healthcare sector. The annual revenue generated by AI companies in the city is predicted to exceed €2 billion by 2025.

Additionally, in March 2021, appliedAI created the «German AI Startup Landscape«, a central database of AI startups, businesses, and SMEs.

According to Startup Verband, the German startup scene employs over 415,000 people, and in the German Startup Monitor 2022, they claim the sector continues to plan new hires. In this report, Fintech and software employ the most significant number of people:

Image Source: Gender Diversity in German and French Startups

Image Source: Gender Diversity in German and French Startups

The same report states that Germany’s startup scene is known for its diversity, with over a quarter of startup employees coming from international backgrounds. This diversity is particularly pronounced in cities such as Berlin and Munich, where the representation of international employees reaches 41% and 36%, respectively.

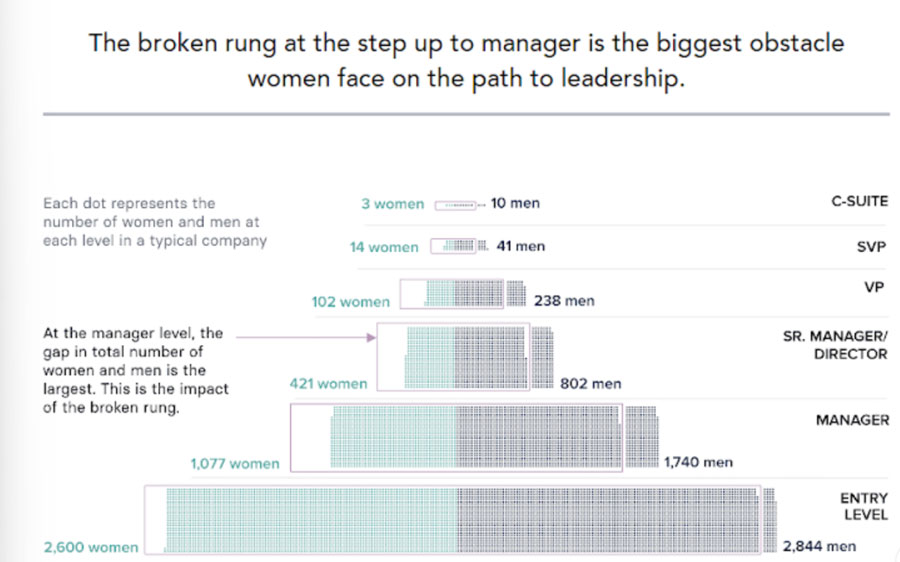

Despite this, there is still room for improvement regarding gender diversity within the tech ecosystem. Although women make up 47% of the general workforce in Germany, the representation of women among employees of startups is lower, at only 37%. This highlights the need for continued efforts to promote diversity and inclusiveness in the German startup scene. Diversity in startups is not just a question of gender parity but also greater human representation and economic growth.

In the MacKinsey Entrepreneurship zeitgeist 2030 report, a study that examines how the German startup scene could improve, data suggests that supporting migrant talent pools could reinforce the startup scene considerably. Currently, 59% of migrants or their descendants express a higher interest in starting a business compared to 49% of non-migrants; however, they only make up 20% of current business founders. With systematic support, this growing talent pool could result in an additional 180 start-ups being established in Germany annually by 2030.

According to Startup Genome, Berlin is one of Europe’s thriving startup scenes, with €10.5 billion invested in 2021, accounting for 60% of the total capital invested in Germany. In their annual rankings, they place Berlin as one of the top five startups ecosystems and in high positions in performance and funding:

Image Source: Startupgenome

Image Source: Startupgenome

The government has pledged €10 billion to support startups in their growth phase, distributed via an investment fund (Zukunftsfonds, or “Future Fund”). This is not the only step the Federal Government has taken in order to solidify its startup scene. In the country’s first comprehensive policy roadmap for startups, with a 10-point plan that aims to enhance financial support for startups, overhaul the tax system for employee stock options, streamline spinouts at universities, and promote diversity.

This Startup Strategy includes some critical action plans:

- Funding: faster and easier access to grants and financing for citizens and companies through a centralised digital funding portal that will allow interested parties to search, apply and process funding in a user-friendly manner. The government will work with private investors to mobilise more private and public capital for Germany as a venture capital location.

- Strengthen the ecosystem: make it easier for start-ups to attract talent, promote diversity and help remove obstacles for women and people with a migration background in accessing financing and subsidies and offer better access to venture capital. Facilitate access to public data sets and facilitate start-up spin-offs from science.

- Focus on quality: prioritise social impact over maximising profit. Provide social impact startups with better access to funding through special financing instruments, such as European structural funds. This will support the growth and expansion of socially focused startups, enabling them to make a more significant positive impact.

- Nourish the sector: Mobilize start-up skills for public contracts, and enhance the connections between all important players in the startup ecosystem. To achieve this, the government will hold the first «Start-up Summit Germany» in collaboration with key stakeholders. A network of startup contact points will also be established in all federal ministries and affiliated organisations.

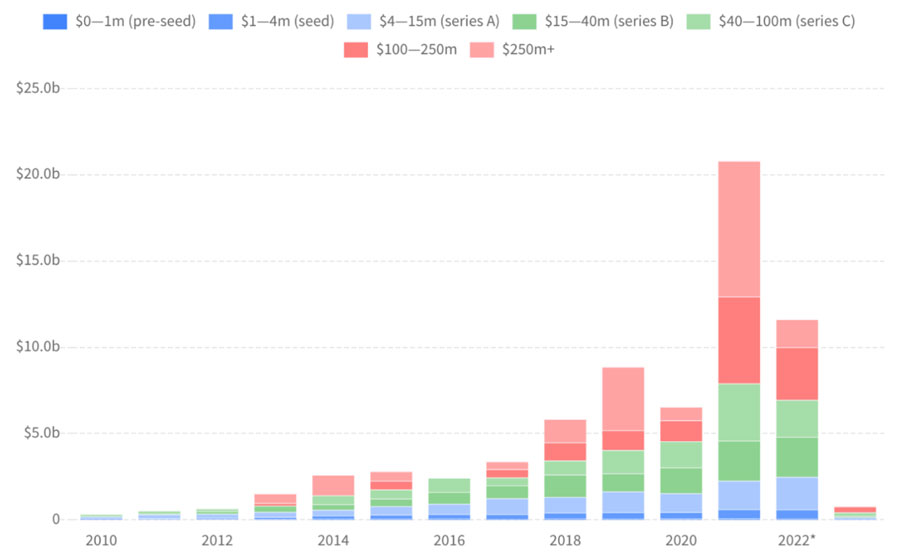

However, startups in Germany rely on more than just public funding but also on venture capital (VC) investments, for which 2021 was a record year, reaching $20.4bn.

This level of growth was significant compared to the previous two years: in 2019 and 2020, investment volume amounted to 6.2€ billion and 5.3€ billion, respectively. The country ranked second in Europe for startup investment volume, behind only the United Kingdom. Despite having a record year in terms of funding during 2021, 2022 was characterised by a more conservative approach, only reaching $11.4bn.

Image Source: Funding Rounds | Dealroom

Image Source: Funding Rounds | Dealroom

Germany, just like Europe, has been impacted by layoffs in tech companies. Some well-known European startups have had to significantly reduce their workforce to control expenses and maintain their cash flow during the global economic slowdown. As a result, VCs are becoming more cautious in their investments.

According to Morphais, the total value of investments in German startups fell by -46%. Despite this, VC investment decreased in the latter half of the year, but there is still a large amount of capital available in the market. This is due to a continuous increase in the number of new VC funds and their total fund volume in recent years. The data shows that fund volumes have continued to increase since 2020.

Despite some challenges in the German startup ecosystem, such as downsizing and layoffs, the overall sentiment remains positive. The entrepreneurial spirit is alive and well in Germany, and many startups are rising to the challenge of a more competitive landscape. The German startup community’s diversity and strength give hope and optimism for the future, and investors and stakeholders remain confident in the potential for success and growth.

The German tech industry has undergone significant changes in recent years, driven by the acceleration of digitalisation and the impact of the Covid-19 pandemic on social and political factors. According to this German Market Analysis, the IT industry is expected to reach a value of US$133.02 billion by 2026.

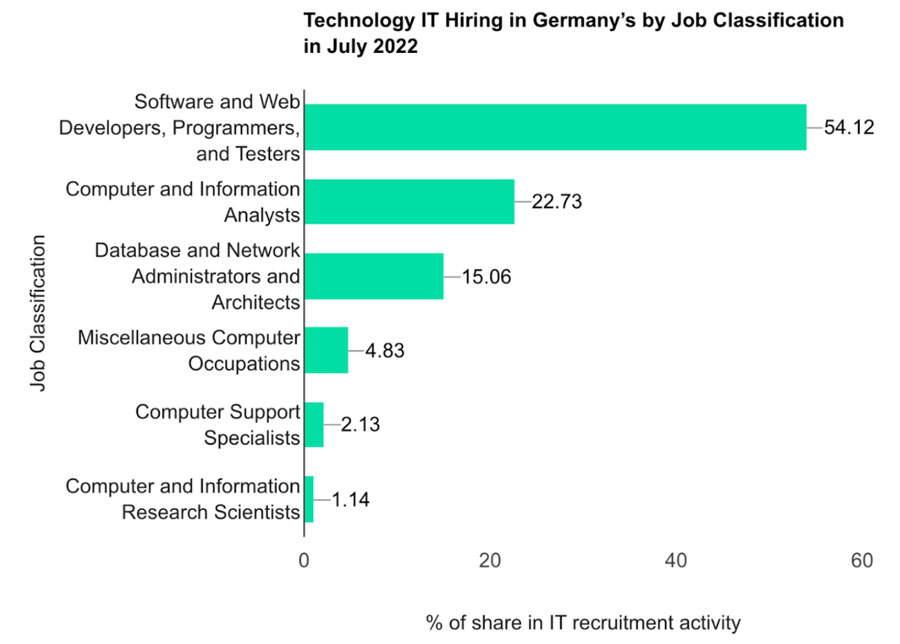

As the tech industry continues to expand, the demand for skilled professionals in the field also increases. The tech industry currently employs over 1 million workers, and 137,000 jobs are vacant in the IT industry, according to Make it in Germany, the Federal Government’s portal. Specialists are particularly in demand in the following areas: software development, application support (maintenance and support of software and hardware), IT security and data science.

Image Source: Germany’s technology industry IT recruitment activity drops 3.7% in July 2022

Image Source: Germany’s technology industry IT recruitment activity drops 3.7% in July 2022

As new technologies are developed and existing ones become more sophisticated, companies in the tech sector need talented individuals to help bring their visions to life.

Additionally, the demand for tech talent is not limited to tech companies; industries across the board are becoming more reliant on technology, further fueling the demand for tech talent in the job market. As a result, individuals with skills in the tech sector are in high demand, making it a lucrative career path with plenty of growth opportunities.

The talent shortage is already impacting the job market negatively. According to Gallup, 14% of German workers are actively looking for a new job, and it’s taking recruiters an average of 122 days to fill a vacancy with a qualified employee. This recent workplace study conducted by Gallup revealed that a significant portion of workers is considering quitting their jobs.

The study found that 39% of respondents stated that they would stop working entirely if they had the financial means to do so, which is a significant increase from the 25% recorded in 2016. This shift is a departure from Germany’s traditionally strong work ethic culture. At the same time, the study also showed that 40% of workers are actively searching for a new job, which represents the highest number of job seekers ever recorded in Germany. These results suggest that the German labour market is becoming increasingly volatile, approaching the level of job market fluctuation in the United States, which is known as the «Great Resignation.»

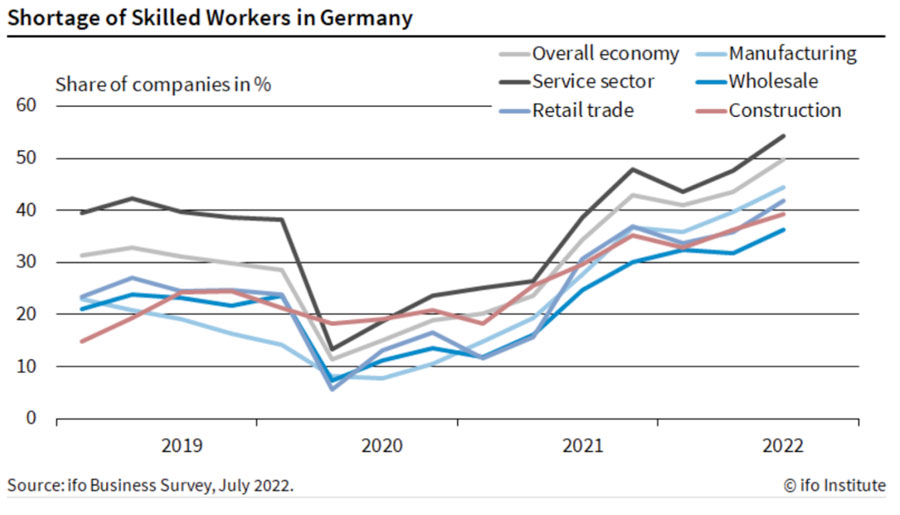

The labour shortage in the German job market is not only changing the tech landscape. As observed in the following image, data from the Ifo Institute shows how the talent shortage is affecting the overall economy and different industries:

The talent shortages have devastating effects on the country’s overall economy, and it could become dramatically worse as the deficit is projected to reach seven million by 2035.

The most impacted industries include IT, healthcare, education, and hospitality. To address this pressing issue and secure a bright future for the country’s economy, the German government has implemented various supportive measures, such as easing immigration laws to allow skilled workers from both within and outside the EU to join the workforce.

The Covid-19 pandemic has changed the world of work dramatically. The transition to remote work, the changes in social life and the opportunity to consider different options in a time of extraordinary stillness have transformed many people’s priorities. Perhaps now more than ever, we are experiencing a realignment in the workforce, where workers wish to connect to the companies they work for more meaningfully. They now also prioritise work-life balance, mental health and personal growth.

In Germany, the term Quereinsteiger, which loosely translates as “lateral entrant” is helping end the job-to-job jump stigma. As more people in Germany reevaluate their work priorities and what they expect from an employer, the number of people considering changing careers is increasing. This job-changing trend results in a significant concern for companies: retaining talent. The Gallup Engagement Index Deutschland data in 2021 shows that 69% of German employees are not engaged, and 14% are actively disengaged, leaving just 17% among the engaged.

This work-change trend often dubbed the «Great Reshuffle», presents a prime opportunity to both bring in and retain top talent, including existing employees. However, to take advantage of this opportunity, employers must provide the desirable workplace experience that workers seek.

This may prove to be a significant challenge, as such work environments typically have a strong focus on values, are flexible, and are led by leaders and skilled managers who prioritise the company’s mission, capitalise on employee abilities, and show genuine concern for their employees as individuals.

Shortages shape the tech landscape, and layoffs also impact the industry. The tech industry is undergoing a significant shift, as some tech markets, particularly the US, are laying off workers while others are in dire need of talent, and the German tech market is embracing newcomers.

The digital skills gap in Germany refers to the mismatch between the demand for digital skills in the German labour market and the supply of workers with these skills. This gap has been caused by the rapid adoption of technology in the workplace, leading to a need for workers with digital skills to keep up with new developments and meet the demands of employers. It directly impacts the number of workers with the necessary digital skills to fill jobs in the technology sector and many other industries that are becoming increasingly digitalised.

As the world gets increasingly technological, people lacking digital skills and digital literacy experience great difficulties participating in society.

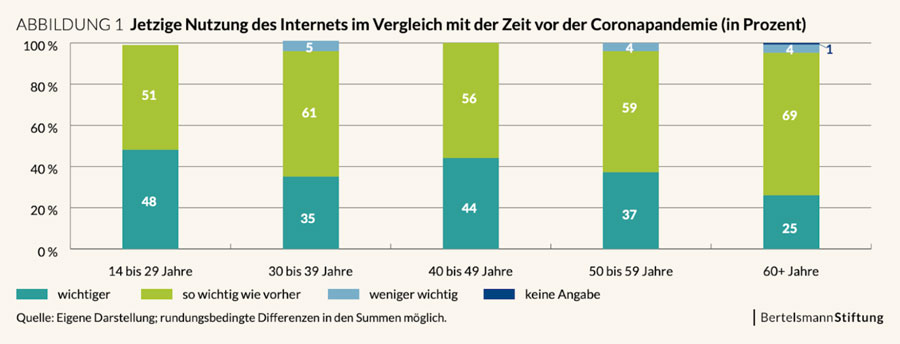

A study titled Digital Sovereignty 2021: Starting Off into a Digital Post-Covid World? examines how in the aftermath of the pandemic, people in Germany have a greater appreciation for digital technologies and their capacity for self-sufficiency compared to two years prior. The significance of Internet usage has increased for 4 out of 10 respondents after the Covid-19 pandemic, with younger people and women considering it more important compared to older people and men.

The importance of the Internet also increases with higher levels of education. Almost half of 14-29-year-olds say using the Internet has become more important due to the shift to online education. Older individuals could benefit from using digital technologies; however, the study shows that older people have less importance attached to Internet use compared to pre-pandemic and have a lower self-assessment of their digital skills. This image illustrates internet usage before and after the pandemic:

Image Source: Digital Divide in Society is widening.

Image Source: Digital Divide in Society is widening.

The study’s data show that different generations have varying views on the internet’s significance, leading to a divide between those who have the digital skills necessary to navigate the increasingly digital world and those who do not. The rapid shift towards digitalisation exacerbates existing differences in digital proficiency among citizens, which is what we call “a digital divide”.

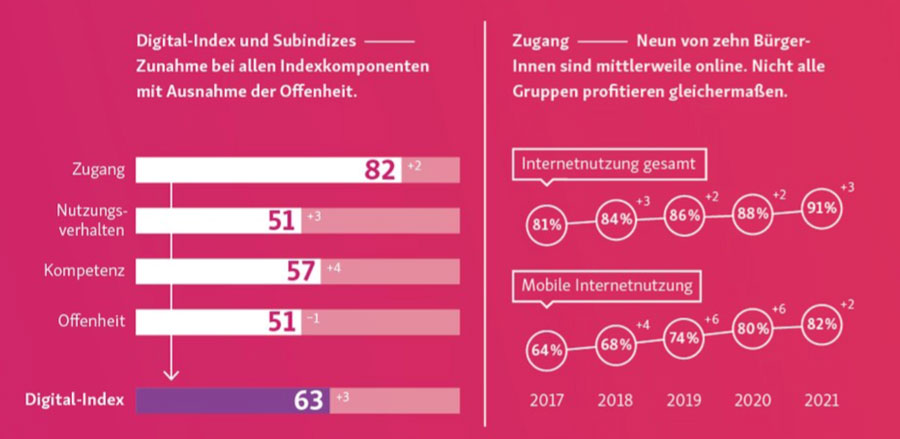

The D21 Digital Index 2021-2022 shows that the digital divide is slowly improving, as there are fewer digital marginalised than in their 2020 research. In fact, the study suggests that at the current rate of digitalisation, all German citizens could be using the internet in five years. Despite still having an enormous division in terms of generation, many parts of German society are catching up in terms of their degree of digitisation; this is especially true for people with formal middle and lower education as well as for people from rural areas.

According to the latest D21 Digital Index study, Generations Z and Y are at a comparably high index level and have high digital proficiency. Generation X can still keep up well, but baby boomers and the post-war generation follow at a clear distance, and the oldest generation up to 1945 consists mainly of digital outsiders.

Image Source: Flickr | D21-Digital Index 2021-2022

Image Source: Flickr | D21-Digital Index 2021-2022

Bridging the digital skill gap can help to reduce inequality and ensure that all members of society have equal opportunities in the digital world, but it’s also crucial to alleviate the talent shortage by providing a larger pool of qualified individuals who can contribute to the growth and innovation of the digital industry.

As the tech industry faces talent shortages across skills and competencies, companies struggle to acquire talent that can provide the necessary skills. Generally, companies can solve a specific skill gap through recruitment, outsourcing or providing their workers with further training. In the long run, providing constant training seems the most suitable to face the future, as it looks ever-changing in the face of tech’s rapid evolution.

According to MacKinsey’s Germany 2030: Creative Renewal report, by the year 2030, approximately 4 million employees will need to transition to different careers, representing nearly 10% of the workforce. Furthermore, over 6.5 million will require significant skill development to keep pace with advancing digitisation. A comprehensive and ongoing education system prioritising lifelong learning will prepare the workforce for the evolving job market.

To overcome the talent shortage in the tech industry, companies must invest in training and upskilling or reskilling their existing employees. Training helps employees acquire new skills and knowledge and leads to higher employee retention and reduced turnover, allowing companies to retain valuable talent and avoid the cost and effort of constantly searching for new hires. Moreover, investing in employee training helps companies stay ahead of the competition and stay relevant in an ever-changing technological landscape.

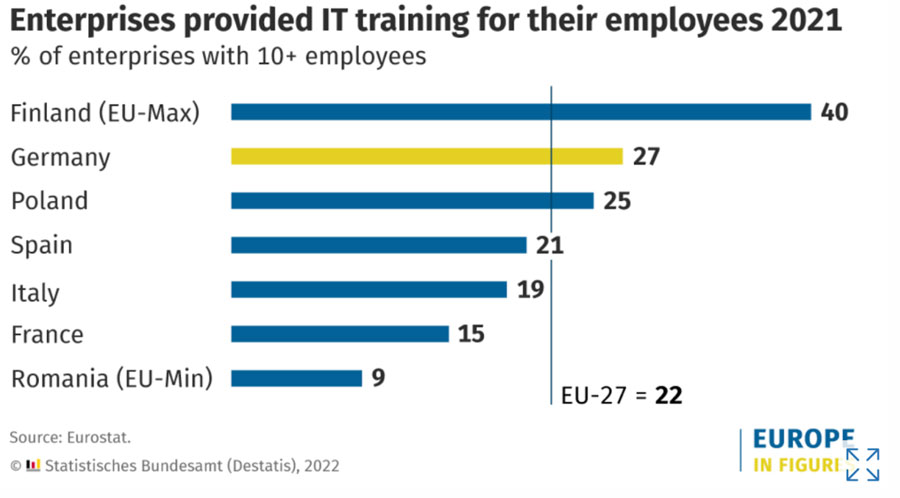

According to data from Eurostat, 27% of German enterprises are actively providing training for their employees, just above the EU average.

Image Source: Eurostat

Image Source: Eurostat

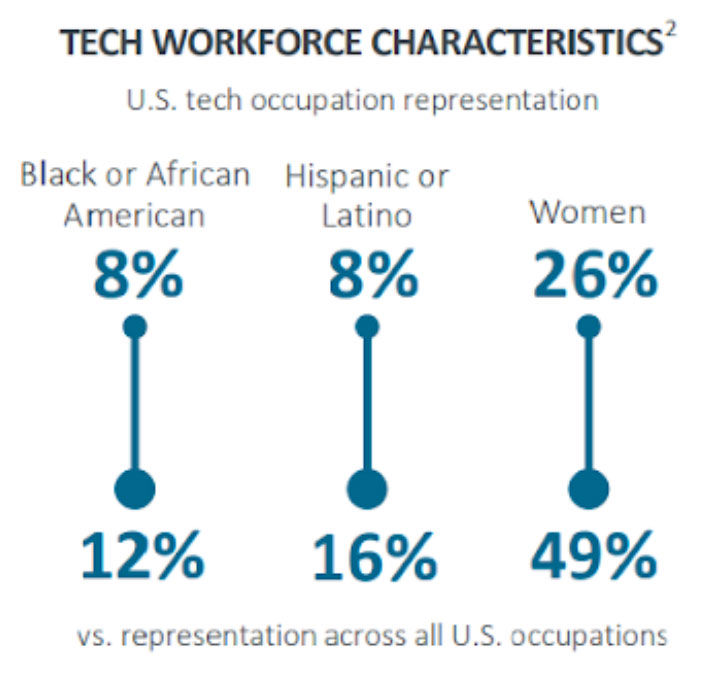

The tech industry in Germany employs around one million people, but just 17% of tech jobs are held by women, despite the fact that women make up nearly half of the country’s workforce. This disparity between the number of women working in the tech industry compared to the overall workforce is referred to as the Gender Gap.

The lack of representation of women in technology is not just a problem for companies and their diversity and inclusion initiatives. It starts long before people enter the workforce and is already evident in students’ career choices. According to data from Erudera, Women made up nearly 35% of students in STEM courses at German higher education institutions during 2021, despite being 52% of higher education overall.

Negative stereotypes can play a significant role in preventing girls from pursuing careers in STEM fields, including in Germany. The stereotype that STEM fields are only for men or that women are not as naturally gifted in these areas can create a self-fulfilling prophecy and discourage girls from pursuing STEM degrees. Girls may also experience a lack of female role models in STEM or face gender bias in the classroom or workplace, further hindering their interest and involvement in the field. Addressing and combating these harmful stereotypes is crucial in promoting gender equality and encouraging girls to pursue careers in STEM.

These stereotypes are vital to understanding women’s underrepresentation in the tech industry and their overall perception of tech, and the role it plays in their lives. According to the Digital Gender Gap study, women tend to achieve a lower level of digitalisation than men, which can limit access to information, hinder job opportunities, reduce efficiency in various industries, and contribute to the digital divide between different socioeconomic groups. Additionally, lower levels of digital literacy can lead to increased vulnerabilities to cybercrime and misinformation. Bridging the digital divide and promoting digitalisation is essential for ensuring a level playing field and equal opportunities for all. Differences in digitalisation (or self-perception of digitalisation) become apparent at young ages:

Image Source: Digital Gender Gap

Image Source: Digital Gender Gap

This digitalisation divide can impact how people feel towards studying STEM-related degrees and pursuing a career in the technology industry. This divide, unfortunately, is not only limited to self-perception in younger ages, it continues throughout higher education, and it’s also apparent when women join the workforce.

One of the Key Opinion Leaders, N. is the CEO and founder of a platform that connects women across the IT industry and provides initiatives for female founders. Regarding women entering the tech industry, she points out:

Soundbite:

N. also mentions how women in the German tech scene hardly have any role models representing women in leadership roles. The lack of role models in the industry severely impacts how young girls perceive tech and the possibilities they have.

According to a European survey by Microsoft, most girls become interested in STEM at the age of 11 but reconsider when they are 15. Surveyed girls named “a lack of female role models” as the main reason they didn’t pursue a career in the sector. Moreover, 60% of participants said they would feel more confident pursuing a career in STEM fields if they knew men and women were equally employed in those professions.

N. talks bout how superstition in the industry plays a significant role in how women are perceived in the industry:

Soundbite:

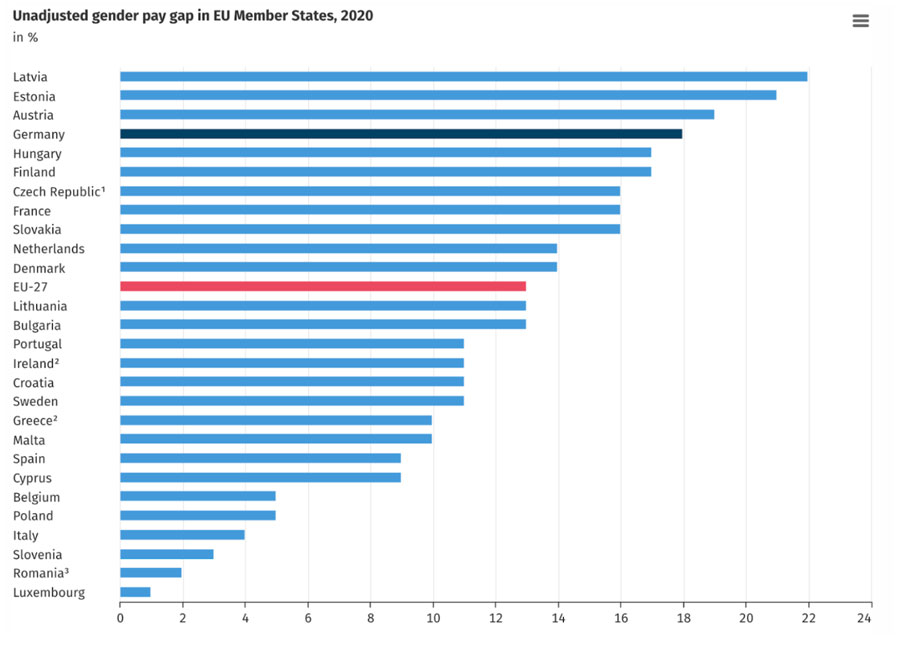

When women overcome these initial access barriers and pursue a tech career, they can still face significant challenges within the sector. One of these challenges is a gender-based pay gap. In late 2019, a Honeypot study revealed that the German gender pay gap in the tech industry is one of the worst in Europe, with only Greece, Poland, Estonia, Slovakia, Lithuania, and the Czech Republic having a lower ranking. To be exact, male tech workers in Germany earn, on average, almost 15,000€ more per year than their female counterparts.

This pay gap is not exclusive to the tech industry, as 2020 data suggests that Germany remains among the EU states with the highest pay disparity:

Image Source: https: Destatis

Image Source: https: Destatis

There are two leading social reasons why women earn less, and in Chapter 8 of this volume, titled Gender Equity in STEM in Higher Education, authors Jennifer Dusdal and Frank Fernandez use the engineering sector in Germany as an example. Some researchers believe that pay disparities are due to the gender makeup of certain professions, with women earning less in male-dominated fields and more in female-dominated fields. Others believe that women earn less because they tend to work part-time. Studies have shown that in Germany, the pay gap between women and men is smaller when limited to full-time employees, and German women appear to be more willing to choose part-time jobs. The Covid-19 pandemic exacerbated the shift towards female part-time work.

Women can also face social and cultural challenges once they enter the tech industry. As N. explains, they may face bias and myths about their performance, criteria or skills:

Soundbite:

Facing academic, social and workplace challenges contributes to women exiting the tech industry earlier and more frequently than men. By the age of 30, only 20% of women in the EU are still working in the IT profession for which they have been educated; by the age of 45, the figure is as low as 9%, according to data from Third Equality Report of the German federal government.

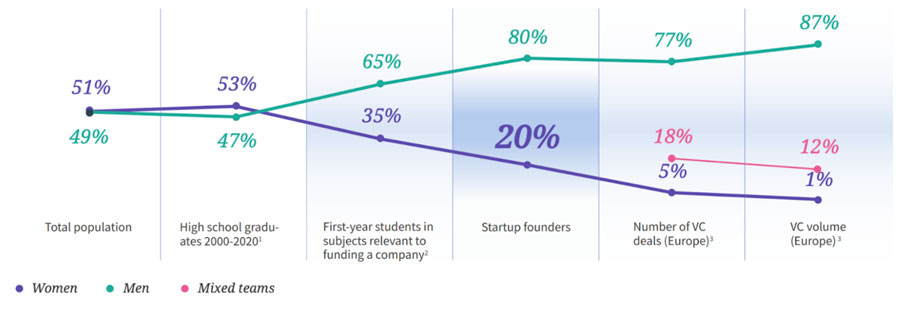

Female tech founders face different challenges, but they are still significant and relevant for the overall state of the industry. According to the Female Founders Monitor 2022, the share of female founders in Germany has risen to 20%, and 37% of founding teams currently include at least one woman – but they remain significantly underrepresented. For example, only 6% of female founders are active as business angels. The Female Founders Monitor also found that Female teams have a stronger focus on sustainability as part of their corporate strategy, and 61% say that their startups are committed to social entrepreneurship.

This overall map represents the Gender Gap in entrepreneurship from the Female Founders Monitor 2022:

The percentage of female founders in the German startup ecosystem has increased by 7.5% since 2013. Despite this progress, 63% of startups still only have male founders, indicating that there are still structural barriers in place and much work to be done in areas like networks and balancing work and life.

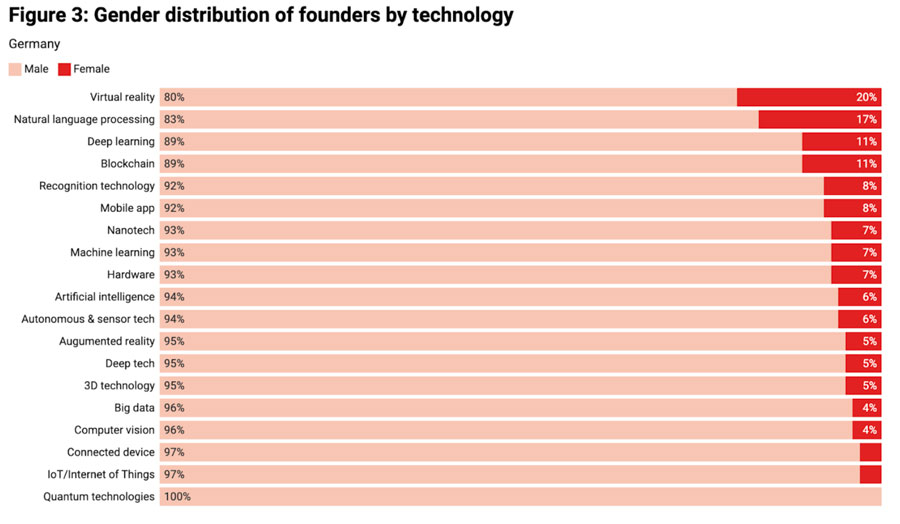

Data from the Gender Diversity in German and French Startups suggests that women are highly underrepresented as founders in all startup categories.

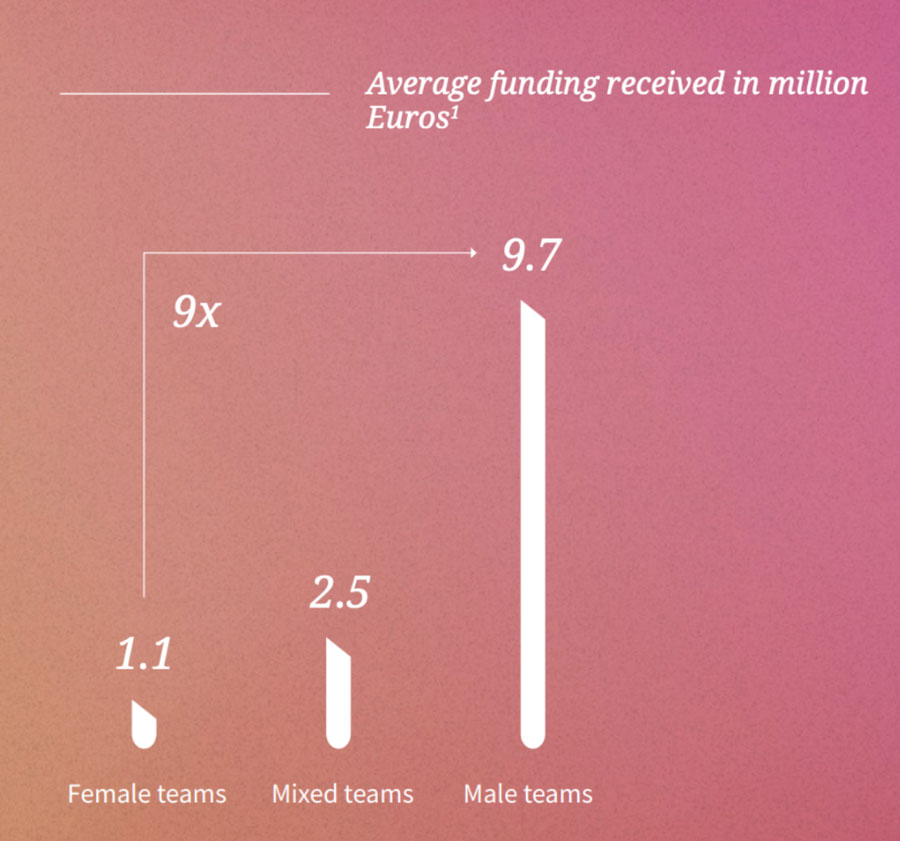

Funding is also a concern for Female Founders, as women-led start-ups in Germany have an 18% lower chance of acquiring investor funds after their foundation. In the third round of financing, the probability of success is even 90% lower.

According to a 2019-2020 Boston Consulting Group study on German Startups Diversity, statistics demonstrate that there are still significant structural barriers in place for women in the startup world and that more work needs to be done in areas such as networks and work-life balance. Unfortunately, Germany lags behind other countries, such as France and the United Kingdom, regarding gender diversity in the startup world. At the present rate, the BCG study suggests that parity will not be reached in the German entrepreneurial ecosystem until 2139.

In Germany, start-ups founded by women face a significant disadvantage in securing funding compared to those founded by men. According to the BCG report, female start-ups are 18% less likely to receive funding, receiving 25% less funding from prominent investors, 40% less likely to secure series-A (second round) funding, and a staggering 90% less likely to secure series-B (third round) funding.

The average funding received by female start-ups in Germany is also lower, coming in at 3.1 times less than that obtained by male-led start-ups, which is a broader gap compared to the UK (1.3 times) and France (2.5 times). This disparity is even more pronounced regarding valuation, with female start-ups valued 16.4 times lower than their male counterparts when raising seed funding.

The Female Founder Monitor expands on this funding disparity, adding that female teams are slightly less likely to secure funding (62% vs 64%). Still, the amount of funding they receive is vastly different. On average, female teams plan to raise external capital at a lower rate than male teams (65% vs 70%) and aim to raise smaller amounts. Female teams have a more cautious approach, targeting an average capital demand of €1.6 million, which is three times less than that of male teams.

Image Source: 2022 Female Founders Monitor

Image Source: 2022 Female Founders Monitor

The absence of women in the tech sector, both in key leadership positions and technical roles, is detrimental not only to the industry but also to the economy’s potential growth. The homogeneity in the tech industry has been shown to be a hindrance to innovation and foster a less inclusive culture. For these reasons, the tech industry must take a proactive approach to promote diversity and inclusivity to build a workforce that reflects society’s rich diversity in the future.

In the current world, the Internet has become an essential part of people’s lives, and it interferes with their daily routine in an intersectional way. The internet and electronic devices affect everything from shopping, entertainment, education, work, transport, banking, healthcare, and even social interactions. Moreover, our data are exposed more than ever to cyberattacks and cyber threats.

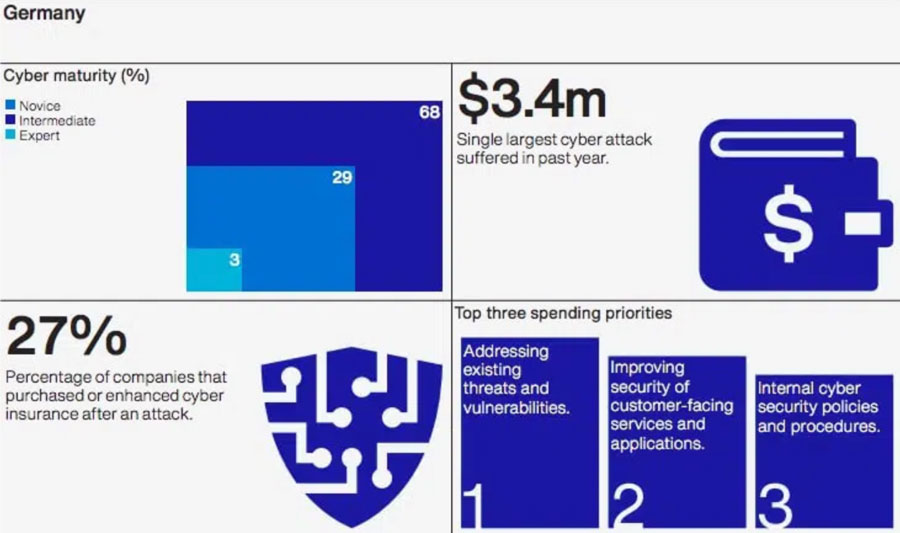

With over 70% of German companies being subject to a successful cyberattack within 12 months, it’s no wonder that 40,4% of German internet users aged 16 to 64 are worried about how companies use their data online, highly over the worldwide average of 33,2%.

Image Source: Cyber Readiness Report 2022

Image Source: Cyber Readiness Report 2022

The cybersecurity market is expected to show an annual growth rate of 7.7% from 2023 to 2027.

Regarding cybersecurity, Germany is pushing itself as a technologically independent country like the US and China. In August 2020, the government announced the launch of a federal agency dedicated to strengthening the country’s digital security against cyberattacks. According to the Cost of Data Breach Report by IBM statistics, Germany was in the top 5 nations with the highest average data breach cost, costing $4.85 million in 2022.

As innovative solutions for implementing the cyber security strategy are needed in all economic and societal sectors, the Federal Government has adopted the 2021 Cyber Security strategy for Germany to improve the overall framework for safeguarding security. This policy provides a roadmap to cyber resilience, defined by Cisco as “the ability to anticipate, withstand, recover from and adapt to adverse conditions, stresses, attacks, or compromises on systems that use or are enabled by cyber resources”.

Also, the IT security “Made in Germany” is an internationally recognised mark of quality and a long-term research funding programme launched by the Bundesministerium für Bildung and Forschung (BMBF, Federal Ministery of Education and Research). It focuses on strengthening the country’s position as an industrial location and protecting the data and privacy of its citizens.

Image Source: GDATA

Image Source: GDATA

According to Mordor Intelligence, over the past few years, security systems have focused on making it difficult for attackers to reach critical data, but with the increase of generated data and the quickly changing technologies, the solutions need to be updated constantly to avoid security exposure.

Due to this, many organisations struggle to fill positions on their security teams because of a skill gap, which according to the study by IBM on The Cost of Data Breach, has immediate implications for the cost of a data breach. Training highly skilled workers has become an important aspect of German IT security research sustainability, so the BMBF founded the KASTEL competence centre, an Institute of Information Security and Dependability which certificates specialists in the IT security area.

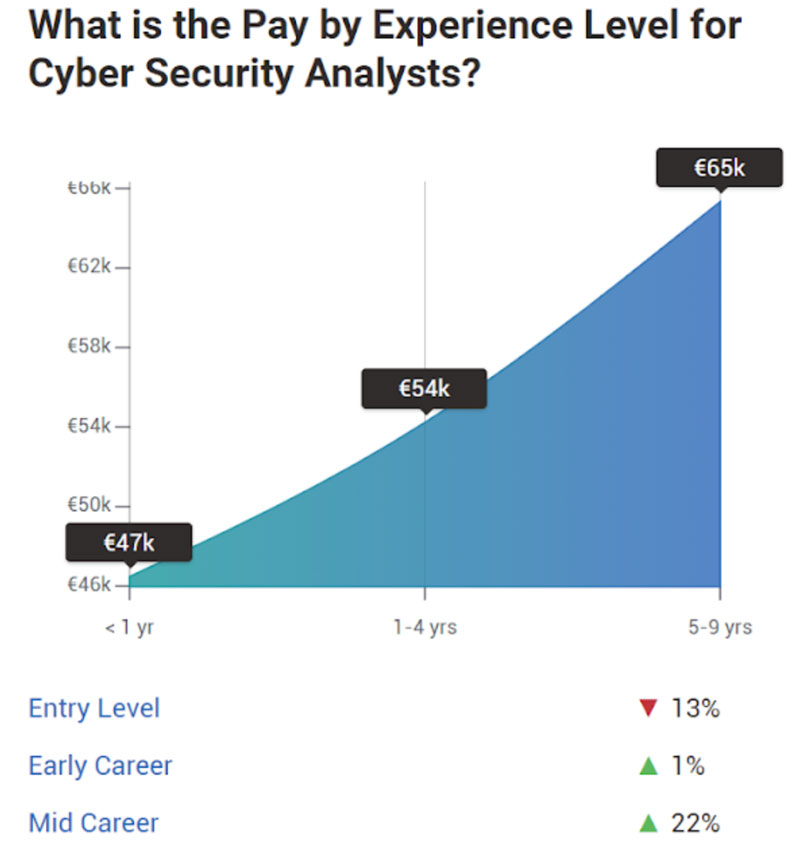

When it comes to wages, according to Payscale, the average salary for a Cyber Security Analyst is 53.328€. Compared with the UK, where the average wage is 37.000€ and France, 41.311€, German workers are the best paid in Europe.

Image Source: PayScale

Image Source: PayScale

The general trends for cybersecurity in 2023 will be:

- Adaptation to new legislation. The new edition of the European Union’s next Network and Information Security Directive (NIS2) regulates the security requirements and reporting obligations that companies and state-owned enterprises must fulfil.

- The impact of AI. Following the 2022 tendency, AI will continue to impact the cybersecurity environment significantly, taking on an important role in businesses, creating real-time solutions faster than humans and performing various security-related tasks. Deepfake videos will be among the most worrying AI regarding fake news and cybercrime.

- Security in the Cloud and Zero-Trust architecture development. Virtual Private Networks (VPNs) cannot meet the scalability demands with the rising remote working trends, so the Zero Trust security framework will become the major solution for authentification and validation before receiving access to applications and data in the cloud.

Image Source:

Image Source:

Image Source:

Image Source:  Image Source:

Image Source: